Most of my capital is invested in stocks. You can see my portfolio here. I keep some cash as rainy-day fund and also for my dry-powder strategy. In today’s low-rate environment, cash does not return much. Short-duration CDs yield 1% to 1.5%. One-year treasury bonds return about 2%. There aren’t many traditional investment options where I could invest this cash and get more than 1% to 2% annual return. Enter option based strategies where I take on a bit more risk but in return my potential profits are also higher.

I have two related strategies for generating higher yield but with limited principal risk: Protective Collars and Buffered Collars.

Protective Collar Strategy: Here I buy common shares of a public company and then simultaneously buy Put options (Protective Puts) and sell Call options (Covered Calls) on those shares. With the Puts, I am protected against any losses if the stock goes below the Put strike price. The Calls cap my upside gain but also fund the expense of buying the Puts. I also get to collect any dividend that the company pays on my underlying shares.

Protective Collars:

- Buy shares of a publicly traded company (whose options are also available) at prevailing market price (in increments of 100’s)

- Buy Put options (one contract for every 100 shares) at a strike price slightly lower than the current share price

- Sell same number of Call options at a strike price above the share price

- Both Put and Call options must have same expiration date

Perhaps the best way to explain this strategy is with a real-world investment. Here I show a Protective Collar position that I initiated in April 2017.

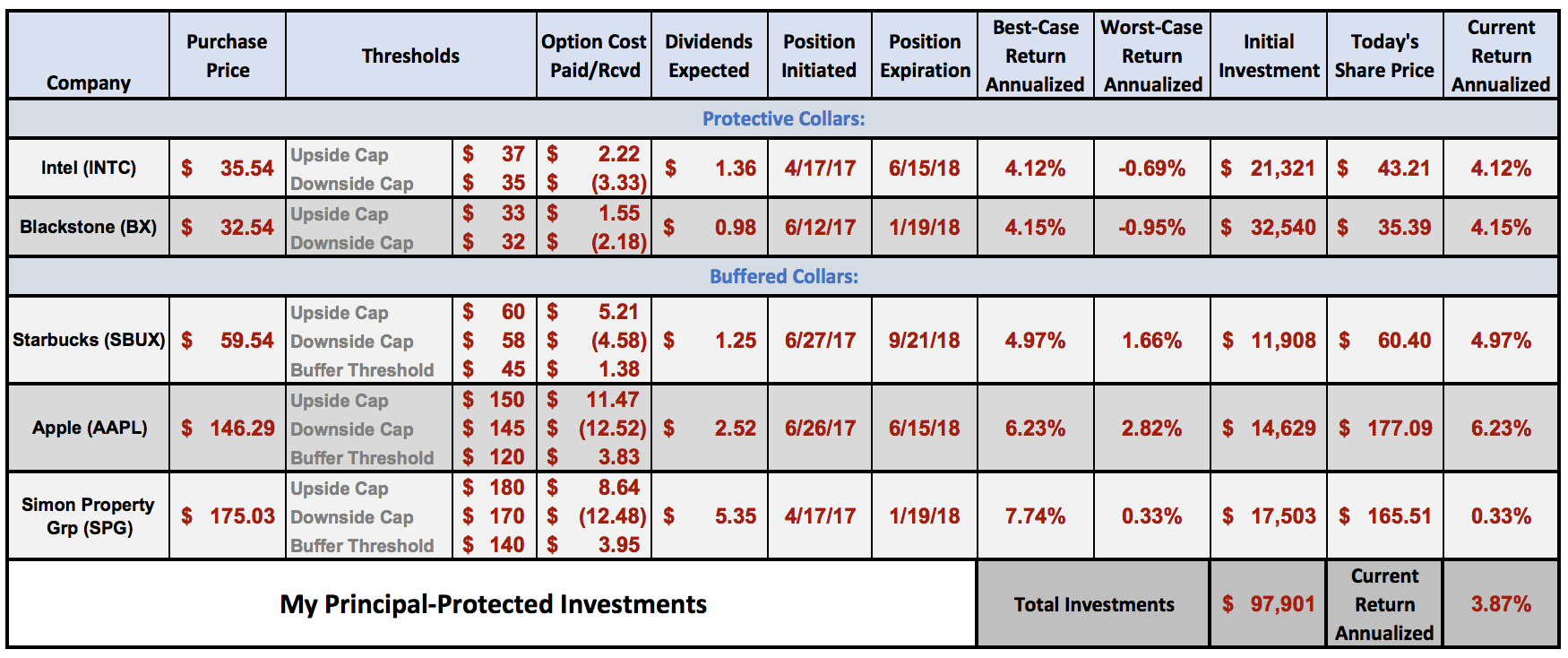

This position expires in June. I bought 600 shares of Intel stock at $35.54 and then proceeded to buy Protective Puts on them (6 contracts) at $35 strike price. So my downside risk is limited to $35. I also sold same number of Intel Calls at $37 strike – which caps my upside return. I paid $3.33 (per share) for Puts and received $2.22 (per share) for Calls. I also expect Intel to pay $1.36 in dividends before this position expires.

This position expires in June. I bought 600 shares of Intel stock at $35.54 and then proceeded to buy Protective Puts on them (6 contracts) at $35 strike price. So my downside risk is limited to $35. I also sold same number of Intel Calls at $37 strike – which caps my upside return. I paid $3.33 (per share) for Puts and received $2.22 (per share) for Calls. I also expect Intel to pay $1.36 in dividends before this position expires.

If Intel were to close above $37 at expiration, I would gain $1.46 per share ($37 minus my initial cost of $35.54) plus the dividends minus the cost of setting up the options. My annualized return in this case would be 4.12%.

Conversely if Intel closes below $35 at expiration, I would have a loss of $0.54 per share. My option costs and received dividends stay the same as before. In this case, my annualized return would be -0.69%.

Looking at the bigger picture, I am taking a small downside risk (-0.69%) to potentially gain a much higher return (4.12%). Compare this to a 1-year CD where my downside is zero but my gain is also limited to 1.5% to 2%.

Buffered Collar Strategy: I also use one other investment strategy where I can generate more upside return. It is very similar to the Protective Collar strategy except with the additional twist that my downside protection is no longer unlimited. My principal is protected up to an extent (buffer threshold). If the stock stays above the buffer threshold, the strategy works just like a Protective Collar. However any price drop below the buffer threshold would reduce my principal value by the same amount.

The mechanics of setting this up is identical to the Protected Collar except that in this case I also sell a second Put option at a lower strike price. The difference in the strike prices of the two Put options constitute the buffer.

Buffered Collars:

- Buy shares of a publicly traded company (whose options are also available) at prevailing market price (in increments of 100’s)

- Buy Put options (one contract for every 100 shares) at a strike price slightly lower than the current share price

- Sell same number of Call options at a strike price above the share price

- Sell same number of Put options at a strike price below the strike price of bought Puts

- All Put and Call options must have same expiration date

Here is a Buffered Collar investment I initiated in June last year with the Starbucks stock. I bought shares at $59.54. My downside cap is at $58 and the buffer threshold at $45. So, my principal is protected below $58 all the way down to $45. However, if the Starbucks stock closes at $40 at expiration, I will incur a $5 loss per share (buffer minus closing price). I believe it is unlikely that Starbucks will drop below $45 by Sept 2018. It would have to drop by 25% from today’s prices.

I bought shares at $59.54. My downside cap is at $58 and the buffer threshold at $45. So, my principal is protected below $58 all the way down to $45. However, if the Starbucks stock closes at $40 at expiration, I will incur a $5 loss per share (buffer minus closing price). I believe it is unlikely that Starbucks will drop below $45 by Sept 2018. It would have to drop by 25% from today’s prices.

I have about $100K of my cash invested in these principal-protected investments – see this table. About half of them are in Protective Collars and the rest are in Buffered Collars. At today’s prices, four out of my five positions are at peak return levels. The only laggard is the Simon Property Group which is at its worst-case level (still in black though). Two positions are expiring next week while two other positions will expire in June. And the final remaining position will expire in September. As my positions expire, I plan to open new positions with the released capital. Today, my investments are returning 3.87% annualized. This is a far better return than I could have expected from CDs or bonds. So far so good!

About half of them are in Protective Collars and the rest are in Buffered Collars. At today’s prices, four out of my five positions are at peak return levels. The only laggard is the Simon Property Group which is at its worst-case level (still in black though). Two positions are expiring next week while two other positions will expire in June. And the final remaining position will expire in September. As my positions expire, I plan to open new positions with the released capital. Today, my investments are returning 3.87% annualized. This is a far better return than I could have expected from CDs or bonds. So far so good!

Leave a Reply