These are all well-known companies. They are also very successful stocks since their respective IPOs. And they all have been rising with the market for last few years. Then what am I doing still buying them today?

I own all four companies for many years. You can see my portfolio here. So my 1Q purchases were not my first. I prefer to gradually build my positions over time. These most recent purchases were made when the market was down 10% and I was following my dry powder rulebook to take advantage of the drop.

Why these four companies? Are there any common themes here? Yes. First, they all have engaged and loyal customer base. Second, they are run by their founders/owners – with Apple being an exception but it is a much older company. And they all pioneered the industry segments they operate in – Apple with smartphones, Starbucks with coffee shops, Facebook with its social network, and Tesla with electric vehicles.

In this post, I won’t hash out my full investment theses on each. It would take too long. I will just focus on specific reasons for making today’s purchases – with a bit of my stock history mixed in.

Apple:

Apple:

I first purchased Apple shares in 2011 – the year when Steve Jobs took an indefinite medical LOA – and later passed away. By then, Apple had already upended the phone industry and had become the clear leader in smartphones. Over the years, I had kept on buying more shares as I built a better understanding of its business and customer base.

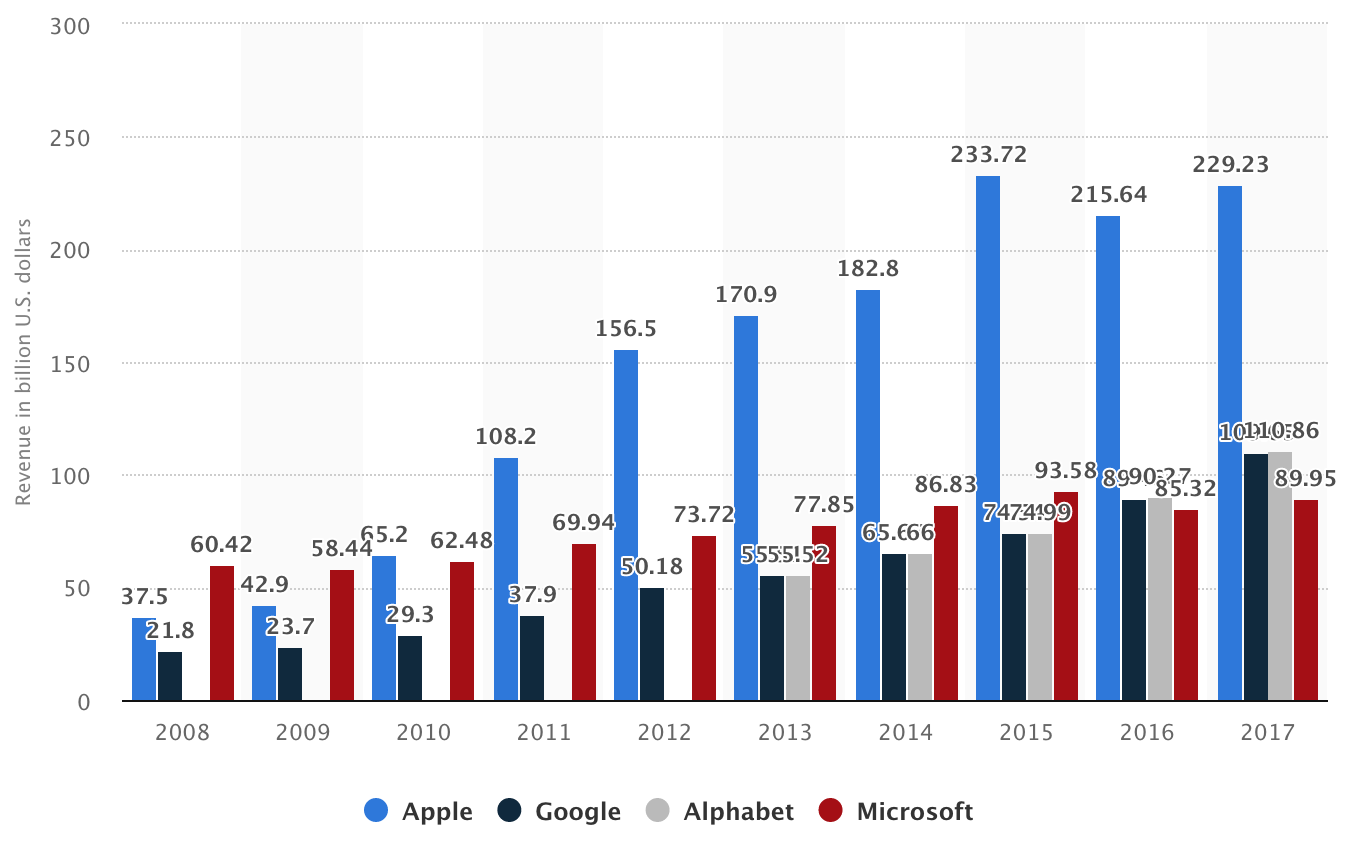

In 2011, Apple was priced at about 14 times previous year’s earnings. By 2013, the stock had dropped further while earnings kept moving up – yielding a bargain earnings multiple of 10. I bought multiple times that year and the following two years.

When Tim Cook was appointed CEO, the board had awarded him a generous stock options grant. The grant was supposed to vest automatically over the following ten years. After Apple stock dropped in 2013, Cook asked the board to change his stock grant from time-based vesting to performance-based conditional vesting. Any year that Apple shareholder returns fall to the bottom third of all S&P 500 companies, he would forfeit 50% of his stock grant. He also volunteered to not participate in dividend accruals.

To my eyes, this was a great sign. He wasn’t the founder owner of the company – yet he was thinking like a long-term shareholder with significant skin in the gain. As I had written before, I prefer CEOs who are significant owners too.

Berkshire bought its first stake in Apple in 2016. And it had continued increasing its position since then. It felt good to see Buffett (and his associates) recognize Apple as a great long-term investment – the same conclusion I had reached some five years earlier.

My latest purchase was made in February when Apple had dropped by more than 10% along with the rest of the stock market. At the time, its earnings multiple was 16x. This was quite a bit more expensive than when I bought in 2013/2014 at around 10x the earnings. But things had changed since then – the market feared far less about Apple blowing its innovation edge or losing its customer base. And at that price it was still cheaper than the market multiple.

Starbucks:

Starbucks:

I am a Starbucks shareholder even longer than Apple. I previously wrote about my Starbucks investment here. I first purchased shares in 2008 when investors were worried about coffee competition from McDonalds. Its founder/CEO had just returned from retirement to take over the reins. Its growth had slowed down considerably. And on top of it, the market itself was down so all stocks were priced cheaply.

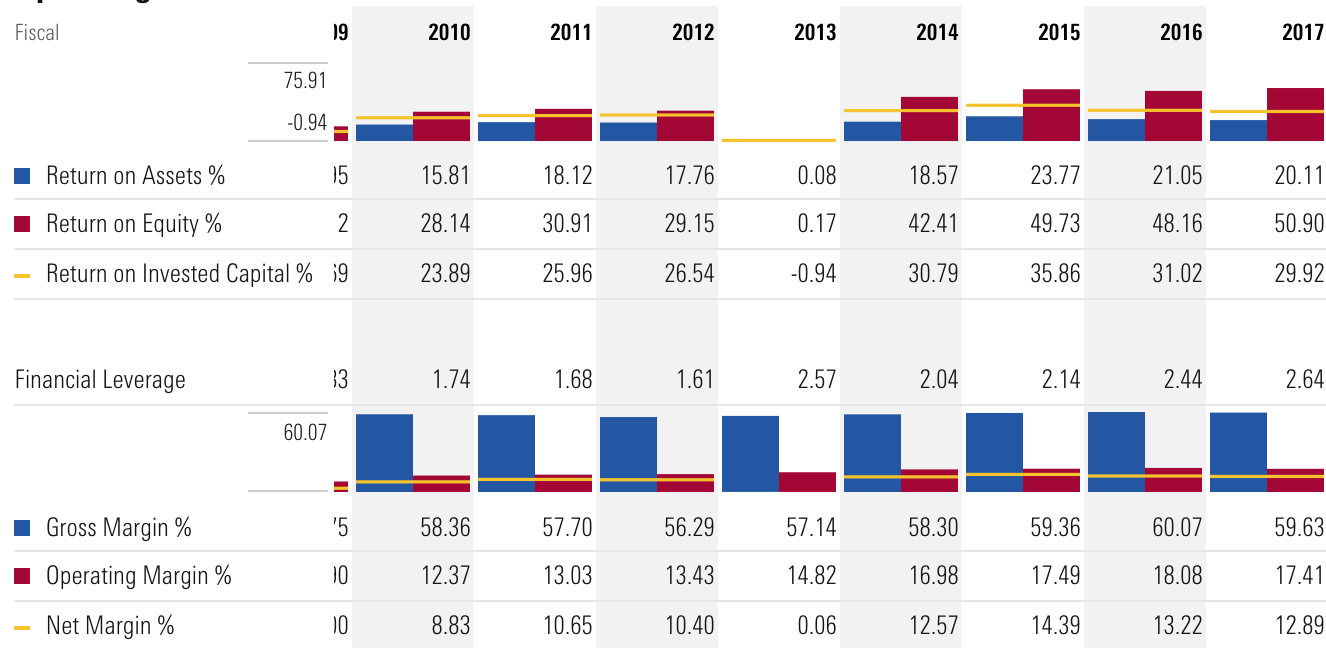

Starbucks was – and still is – a great business, run by capable management. Its long-time founder CEO – now its executive chairman – Howard Schultz owns 3% of the company worth about $2.3B. Since the time Schultz took over in 2008, the business has proven its durable competitive edge. You can see it in the numbers. Its Operating Margin has been consistently over 15% and Return on Investment Capital hovers around 30%.

Investors have two main concerns these days. First, that its same-store sales are slowing down. And then longer term, can it continue to grow given the current level of market penetration? I believe that these concerns are overblown. Its comp sales have slowed down in recent quarters, but management believes that is temporary. They are sticking to their full-year guidance. It also has several growth opportunities over the next few years – from further penetration in Asian countries to premiumization of its brand via Starbucks Roastery and growth in consumer-packaged goods.

My 1Q purchase was made in February at $56. Last I bought was 18 months ago at around $54. The stock had mostly flatlined since then even though the company consistently grew earnings over that time period. At the time I bought, it was down 14% off its 52-week high – about 9% down since January earnings announcement, and sporting a 22x multiple on forward 12-month earnings. Not cheap but reasonably priced for an outstanding franchise.

Facebook:

Facebook:

The first time I bought Facebook in 2013, it was just a few months after its IPO. The stock had fallen off by 50%. There were lingering concerns about how its advertising business would fare in the midst of consumers increasingly surfing on smartphones. Investors didn’t think that display ads on small phone screens would be effective. Well, Facebook proved the naysayers wrong on that point.

And then in 2014 Facebook made a whopper of an acquisition – WhatsApp at $19 billion. At the time I was a little puzzled by it – I didn’t understand the rationale behind it given that Facebook was already working on a similar in-house product, its FB Messenger. Four years later I could see why WhatsApp became a successful platform on its own. It caters to people who prefer to keep their messaging identities separate from their Facebook profiles.

By all accounts Mark Zuckerberg is a smart founder CEO. He owns a substantial portion of Facebook equity – making his interests in sync with ours. Early on, he brought onboard a seasoned operational manager in Sheryl Sandberg – and gave her a wide leash to run operations while he himself concentrated on long-term strategy. This reminds me of how Google co-founders had brought on Eric Schmidt to run the company in its formative years.

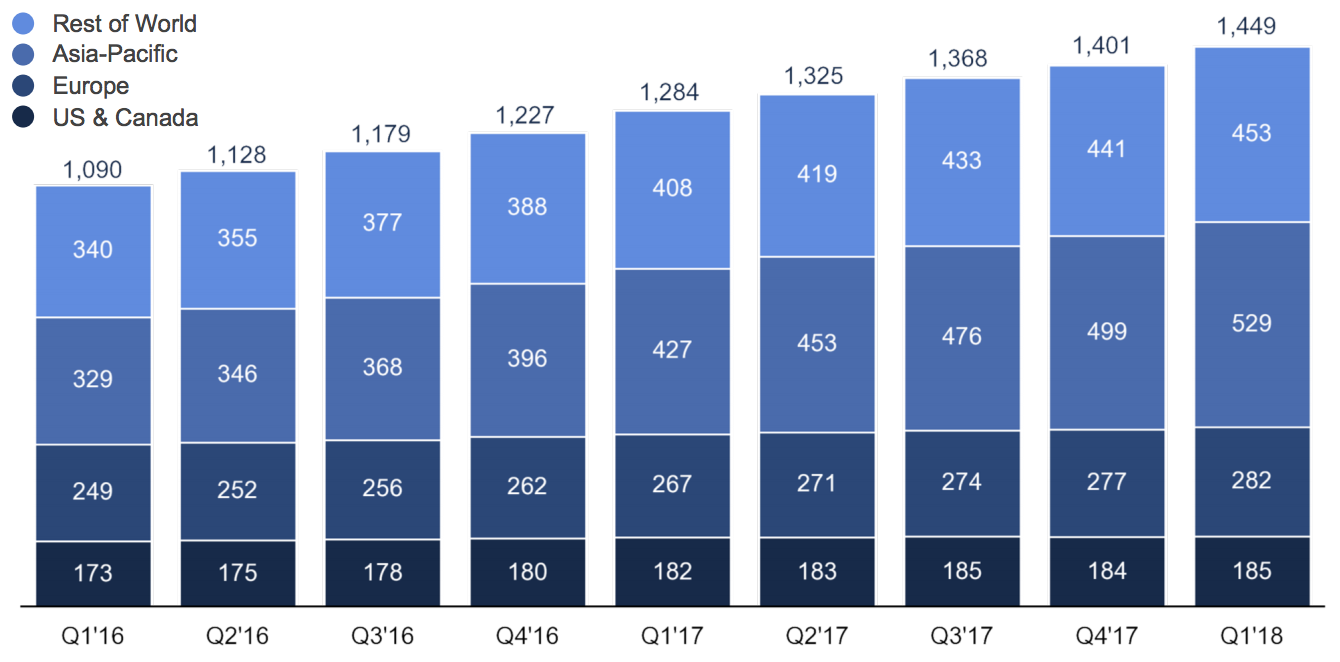

Facebook has clearly dug a wide moat around its business. Today it is very difficult for competitors to create an alternate social network of this magnitude – and convince people to switch. Google tried it valiantly for years with its Google Plus network – to no avail. We can see the growing network effect in how daily average users have risen consistently every quarter for last few years. Today, Facebook daily user count stands at 1.45 billion.

Thanks to its huge competitive edge, the Facebook business has the best of both worlds – growth and profitability. You can see it with 3-year average revenue growth of 48% and operating margins hovering near 50%. There is not much to dislike in FB numbers.

My last purchase was in February. The stock was down 13% from its 1-year high and trading at a reasonable earning multiple (24x forward earnings). I hadn’t bought in two years and I thought it was a good time to increase my stake.

Tesla:

Tesla:

Among the four purchases I highlighted in this post, Tesla stands out as the most speculative high-risk investment of mine. It does not lend itself to standard valuation techniques since it doesn’t have sustained cash flow or earnings. It operates as a niche auto manufacturer whose market segment (electric vehicles) is tiny (0.2% of all passenger cars today) and unproven. It also has much larger entrenched competitors with scale and existing infrastructure to crank out lot more cars.

So why am I invested in it? There are three compelling factors in making Tesla an interesting opportunity today.

- It has a visionary CEO with proven track record and significant skin in the game. With SpaceX and Tesla, Elon Musk has shown the world that he can break existing industry molds and carve out new market segments. Who’d have thought a decade ago that reusable rockets and electric vehicles will soon become commercial realities?

- It makes outstanding products that have attracted a fiercely loyal and raving customer base. Tesla car owners (full disclosure: I am one of them) remind me a great deal of iPhone owners from a decade ago. They love the product, are vocal about it, and serve as effective brand ambassadors for the company.

- Outside of EV manufacturing, the business has optionality in form of other adjacent business segments such as battery storage, solar power generation, and autonomous ride-hailing network.

But let’s not forget that there are significant risks to this business too. Any one of them could lead to outright failure. Such is the nature of a trail blazing business in an unproven market. In my mind, the biggest risk Tesla faces down the road is whether it could raise (or internally generate) enough capital to scale its production. Auto manufacturing is a very capital-intensive industry. I am not confident that Tesla could generate enough free cash flow from its existing product lineup to fund its production growth. Very likely, it will need to raise external capital – either debt or equity. When the next recession hits the economy (as it is wont to do from time to time), would it be too costly for Tesla to issue bonds? Or if its stock price tanks for some reason, would equity raise then become prohibitively expensive?

My latest purchase was made after I had time to study Tesla’s new CEO compensation plan. I liked it for two reasons. One, it confirms that Elon plans to stay at Tesla for foreseeable future. Second, it sets very aggressive performance targets that Elon has accepted. He won’t get paid a dime unless he meets at least some of the targets. While I am not sure if Tesla could ever achieve all the stated performance goals – 10x market cap increase, 21x revenue increase, 15x EBITDA, all within ten years – even if Elon achieves some of these targets, we the shareholders would have plenty to rejoice!

[…] that will survive and thrive throughout economic cycles. I wrote about some of them previously here, here, and […]