There weren’t many changes made in my portfolio last quarter. I did not start any new stock position – though I did add to three of my existing positions. I closed a couple of small stock positions where I took capital losses. There were no changes in my mutual fund positions. And finally, I donated one stock position to my charitable fund. Read on for details …

There weren’t many changes made in my portfolio last quarter. I did not start any new stock position – though I did add to three of my existing positions. I closed a couple of small stock positions where I took capital losses. There were no changes in my mutual fund positions. And finally, I donated one stock position to my charitable fund. Read on for details …

You can see from this previous post that I own more than 30 different stock positions. From my core holdings, I seldom sell any. I add to them over time whenever the market is offering a reasonable price for them. I follow their quarterly updates, but this does not usually result in any new selling or buying activity.

Moreover, I am always researching new companies. Every so often I identify a good business that is also reasonably priced. Whenever I find such an opportunity, I initiate a first position in it – usually a less than 1% stake. Over time as I begin following that business closely, I gain better understanding of not just the business itself but also the industry it operates in, its competitors, and its management quality. If I like what I see, I gradually up my stake in it. See the background on my individual stock positions here.

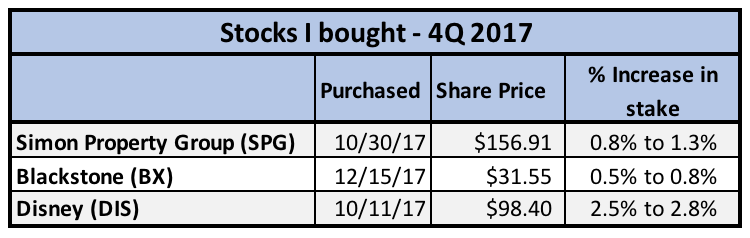

Stocks I bought:

The three stocks I bought last quarter – they all fall in the above-mentioned “gradually increasing my stake” bucket. Two of them – Simon Property and Blackstone – are relatively new positions. I first bought them less than one year ago. The third stock – Disney – is a long-term holding of mine – ten years and counting.

I outline my investment thesis for Simon Property further down in this post. In a future post, I will do similar analyses on Blackstone and Disney.

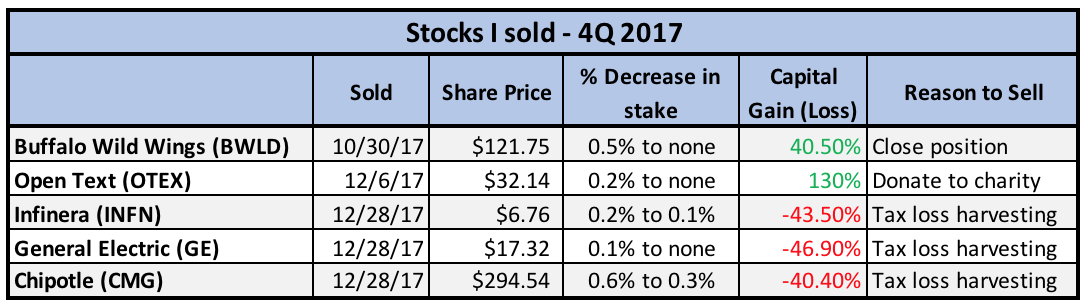

Stocks I sold:

I closed my position in Buffalo Wild Wings with 40% total gain. I had already reduced my stake in July. With this recent sale, I sold off the remaining shares. This final sale was prompted by Sally Smith’s retirement announcement, its long-time CEO. She had just lost a proxy battle with activist hedge fund, Marcato, for control of the company. I had great admiration for how she ran the restaurant chain for 21 years with excellent shareholder returns. With Marcato taking over the business, it was unclear where they will take the business next. It was time for me to take profit and look elsewhere!

As I explained in this year-end tax post, I had wanted to maximize my itemized deductions for 2017 before the new tax law took effect. So, I pulled ahead my 2018 charitable contributions into December through my Donor Advised Fund (DAF). The money wasn’t meant to be distributed before 2018 but, for tax purposes, I had donated the entire amount in 2017. To further save taxes, I went looking for a position that had considerable capital gain – and yet I was willing to close it out. I found it in Open Text (OTEX). OTEX is a Canadian I.T. services firm that I had bought in 2011. Although it had been a consistent performer for me over the years, I didn’t want to increase my position – nor did I have time to follow the business closely. By donating the shares in-kind to my DAF, I avoided paying capital gain tax on it.

As I explained in this year-end tax post, I had wanted to maximize my itemized deductions for 2017 before the new tax law took effect. So, I pulled ahead my 2018 charitable contributions into December through my Donor Advised Fund (DAF). The money wasn’t meant to be distributed before 2018 but, for tax purposes, I had donated the entire amount in 2017. To further save taxes, I went looking for a position that had considerable capital gain – and yet I was willing to close it out. I found it in Open Text (OTEX). OTEX is a Canadian I.T. services firm that I had bought in 2011. Although it had been a consistent performer for me over the years, I didn’t want to increase my position – nor did I have time to follow the business closely. By donating the shares in-kind to my DAF, I avoided paying capital gain tax on it.

The remaining three holdings – Infinera, General Electric, and Chipotle – were sold to harvest capital losses. I had significant capital gains elsewhere that I needed to offset. These positions were in taxable brokerage accounts. I may buy them back in February after waiting out the 30-day wash sales period. Stay tuned for my 1Q portfolio update in April.

Why I like Simon Property Group (SPG)?

SPG is a Real Estate Investment Trust (REIT) that owns and operates high-quality regional malls and outlet centers. It is the largest REIT in the world and twice as big as its nearest competitor. It also owns retail centers in Europe and Asia through joint ventures. All their properties are best-in-class – they garner highest rents and occupancy rates in the industry.

SPG is a Real Estate Investment Trust (REIT) that owns and operates high-quality regional malls and outlet centers. It is the largest REIT in the world and twice as big as its nearest competitor. It also owns retail centers in Europe and Asia through joint ventures. All their properties are best-in-class – they garner highest rents and occupancy rates in the industry.

I trust their management’s long-term focus, dedication, and good stewardship of shareholder interests. It’s a well-run business with long-tenured competent management. David Simon has been the CEO since 1993. Both the COO and the CFO have also been with the company since early 90’s. David Simon has significant “skin in the game” – he owns about 3.1% of shares worth $1.57B. His father was the co-founder of the company.

Simon is in early 50’s and has spent nearly his entire career working in the retail industry. You can tell from his quarterly earnings conference calls that he knows inside-out this industry. He gives detailed answers and I find him very open and forthcoming.

One could tell that David Simon understands business cycles. He’s made some shrewd moves over the years to take advantage of changing business environment. During the Great Recession of 2008, he bought Prime Outlets (outlet shopping center business) on the cheap. He also tried to acquire General Growth Properties (GGP), the second-best mall owner in the country, but backed off when other bidders emerged, and a price war ensued. By 2014 when the U.S. commercial real-estate market had recovered, he spun off SPG’s strip center and lower-quality mall properties into a separate REIT, Washington Prime Group (WPG). A timely move – those same lower-quality malls are suffering today due to department store troubles.

Executive compensation looks not only reasonable, but it is also tied to shareholder returns. Cash bonuses are paid on reaching yearly FFO (Funds from Operations) targets. Stock options are granted on the basis of how well the stock performs relative to the overall market and other REITs. In 2017, the CEO and other top executives voluntarily declined to take any cash bonus or stock grants because REITs did not do so well relative to the overall market. This doesn’t happen often but as I wrote in another blog post, I like CEOs who take voluntary pay cuts when the businesses aren’t doing so well.

The industry is in trouble, but I like Simon’s position in it. The market has turned sour on brick-and-mortal retail in the U.S. with mall operators taking the brunt. REITs in general have been pounded lately due to the prospect of higher interest rates. SPG has taken a beating in sympathy. From my perspective, this is like throwing the baby out with the bath water.

The US is probably over-retailed. And e-commerce is gradually taking a bite out of the overall retail. However, Simon only owns top-tier malls in key locations. There is virtually no new supply of malls in the country. While lower-quality malls and ageing department stores continue to be in trouble, it is my view however, that high-quality retail locations like Simon’s will attract rising retail stars. Consider for instance, that Amazon bought a brick-and-mortar retailer (Whole Foods) last year. Also note Warren Buffet’s backing of $1.5B 433-acre mixed-use retail development in North Texas called Grandscape. My investment thesis lies mainly on the premise that brick-and-mortar retail is not going away. There will be a fall-out (it is already happening) but the best of the crop will do fine.

The market is offering a good price. When I bought SPG at $157 in October, the market was valuing it at about 14.5 times LTM FFO (Last Twelve Month – Funds from Operation). FFO is REIT’s version of free cash flow. This is the cash earnings that belongs to the shareholders. SPG distributes some of it in form of dividends and use the rest for growth projects.

Since 2012, SPG has grown FFO by 7% and dividends by 12% annualized. Assuming 7% FFO growth for next 5 years and 3% thereafter, I can expect 11% annual return from the stock since I am only paying 14.5 times its current FFO. 11% prospective return is quite good in today’s low-rate and high-valuations environment. SPG may surprise me by surpassing these modest growth assumptions. CEO Simon has recently said that he likes to grow dividends by 10% annually.

Today Simon is trading at about 30% below its five-year high and 16% below its 52-week high. Mr. Market clearly does not favor Simon. But I like a good business when it goes on sale. So, I am building up my stake in it.

[…] earnings (like Amazon and Berkshire). Others return all their profits in form of dividends (like Simon Property and Blackstone). And there are some who return a vast majority of their profits in a mix of share […]