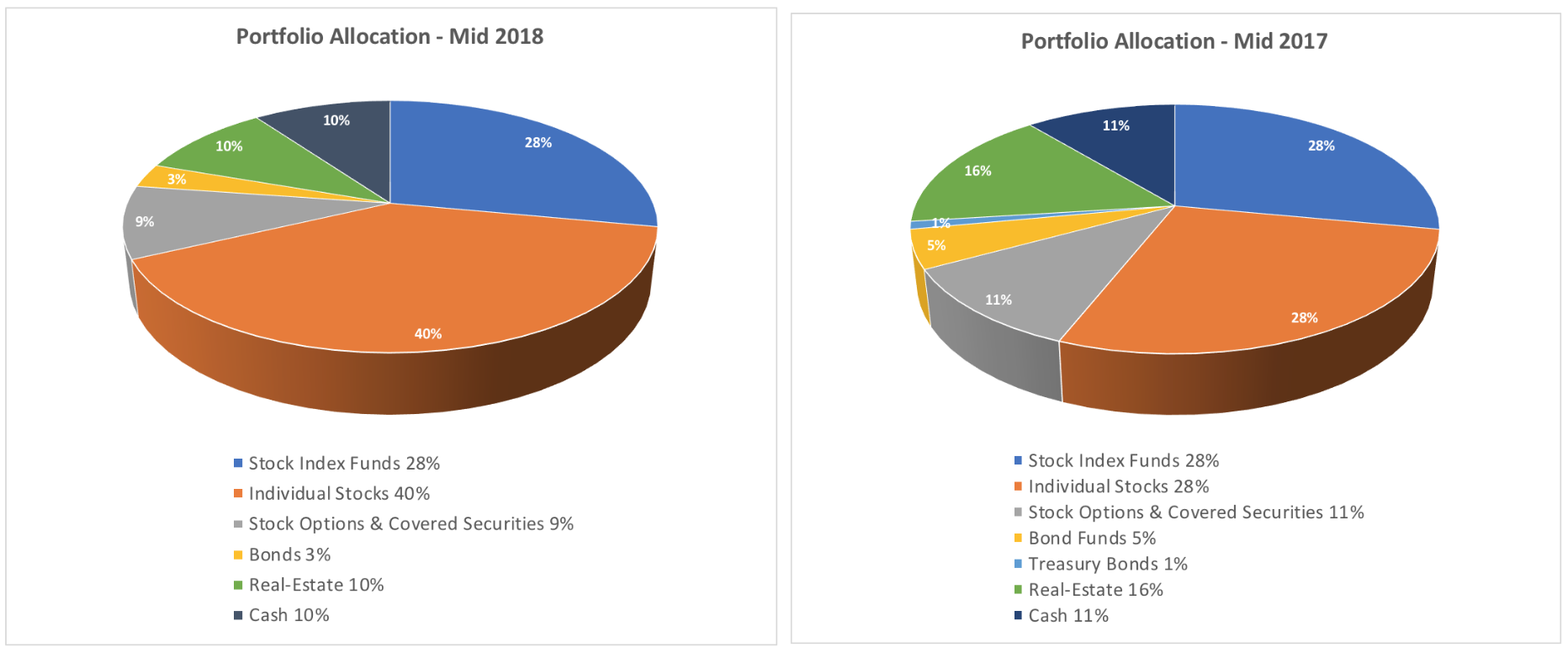

Since my last quarterly update, there haven’t been many changes in my portfolio. Stocks have been on the rise since April this year — making up for the losses in the first quarter. Looking further back, if I compare today’s asset allocation with what I had last year, there have been some notable changes. See the two pie charts below. Today, my equity holdings (especially individual stocks) have become a larger percentage of the portfolio. Two reasons for that. One, the stock market’s substantial rise from last year – and two, real-estate holdings haven’t kept pace with stocks.

Since my last quarterly update, there haven’t been many changes in my portfolio. Stocks have been on the rise since April this year — making up for the losses in the first quarter. Looking further back, if I compare today’s asset allocation with what I had last year, there have been some notable changes. See the two pie charts below. Today, my equity holdings (especially individual stocks) have become a larger percentage of the portfolio. Two reasons for that. One, the stock market’s substantial rise from last year – and two, real-estate holdings haven’t kept pace with stocks.

Inspiration. Apart from equity holdings which I will go into a bit later in this post, I also had some other tweaks to the portfolio. These secondary changes were inspired by my reading of David Swensen’s Pioneering Portfolio Management book. I had also written about this book in an earlier post where I benchmarked myself against Yale’s endowment fund. It is a remarkable book — very original and unique with regards to how Swensen approaches asset allocation. Everyone managing an investment portfolio — professional or part-timers — would benefit from reading this book. His writing style is academic which can be a turn-off for some readers. Though, after I persevered through the first couple of chapters, I was hooked.

Inspiration. Apart from equity holdings which I will go into a bit later in this post, I also had some other tweaks to the portfolio. These secondary changes were inspired by my reading of David Swensen’s Pioneering Portfolio Management book. I had also written about this book in an earlier post where I benchmarked myself against Yale’s endowment fund. It is a remarkable book — very original and unique with regards to how Swensen approaches asset allocation. Everyone managing an investment portfolio — professional or part-timers — would benefit from reading this book. His writing style is academic which can be a turn-off for some readers. Though, after I persevered through the first couple of chapters, I was hooked.

What sets Swensen apart from many other financial writers is his accomplishments. He is first and foremost a practitioner — not an academic or a journalist. He’s been running one of the world’s largest university endowments for over 30 years — with outstanding results. He practices his portfolio allocation in the real world. It’s the same reason why I follow Howard Marks’ and Ken Fisher’s writings closely. Like Swensen, Marks and Fisher are also full-time investment professionals par excellence!

Back to my portfolio discussion … two changes I made after reading Swensen were in bonds and real-estate allocations.

First, the bonds. Swensen advocates keeping only a small fraction of bonds in a portfolio — certainly far less than most professional (or amateur) portfolio managers used to hold at the time of his writing. Swensen points out in his book that bonds’ main purpose is to protect against unexpected financial trauma and deflation. And even for that purpose, only non-callable highest quality government bonds are effective. We witnessed that in the 2008 financial crisis when corporate bond market essentially stopped functioning after the Lehman crash — and treasuries, on the other hand, rallied because investors piled into safe assets.

Relative to corporate obligations, US Treasury bonds contain fewer alignment-of-interest issues, as the government lacks a strong set of incentives to reduce the value of existing debt obligations … Investors frequently own more fixed income than necessary to protect against hostile financial environments, leading to behavior that undermines the fundamental purpose of holding bonds.

David Swensen, Pioneering Portfolio Management

In my portfolio, I have now reduced my bond holdings to roughly 3% and swapped corporate bond funds with treasuries. Mostly I own Series-I Treasury bonds where I don’t pay any tax until I cash out my holdings.

Then, real-estate. You can see from the pie charts that my real-estate allocation has also dropped since last year — from 16% to 10%. The numbers are misleading though because I’ve actually added to my real-estate holdings. It’s just that the equities have increased in value substantially since then. As I wrote in this blog post, My Quest for Commercial Real-Estate, I have been researching real-estate investments. Failing to find any suitable private deals so far, I have moved to public REITs (Real Estate Investment Trusts) as an alternative. For individual investors, REITs are more accessible than private real-estate deals. Publicly traded REITs, especially in the retail sector, have been out of favor lately. My favorites today are Simon Property (SPG), American Tower (AMT), and Retail Opportunity Income (ROIC). I have been adding to them.

Long term investors favor REITs when portfolios trade at a discount to private market value, avoiding high-priced private assets, and sell REITs when shares trade at a premium, pursuing relatively attractive private properties.

David Swensen, Pioneering Portfolio Management

Market cycles. Howard Marks in his book, The Most Important Thing, wrote about the inevitability of market cycles. They are also unpredictable, to both extent and timing. How could investors deal with them? He suggested three possible solutions. One, we could redouble our efforts to try and predict them. Two, we could just ignore them and hold our investments throughout. Three, we try to figure out where we presently stand in terms of cycles and act accordingly. His preferred strategy is #3. Know where we are and stay prepared for the cycle to turn without knowing precisely when and by how much.

I am mostly a #2 kind of an investor — riding out market cycles patiently. I posted my thoughts on this in a previous blog entry: Stock investing is not a zero-sum game. However, Marks makes some very persuasive arguments in his book. Inspired by his words, I’ve begun to lean towards #3 myself. So where do I think we currently stand in this cycle? Like Marks, I also think we are in the latter stages of a market upcycle. How do I prepare my portfolio for this? I’ve gradually increased my dry powder cash holding over the last two years to take advantage of an inevitable downturn — whenever it may come. Percentage wise, today I have roughly the same cash allocation from last year but, in dollar terms, my cash holdings have gone up significantly. The overall pie has gotten bigger too.

Equities. My portfolio is full up on equities. I am not adding to equities at this time. Also, my dry powder cash holding is also adequate for now. I am comfortable with the current mix of buy-to-hold equities (68%) and cash (10%).

I still buy some individual stocks opportunistically though. Even in this bull market, there are occasional company specific events that result in good bargains. When I do buy, I sell proportionally from stock index funds to fund purchases — keeping my overall equity allocation about the same.

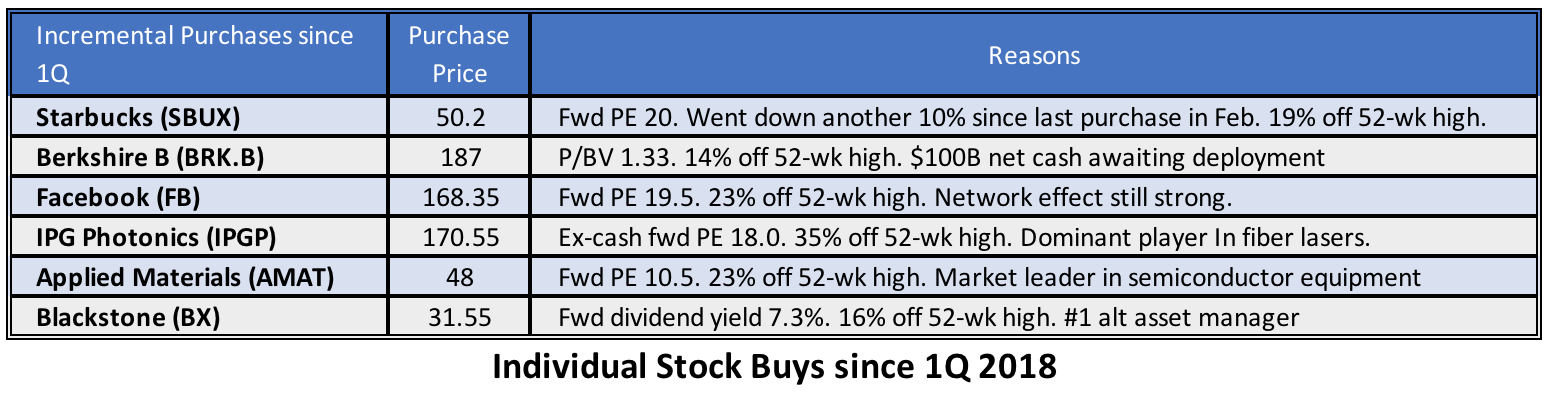

I did some buying in the second quarter too. These were all incremental purchases to my existing stock positions. You can see from the table below what I bought and why. Collectively these stocks were down about 23% from their 52-week highs. I have an active investment thesis for each one of these businesses — and I am convinced that they are the kind of durable franchises that will survive and thrive throughout economic cycles. I wrote about some of them previously here, here, and here.

Cash. Lastly, a small change in my dry powder strategy. I now more aggressively use protective collars to generate higher-than-cash income. When stocks will turn lower, I won’t make much out of my collars but then I’d be ready to deploy some of this cash by investing in stocks. I wrote about this change in another post last month: Revisiting my dry powder strategy.

Cash. Lastly, a small change in my dry powder strategy. I now more aggressively use protective collars to generate higher-than-cash income. When stocks will turn lower, I won’t make much out of my collars but then I’d be ready to deploy some of this cash by investing in stocks. I wrote about this change in another post last month: Revisiting my dry powder strategy.

Based on my dinner conversation with the folks at RealtyShares, the fund is on pace to reach its target IRR of 15% over five years, but I m not holding my breath. If I can get an 8% IRR, I ll be ecstatic. For those of you looking to invest in a fund as well, you might get a chance in 2H2018. I ll be sure to keep you updated.

I am afraid RealtyShare has gone out of business:

“RealtyShares of San Francisco, one of the legions of companies trying to shake up the real estate industry with technology, has laid off most of its people and will no longer seek new business but continue to manage existing deals.”

https://www.sfchronicle.com/business/networth/article/RealtyShares-downfall-shows-perils-of-13379804.php