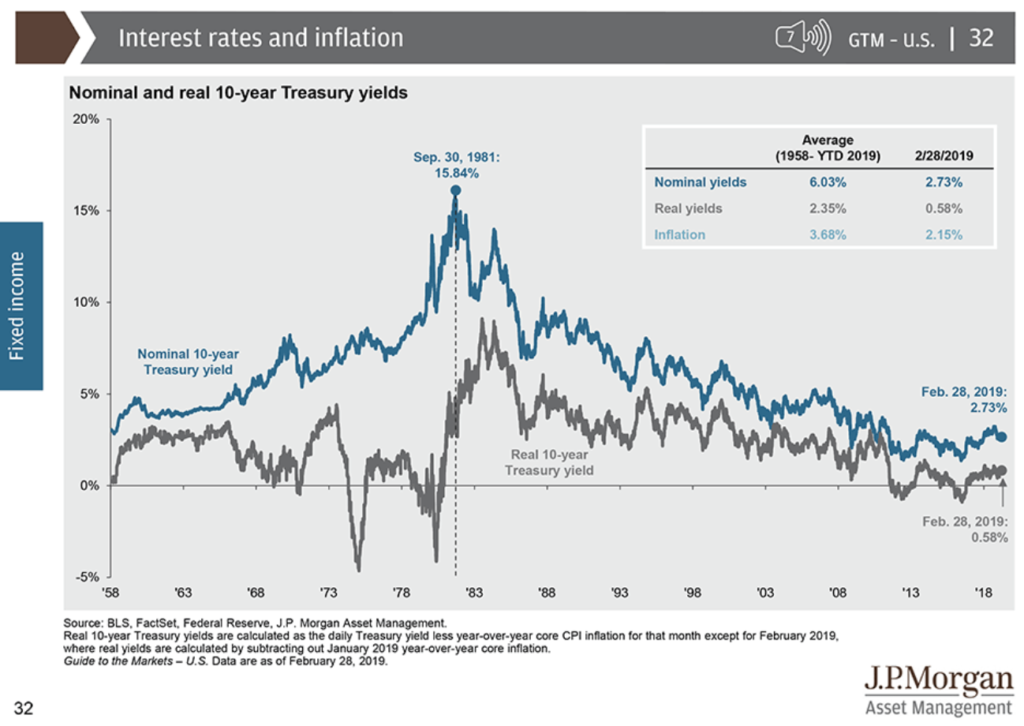

A week ago, I heard Blackstone’s COO, Jon Gray, talk about his company’s recent growth tilt. He said that decline in the U.S. interest rates that has gone on for last 30 years has come to an end. And with that, expansion of valuation multiples too. He is now focused on acquiring businesses that can increase earnings and expand their valuations through growth.

You can see the 30-year decline in U.S. 10-year interest rates in this chart from J.P. Morgan:

Liquidating bonds: Until recently, I had about $100K invested in Fidelity’s US Bond Index Fund (FXNAX). This fund tracks Barclay’s US Aggregate Bond index and has an average maturity of about 8 years. My 5-year total return had been 2.51% (pre-tax and annualized). Not a big return but not unexpected either given this was a safe but slow-growth asset. A vast majority of times, bonds don’t outgrow stocks. They are there to protect from unexpected deflation and bring stability to the overall portfolio.

I had been considering liquidating this position and moving this money into a higher return asset. But at the same time, I didn’t want to add to my common stock holdings — I have significant exposure to them already in my portfolio. What I really wanted was an asset that would allow me reasonable exposure to equities’ upside but also limit my downside to less than 5% loss. In other words, I was looking for an asset that would be a bit higher on the risk-reward curve than a bond position but not at par with common stocks. This money was meant to be in a safer asset than common stocks.

Enter my own home-brewed structured investment … Using long-dated stock options and an underlying common stock position, I created a position that limited my downside exposure but at the same time enabled me much higher positive return potential than otherwise possible with bond-like assets.

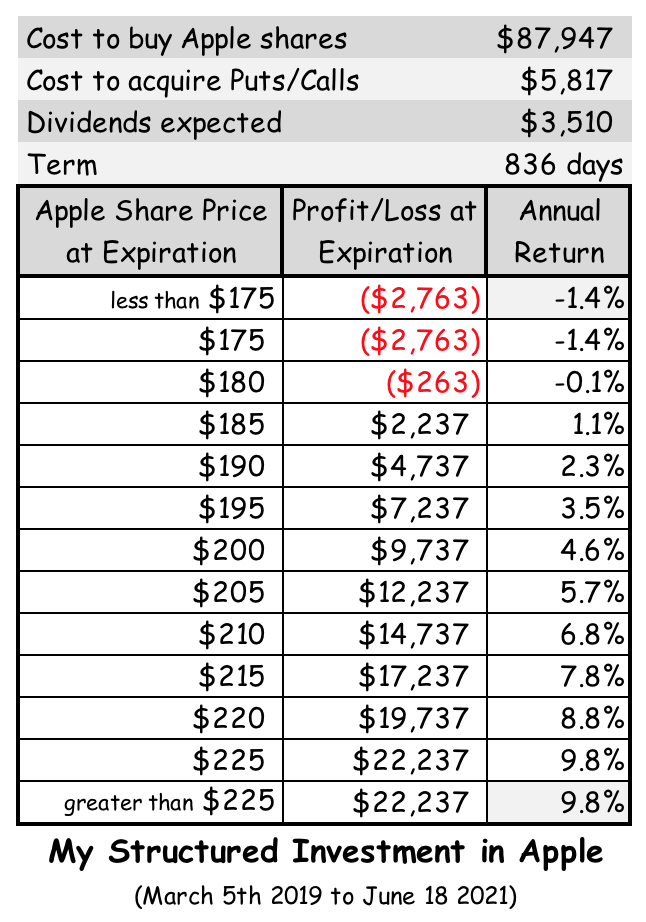

This is how I structured it: I bought 500 shares of Apple (AAPL) common stock at an average share price of $175.89. Concurrently, I bought 5 contracts of long-dated (June 2021) Put options on Apple with the strike price of $175. This would limit my downside risk to about $175. To pay for my Put protection, I also sold 5 contracts of same-dated Call options with the strike price of $225. This had the effect of limiting my upside gain to $225. Between the Puts and the Calls, I paid $11.65 per share.

In essence, this forms a protective collar around my Apple shares. I have previously written about other variations of protective collars here and here. There is one major difference with this position, however. Here I will be taking some downside risk while in my market-neutral positions, there was virtually no risk.

For this position, my average annual return could range anywhere from negative 1.4% to positive 9.8%.

I wish we had even longer-dated stock options available to us, but we don’t. Farthest these options (LEAPS) go is about two years. This is one difference between us the individual investors versus investment banks. Investment banks have the ability to create much longer dated (5 to 6 years are quite common) structured investments than what we can do with publicly traded stock options.

On the other hand, those professional structured products from investment banks cost a lot more too. Investors who buy those products usually end up paying 3% to 4% in commissions and fees. Contrast that with my paying about $30 to set up this position in a Fidelity managed IRA.

Why I chose Apple as the underlying security? I could have picked another common stock. Indeed, I could have also created a similar protective collar with a whole-market ETF such as SPDR. Here are my three reasons for going with Apple:

(1) I like Apple’s business and its current management. I previously wrote about Apple’s CEO in this post: CEOs who take pay cuts. Apple has brand power, enormous scale, loyal customers, and thoughtful long-term minded management — all of which gives it a strong competitive edge over rivals. Even Warren Buffett likes Apple — even though he is generally not into technology businesses. In fact, it makes me happy to claim that I had found Apple before Buffett did. I own Apple shares since 2011.

(2) Apple’s share price is down by about 30% from its peak. This is important because, unlike my regular stock positions that are open-ended, this investment has a time-frame associated with it. In order to make money, I need Apple to move up from its current price in less than two and a half years. I believe Apple has a good chance to move up from here within two years. Apple shares have been over-sold lately, in my opinion.

(3) One other thing going for Apple today is its aggressive capital return policy. Management announced last year that the company plans to operate with zero net cash moving forward. While there was no definite timeline given for this, it is widely expected that they will return all excess cash on the balance sheet (along with majority of its annual Free Cash Flow FCF) during the next four years. It currently has $130 Billion net cash on its books, as of 1Q FY2019. On top of it, it generates roughly $50 Billion in FCF every year. In last three years, Apple has increased dividend per share by about 10% annually. Per my calculations, if it continues capital return at the same rate as it did in 2018, it would increase its dividend between 11% to 12% yearly from here. Value line estimates 15% rate of increase for the next five years.

This investment is 27 months in duration. I expect nine quarterly dividend payments. I will be better off if Apple moves even more aggressively with its capital return plan during the next two-and-a-quarter years.

As I wrote in this blog post – Grading CEOs as capital allocators – Apple has an excellent record returning excess capital to shareholders. It has been an aggressive share repurchaser. It reduced its share count by 25% during the last six years.

This is a two-year commitment and I plan to let it run for that long. In the near-term it wouldn’t matter what I think of Apple stock’s fair price. Its shares will move as the stock market moves. In fact, Apple has already dropped about four points (as of March 7th) below my purchase price of $176 and it’s only been less than a week. But that’s ok by me. I don’t need to monitor Apple’s stock performance on daily or even weekly basis. As I explained in a previous blog post, I don’t focus on checking stock prices every day.

There are two extreme scenarios where I might consider closing this position early. Both are unlikely though:

The first scenario is where Apple’s share price moves up quickly and far beyond my $225 Call strike level — say it reaches $250 in six months. In this case, both my options would have lost majority of their time-values. And I’d have gained maximum capital gains I could possibly achieve. I would then just close the entire position — foregoing any remaining dividends. My dollar gain would be somewhat less than if I had waited until expiration, but my rate of return would be much higher due to the shortened time frame. I’d expect my annual return to be 15% or higher. I’d then release cash early and look elsewhere for another opportunity.

The other scenario is where the share price is way below my Put strike threshold of $175 and I have already collected my last dividend payment (expected in May 2021). This would be about a month before expiration. In this case again, both my options would have already lost most of their time-values and I’d have substantial capital gain on my in-the-money Puts. In this case, I’d sell the Puts and buy back the Calls (if any value left in them) but still keep my Apple shares. Let’s say Apple shares have dropped to $100 by the time I receive my last dividend payment. By selling Puts, I’d have recovered about $75 of my original cost. I would then be left with an unprotected position of 500 Apple shares where my cost basis is only about $4 or $5 above its share price. So, rather than take a small loss and close the entire position, I’d have converted it into an ordinary long stock position. I might consider taking this approach if Apple’s long-term business prospects still look good at the time.

No substitute for stocks: Would I consider moving money out of stocks into protective collars like this one? After all, my stock investments are open-ended — no downside protection. Protective collars like this might be tempting for some investors but I don’t see them as substitutes for common stocks. My stock positions have unlimited upside and no expiration dates. I plan to keep them for a long time. On occasions, I may move money between different stocks or take some profits, but I plan to keep my overall stock allocation about the same. My capital invested in stocks is of patient and long-term nature. In February last year, in a blog post (Yes stocks are volatile) I showed how if we invest in stocks for 10 years, we’ve almost no downside risk (worst-case negative 1%) but our upside could be as high as 19%. Average annual return for stocks is 11% but because of high volatility, investors won’t even get to average returns if we limit our upside for the sake of downside protection.

Recall how I started with this protective collar. I had a bond investment which I didn’t think would be going anywhere. So I switched into a protective collar to move up a bit on the risk-reward curve. Given where Apple shares are trading at and its future prospects, I think I have better-than-average odds of winning this bet (I give it about a 70% chance of turning profitable). Let’s see how it goes.

Hi emcee, I’d be interested to know where you are with this trade right now and how you think about it going forward, cheers!

Hi Graham, I just posted an update on this position. See my latest post: https://www.investingparexc.com/2019/10/29/update-on-apple-bet/