Various organizations and economists in the USA try their hand in predicting when the next recession might occur – none of them have been very successful.

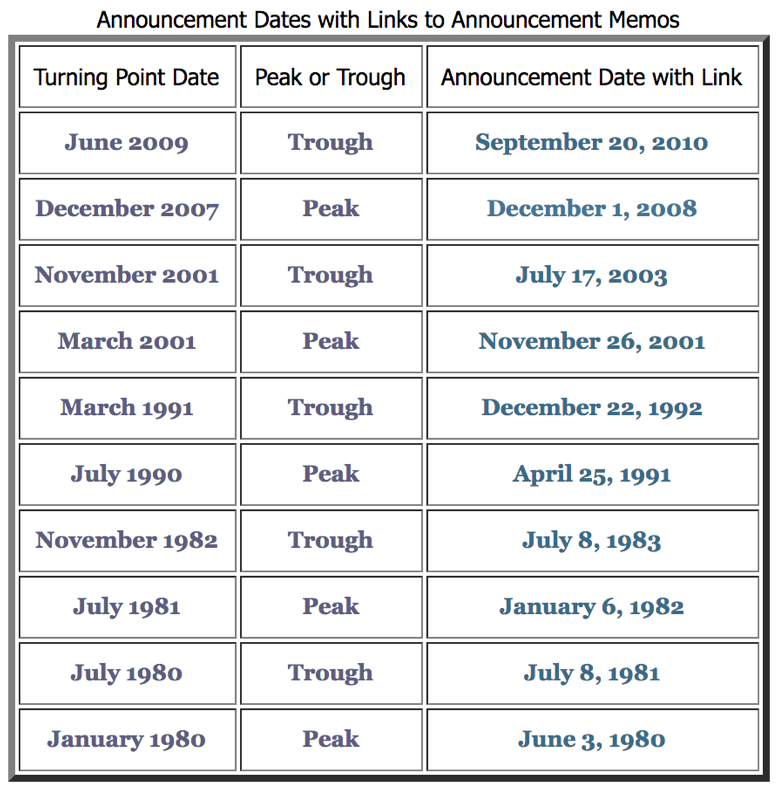

The National Bureau of Economic Research (NBER) is the de facto authority that marks the beginning and the end of each recession in US. However, it does not try to predict a recession ahead of time – just announce it after the fact. And even that announcement usually comes one year after the event. A case in point – today’s expansion cycle began in June 2009 but that date wasn’t determined by the NBER until September 2010 – more than a year later. This table shows the turning points in the US economy over the years – and when they were officially declared by the NBER. As you can see from the table, the NBER declarations usually come six months to one year after the fact.

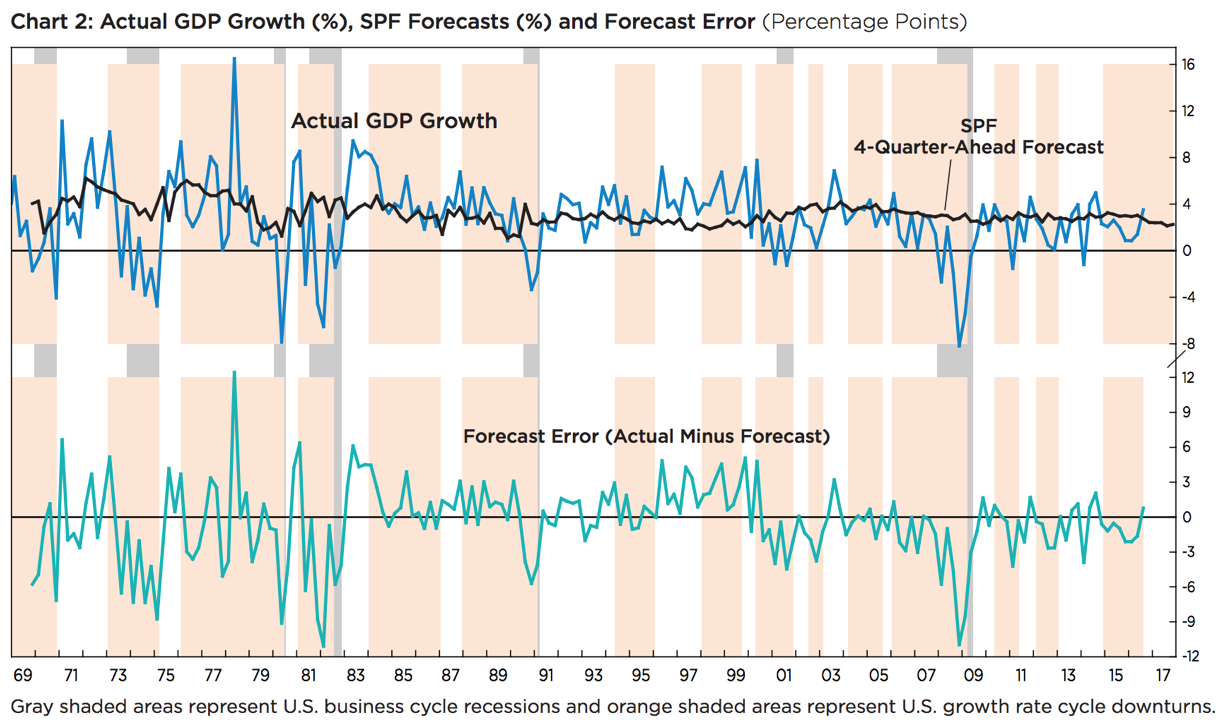

If we can’t count on the NBER to tell us in advance, perhaps we can find some other good economists that can do this job. Not so. Consider this. The Federal Reserve compiles a quarterly survey of economic forecasters (called the Survey of Professional Forecasters or SPF) since 1969. How have they done so far? The chart below overlays their one-year-ahead forecasts with subsequent GDP growth. Since 1969, their consensus forecast had never predicted a single recession.

Looking beyond the USA, evidence of economists correctly predicting a recession is equally scant. IMF researchers published a paper in 2000 titled How Accurate Are Private Sector Forecasts?. It looked at monthly forecasts from 63 different countries over a period of 9 years. It’s conclusion: “the record of failure to predict recessions is virtually unblemished”.

Complex systems such as weather, stock markets, and national economies are very difficult to predict – even for professionals. For more on this topic, read Nate Silver’s excellent book, “The Signal And The Noise – Why So Many Predictions Fail But Some Don’t”.

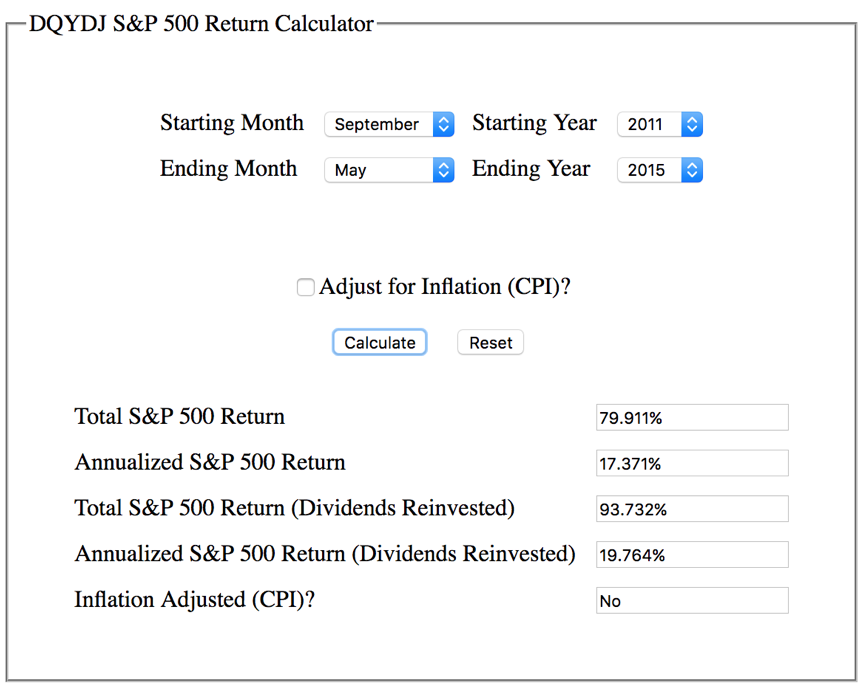

Take a more recent case. ECRI (Economic Cycle Research Institute) is a well-respected private organization in the business of business-cycle predictions. In September 2011, ECRI predicted a recession in the country. It didn’t happen. They repeated this call again in May 2012 – extending the timeline and this time predicting a recession by the end of 2012. It still didn’t happen. When they finally came around to admitting that their recession call was incorrect, it was May 2015. Meanwhile, the US stock market chugged along and nearly doubled during that period. If an investor had paid heed to ECRI and gotten out of the market in September 2011 and stayed on sidelines until May 2015, he would have missed out on 94% of potential portfolio gain (dividends reinvested – see table below).

When it comes to predictions about the stock market and national economy, maintain healthy skepticism! Even better – just ignore them. Given the history of failed predictions, you are better off not basing your investing decisions on them.

Historically, stock markets have been among the leading indicators of the state of the economy. Markets tend to drop ahead of an upcoming recession. Often times, a good 3-6 months ahead. In other words, markets foretell economic conditions – not the other way around. For instance, the current expansion cycle started in June 2009 per NBER. However, the US stock market had already started recovering in March 2009 – a good three months ahead of time.

Patient long-term minded investors should not care about recessions. They are inevitable. We can’t predict them – neither can we control them. What we do control is our own investing behavior before and during a recession. I stayed invested during the last two recessions and came out unscathed. Read more about my 20-year 401(K) journey here and why I stay invested during market downturns here.

hi,

interesting post.

But, whatdo you think about Mr Martin Armstrong and his “Socrates” algorythm ofeconomical forecasting?

https://www.armstrongeconomics.com/

Hi erman: I haven’t studied Martin Armstrong’s predictions so I don’t have much to say specifically about his methods. However, I’d be very careful in relying on any one economic forecaster – unless they have established a long-term record of accurate predictions. I doubt if anyone has. Reasons why economies are so hard to forecast:

(1) They are constantly evolving

(2) Economic data is very noisy

(3) They are complex dynamic systems

I am no expert. If you ever get a chance, please read this chapter “How to Drown in Three Feet of Water” from Nate Silver’s book “The Signal and The Noise”. That entire chapter is devoted to economic forecasting and why we fail at it.