I worked for one Fortune 100 company for a bit more than 20 years. I had an active 401(K) retirement account while I was working for it. I saved and invested a portion of my earnings every year—taking advantage of company matching dollars and tax-deferred savings. What follows is a mini-journal of my retirement account over those years …

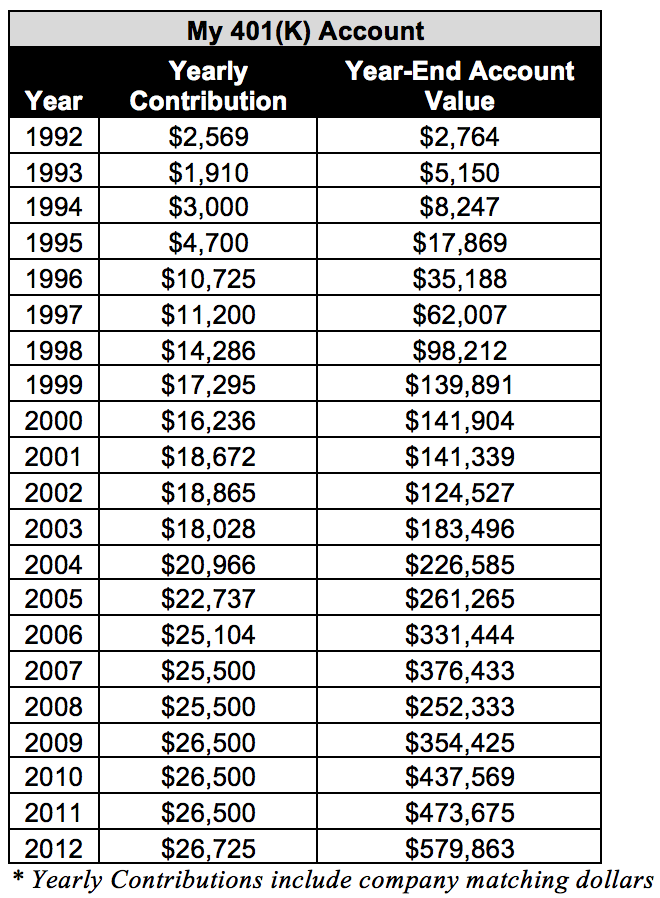

The table below shows actual dollar amounts I invested (includes company matching dollars) every year in the account. It also shows year-end account values.

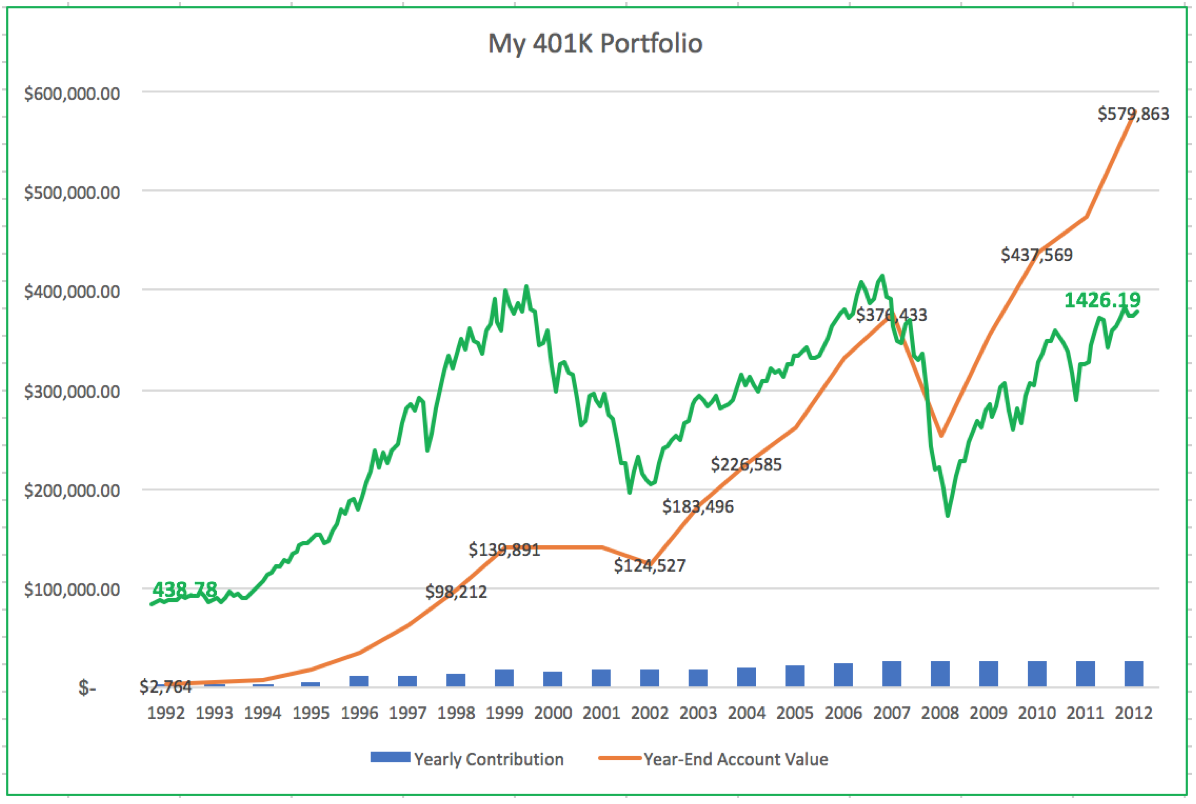

The chart shows the same information visually. I also overlaid the S&P 500 stock market index for the same 20-year period. The S&P 500 graph is not on the same scale though. It is meant as a reference to how the overall market was doing in that period.

1992 – 1997:

When I started working, I was lucky enough to have an employer that offered a 401(K) retirement plan. It even matched 50 cents to a dollar to encourage savings (up to an extent). At the time, I didn’t know enough about investing or the stock market to know what to do about it. I did manage to put little bit of my savings into it initially. At the time, I thought I should get at least those free dollars that the company was matching.

Over the next few years, as I learned more about stocks and investing, I gradually increased my tax-deferred savings every year to keep up with salary/bonus raises. Still, I was just putting enough money to get those company-matched dollars. The thought of paying 10% IRS penalty to withdraw my savings had scared me off. One must wait until he is 59 ½ to withdraw without penalty. I was in 20s. I didn’t think I could keep my hands off this money for another 35 years!

Most of the savings went automatically into a couple of different stock mutual funds that my company plan offered. I did put about 10% in a bond fund but I didn’t keep any cash around. I set up the account so that monthly paycheck deductions would go into those funds every month.

You can see from the table above—I started with investing $2,569 in 1992 and gradually increased it to $11,200 (including matching company dollars) in five years. Still, I wasn’t maxing out my annual contributions—in 1995, the IRS imposed max contribution limit was $9,500 (plus company dollars).

Looking back, those were easy days to make money in the stock market. The market went up steadily without a major downturn. The S&P 500 index went up from 408.78 to 970.43—more than doubling in five years. I started from zero but still by the end of 1997, my savings had grown to $62,000. Interesting times were about to begin!

1998 – 2002:

By now, I had become a firm believer in long-term investing. I also had more money to save. From 1998, I started maxing out my 401(K) contributions. The max IRS limit was $10,000 in 1998.

The first two years, up until end of 1999, the stock market rose to great heights. My maxing-out decision looked very serendipitous. As the stock market went up, so did my portfolio value—more than doubling in two years. Life was good!

Then the downturn began. The stock market went down every year for the next three years. It seemed like bad news was followed by more bad news. First, it was the technology stocks bust. Then, we had the 9/11 attack and the accounting frauds of Enron, WorldCom, and others.

Amid all this turmoil, I kept a steady hand for the most part. I maxed out $10K in 2000 but then dropped to $9K in each of the next two years even though the IRS had raised the limit to $11K by 2002. I guess I was a bit affected by all the negativity surrounding stocks those days. Nevertheless, I did not capitulate and kept on investing with new money every month.

During those three down years (2000 to 2002), I put in over $53,000 of new money into my account—yet the account value dropped by more than $15,000. Ouch!

2003 – 2007:

The stock market finally turned around in 2003 and rose strongly for next five years. As you can see from the table, I kept maxing out my annual contribution—increasing it consistently as IRS raised the contribution limit every year. All in all, during those years I contributed a total of $112,000 to my account but ended up with nearly $250,000 increase in value. I was benefiting from my consistent buying not just in those five years but also the previous three years when stocks could be had for cheap.

2008 – 2012:

To some investors, those five years were disastrous. To others—myself included—it was a tumultuous experience but in the end a highly profitable one. You can see from the year-end account values. In 2008, the market went down big—my account was cut by one-third. In dollar terms, I had lost nearly $124,000 in that single year.

It was painful but I had done my homework. I was aware of the market history and knew that this phase too shall pass. I didn’t waver in my resolve and continued to put max money in throughout. Following the disastrous first year, the market started recovering the next year. It consistently rose each of the next four years—eventually breaking close to even in 2012.

For a lot of people who were watching from the sidelines, those five years appeared like treading water—going nowhere fast. All the market did was break even eventually. On the other hand, for patient investors like me who never lost faith in long-term investing, those down years were excellent times to buy shares on the cheap.

Because I was consistently buying new shares at depressed prices, by the time the market eventually recovered to its previous high, my account had already grown to a new high. You can see this from the chart. During this time, I had invested $131,700 of new money but my overall gains were $203,000. Even though the market did nothing but crater and then recover to its previous high.

Lessons Learned:

It is impossible to know how the stock market will behave in near future. The future is by definition unknowable. When we invest in stocks, we are counting on the long-term appreciation of stocks. During those 21 years, I had diligently put my savings into the retirement account every year—total money added to the account: $363,519. At the end, my account value was $579,863 so I gained about 1.6 times. This may not sound like a big deal but consider this: We went through two of the biggest stock market crashes of our time. And the overall market went nowhere from 2000 to 2012—essentially returning to the same level it achieved 12 years before. Yet, my 401(K) gained in value because I kept buying even when the stocks were on sale.

Here I only journaled this 401(K) account progression until 2012. That was when I quit this job and stopped contributing new money to this account. However, I still own this account today and have not withdrawn any money from it. As the stock market rose relentlessly from 2012, today (October 2017) the value of this account has more than doubled since then.

Footnotes & Clarifications:

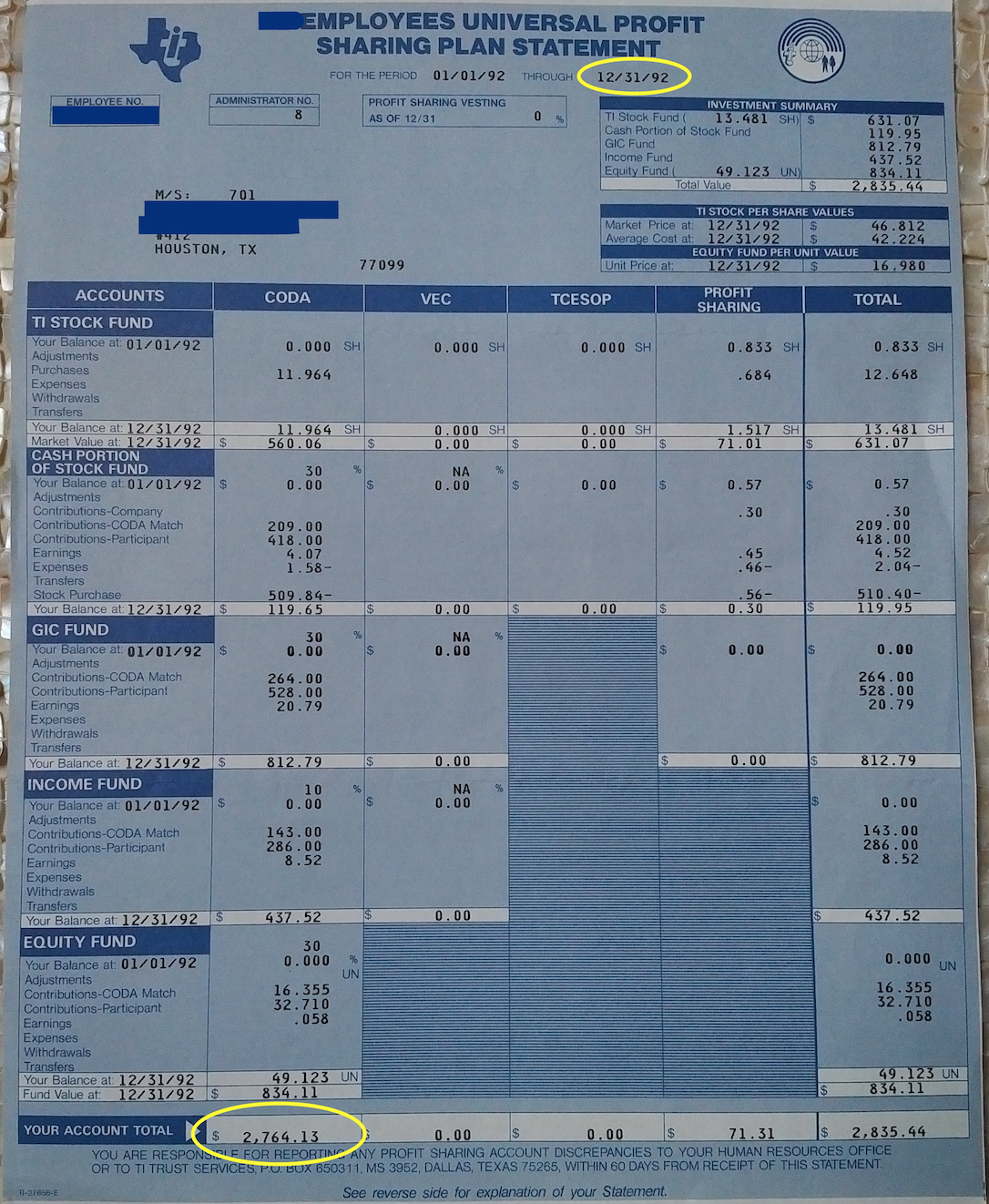

- Year-End Account values shown in the table/chart are actual results (including fees/commissions) obtained in my 401(K) account.

- Yearly contributions shown are total contributions made to the account in a calendar year—both employee and employer matching dollars included.

- The stock market graph is shown for comparison. It is the S&P 500 monthly market index with dividends included. It is not a perfect comparison to the variations in my account value for the following reasons:

- My account was not fully invested in an S&P 500 index fund during the entire period. I had a mix of large-cap, small-cap, and international stock mutual funds that were available at low-cost at the time.

- My allocation was not 100% in stocks. I started out with 80% in stocks and 20% bonds but gradually became 90% invested in stocks.

- I had some shares of my employer’s stock in early years – gradually reduced to zero over time.

Related:

Investing in Installments

What My Portfolio Contains Today?

What an great article/journal. Fidelity/Vanguard should use this and share with companies for new college grads who are just starting out!

The article emphasize the importance of walking with faith and staying invested in the market.

I agree the only way one can retire comfortably is thru regular Investing from young age.

I practiced in an identical way as you did. Thanks for sharing your approach.

Best Wishes

Thanks Sairam! Glad you follow the same approach. My portfolio has evolved over the years – from just index funds to today a mix of funds and individual securities. But the underlying philosophy has stayed the same. Check out:

http://www.investingparexc.com/2017/10/16/what-my-portfolio-contains-today/

http://www.investingparexc.com/2017/11/25/a-deeper-look-into-my-portfolio/

If you had plotted your cumulative contributions as well, you would have seen that up to 2002, you contributed $119,458 and the account value was just about $5K more than that. I started in 1992 as well, and my balance was only $2K more than the cumulative contributions at that time. If I had looked at that number at the time (I only did the chart last year), I would have been really bummed about the situation and might have changed course. The time-weighted return on the investment, which is what the summary statistics for mutual funds show, was about 8% cumulative (to that low point). To me, that highlights the effect of sequence of returns, the importance of looking at the returns the right way, and that investing for retirement needs to be a long-term effort.

Hello John, I agree with all your points above. Thanks for sharing your investing experience from that period! I hope you kept on investing since then.

Benign neglect can be a good thing after all. I wasn’t doing a lot of measurement and tracking back in those days. To me, long term investing mindset comes from detaching myself from emotions of current investing environment and believing in the long-term upward growth in the country’s economy. As I wrote this in a recent post: stock investing is not a zero-sum game. http://www.investingparexc.com/2018/03/19/stock-investing-not-zero-sum-game/