CenturyLink (CTL), a large U.S. telecom operator, has just slashed its dividend by more than one-half. For the last two years, it had sported a mouth-watering double-digit dividend yield that reached as high as about 16% recently. It was no surprise that many dividend-seeking investors had jumped on this bandwagon lately. The dividend cut wasn’t what most investors were expecting though.

I am not an investor in CenturyLink even though I did take a look at the business late last year. Its unusually high dividend yield had caught my attention. Looking through its financial numbers, it was immediately obvious why the dividend yield was so high. It wasn’t because it had been growing gangbusters (revenue and EPS had flatlined in previous five years). Nor was it rapidly increasing dividends per share every year. In fact, the management hadn’t increased dividends in last ten years. The main reason for its high yield was its fast-declining share price. That wasn’t a recipe for long-term success. I didn’t investigate why its shares were going down. From what I had seen, it wasn’t a business I’d have been interested in buying in any case.

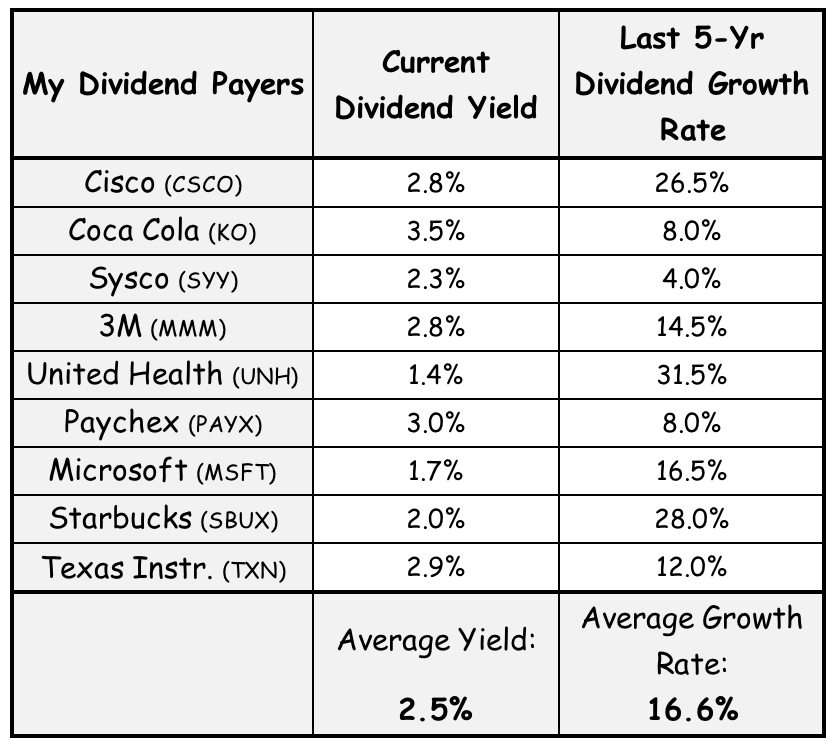

I believe that dividends can be an important factor in investing performance. I have stock positions that have been growing dividends for over a decade or longer. But my focus tends to be on a business’s dividend growth potential rather than its current dividend yield. Here are some of my holdings that have been consistently growing dividends.

Average dividend yield of 2.5% doesn’t look so impressive though. But that’s not really what I focus on. Current yield is only useful if I am investing new dollars. And current yields also fluctuate daily with share price changes.

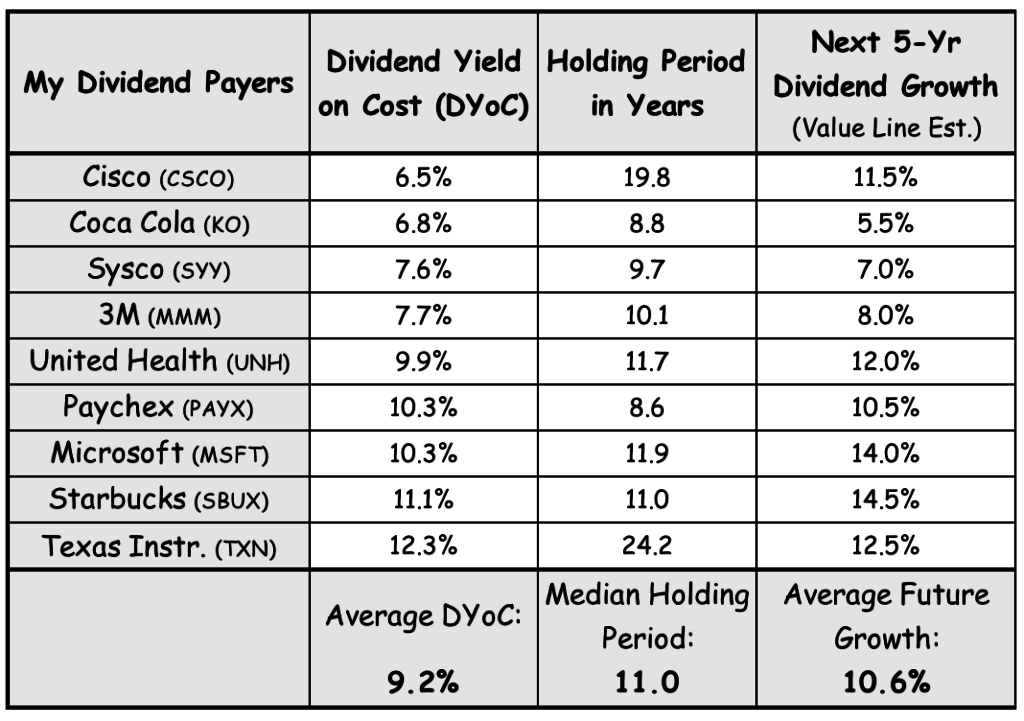

On the other hand, I prefer to hold on to my stocks for years, if not decades. So for those long-term holdings, I like to look at their Dividend Yields-on-Cost (DYoC):

Over time, as these businesses grow, they also increase dividends. One good thing about DYoC is that it doesn’t change with share price. It only takes into account how much I’ve paid for my shares and the dividend I am getting today relative to my original cost.

In a blog post last year (When stocks turn into perpetual bonds), I shared how my Starbucks position has a high dividend yield-on-cost. Here I show my other long-term holdings that have also proven to be excellent dividend payers:

Why my yield-on-cost is so much higher than the current dividend yields these stocks have? One, because I picked good businesses that have raised dividends substantially over time. Average dividend growth rate for these stocks have been more than 16% per year over the last five years. Another reason is that I have kept these positions (and on occasions, add to them) for a decade or longer—letting these businesses compound profits. Some of these businesses (Cisco and Starbucks, for instance) weren’t even paying dividends when I bought them the first time. They gradually switched from reinvesting all excess profits to paying dividend.

In December, I wrote about what dividend yield-on-cost I am getting on my commercial real estate holdings in this post: How am I investing in commercial real-estate?

Share buybacks get a bad rep these days. But consider this: If a business is paying dividend and it also buys back its own stock, investors get a double dose of return. How? Share buybacks reduce total number of shares that are dividend eligible. By virtue of reduced share count, total dividend allocation is then distributed over fewer shares. Thus the dividend yield would rise even if company doesn’t increase total dollar amount allocated to it. Either way, investors gain.

Returning to the previous table, here’s another consideration. When my dividend yield on cost is in high single digits (double digits in some cases), this gives me an extra incentive to stay invested in those positions even when share prices are down.

We know the stock market is unpredictable and volatile. When the market turns bearish, there is a good chance that my stock positions will go down quite a bit. Likely even cut in half or more. I pointed out in a previous post (A lesson from Buffett), even Berkshire share price wouldn’t be spared in those times of market turmoil. Berkshire shares had been cut in half on at least four occasions in last 40 years.

So when my current stock positions drop in half (or even more) due to market or economic conditions, I can reassure myself that my dividend yield-to-cost is still the same, these businesses will keep paying me dividends, and when market eventually turns around, they are likely to grow dividends once again. And eventually recover past share highs too.

Say when Texas Instruments (TXN) share price is down 60% due to some market drop (or an economic slump), I would still be getting my 12% dividend yield on those shares. No change. So long as its business stays healthy and generates adequate free cash flow. The management may decide not to increase dividends that year or stop share buyback to save some cash but it likely won’t reduce annual dividends. My 12% annual return is nearly guaranteed.

As readers of this blog know that I don’t focus exclusively on dividend paying companies. Last May, I wrote a blog post (Rise above dividends) where I made the case for investing in strong durable businesses regardless of whether they pay dividends or not. See my full portfolio here. In fact, some of the companies shown in above tables are not even among my top-20 positions. I look for good businesses run by reputable management— even better if managers are significant owners too.

So, focusing on my dividend yield at cost is a good thing—it keeps me stay grounded. But it only works for dividend generating businesses. What about those businesses that reinvest most of their profits. For them I focus on earnings yields. Not just any earnings but in Buffett’s terms, owners’ earnings. I’ll write more about earnings yield in a future post.

In a few years, I expect my Apple (AAPL) and Intel (INTC) holdings to also join this group of uber dividend payers. Both have excellent long-term prospects and growing dividends plus share buybacks. They both already generate healthy dividends for me but since I have bought more shares in last two years, my yield-on-cost is not nearly as high as those listed in the tables above.

Leave a Reply