When you buy corporate bonds, you are told how much interest you will get and for how long. Your expected returns are spelled out by the company issuing the bonds. If you hold these bonds until they mature, you will get your initial investment back. There are risks, of course. What if the company falls on hard times? If a business is in trouble, you might not get your money back. This is called the default risk. What if interest rates rise after I bought that bond? That alone won’t cause you direct harm – you will still get your money back at maturity. But you will miss the opportunity to earn higher payments because your principal was stuck until the bond matures. This is the interest rate risk.

Apart from the risks mentioned, there is another opportunity cost associated with bonds. With bonds, the business tells upfront what it will pay you for the privilege of using your capital. If the business does well, it will eventually return your capital along with all promised interest payments. But that’s it! It won’t pay you any more than what it promised. Bond holders don’t get to participate in the business’ growth. That privilege is reserved for business owners. If you had bought shares in that business, you will own a share of its earnings for as long as you keep your shares. If the business flourishes, you will participate in the upside too.

How does a shareholder participate when a business does well? As business’ earnings increase, its stock price also increases. But this is a tenuous relationship since the stock price in the near term often depends on the prevailing mood of the stock market. Companies also use profits to buy back their own shares – this makes each remaining share more valuable. A more direct way is where management increases dividend it pays to the shareholders. As earnings grow, so does the dividends.

If you choose your stock investment wisely, you could become shareholder in a business that grows its dividend rate each year. You will get quarterly dividend payment that potentially increases each year for as long as you hold the shares. In effect, what you will be getting is a perpetual bond. A bond-like instrument that pays you quarterly and the coupon rate increases every year. Unlike regular bonds, this one does not have a maturity date. You could keep it forever. Of course, the return of the original investment is not guaranteed – unlike in a real bond. But rest assured, if the business grows its dividend regularly, its share price would also rise over time.

Here I will show you an investment I made several years ago that fortuitously turned into a perpetual bond for me:

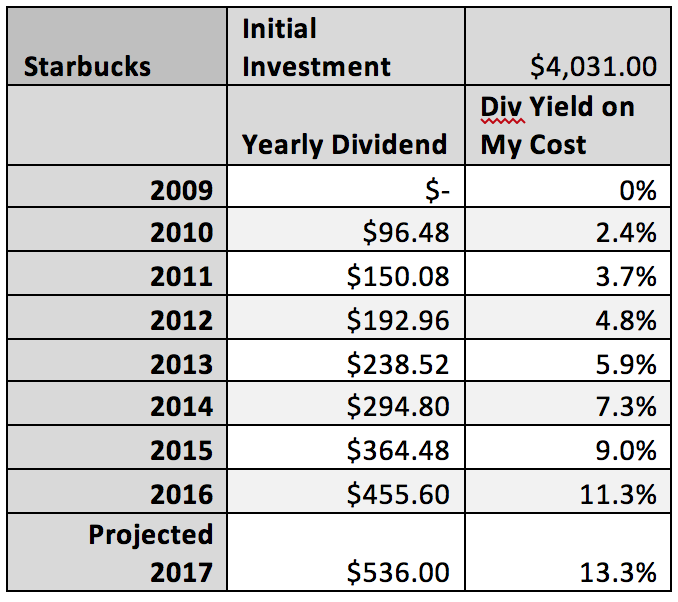

I bought 536 Starbucks shares in March and October 2009 at an average cost of $7.52 (split adjusted). Total amount invested $4,031. At the time, I thought the shares were quite inexpensive. There were concerns about rising coffee competition from fast-food chains like McDonald’s and slowing consumer spending. Back then, Starbucks did not pay any dividend. It started a dividend in 2010. In April 2010, I got my first quarterly payment of $26.80. As the business picked up with the economy, Starbucks kept on raising dividend every year. Today (August 2017), the same 536 shares pay a quarterly dividend of $134. This comes out to be 13.3% yield on my investment (4 times $134 divided by $4,031). In other words, my effective coupon rate on this perpetual bond today is 13.3%.

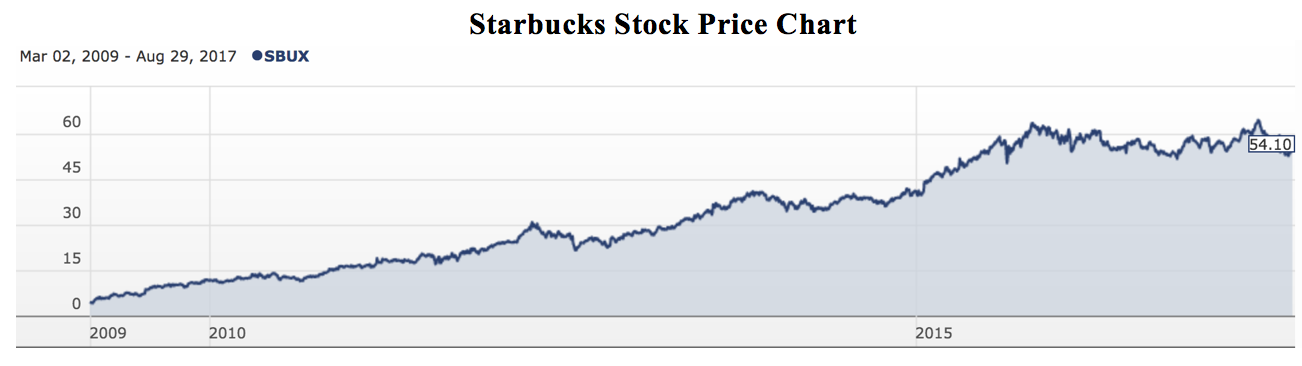

Here I am not even considering the unrealized capital gains due to the increase in Starbucks share price since then. I don’t plan on selling my shares any time soon even though one could argue that the shares are overvalued today. In 2008, Starbucks Trailing 12-Month P/E Ratio was about 14.4. Today, it is 27.3. It is certainly possible that the Starbucks share price could be cut in half (or more) from here. One could never be sure about the stock market behavior in the near term. But I don’t see the business cutting its dividend payment even when the economy takes a hit.

Its dividend payout ratio today is just 48% i.e. it pays out 48 cents dividend for each dollar of income.

When the stock market takes a turn for worse – which it eventually will – I will still be confident in Starbucks paying me dividend at the same level (if not higher). So my 13.3% effective coupon rate will still be good. If anything, I expect that over time, my coupon rate has nowhere to go but up. Starbucks, by all reasonable measures, is still a successful growing worldwide business. Why would anyone sell an investment that is yielding over 13% today even if a stock market crash were imminent?

If you are lucky enough to buy a strong growing business at decent price, it doesn’t make sense to sell it even when the market is over-valuing it. This is what Buffett meant when he said this:

- Warren Buffet, Berkshire Hathaway Annual Letter 1988

[…] corner and the business is very profitable, why would you sell? As I wrote in an earlier post, I bought some Starbucks shares at a bargain price in 2009. Today, I get double-digit dividend yield on those shares (on my […]