BDCs, like REITs, are income producing investments. Investors don’t expect a lot of share price growth and only modest (if that) dividend growth. They make up for this lack of growth by generating high current yield. For instance, many BDCs today yield between 7% and 9%.

In my last blog post, I profiled BCRED, the Blackstone Private Credit Fund. Even though it is a new kid on the block, its sponsor, Blackstone, makes it an attractive investment possibility for those seeking income.

I also pointed out in that post that I did not invest in BCRED because it can only be invested in through an advisor directed portfolio. Instead, I opted to add another BDC in my portfolio. It is called OCSL, Oaktree Specialty Lending Corporation. Unlike BCRED, OCSL shares are publicly traded (on NASDAQ) so anyone with an ordinary brokerage account can buy.

OCSL parent is Oaktree Capital, a highly regarded asset manager whose co-founder is well-known Howard Marks. See my detailed profile of Oaktree here. Oaktree acquired this BDC in late 2017. Before that, it was still a BDC but managed by another asset manager, Fifth Street.

So, one reason to invest in OCSL is that it is managed by Oaktree. Oaktree in turn is now majority owned by Brookfield Asset Management (BAM), a well-known Canadian asset manager that I profiled here.

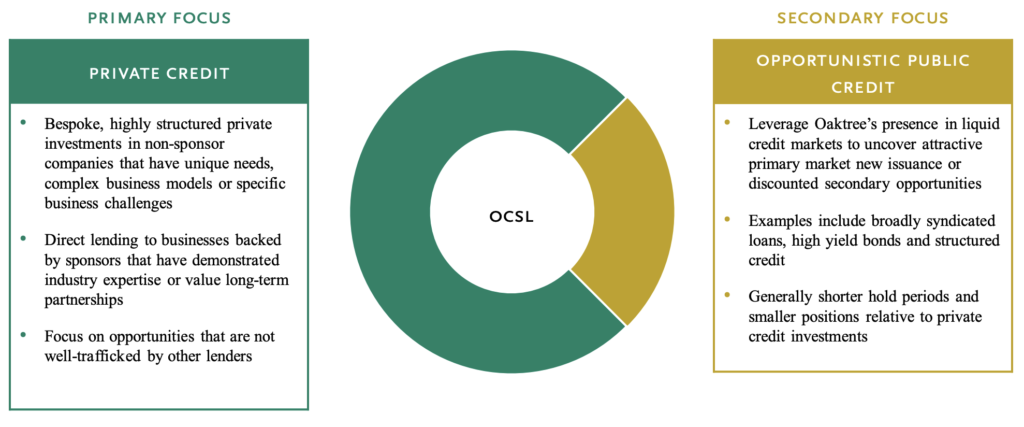

Another reason to invest in OCSL is that the current management has proven the quality and resilience of its portfolio during the last year’s recession.

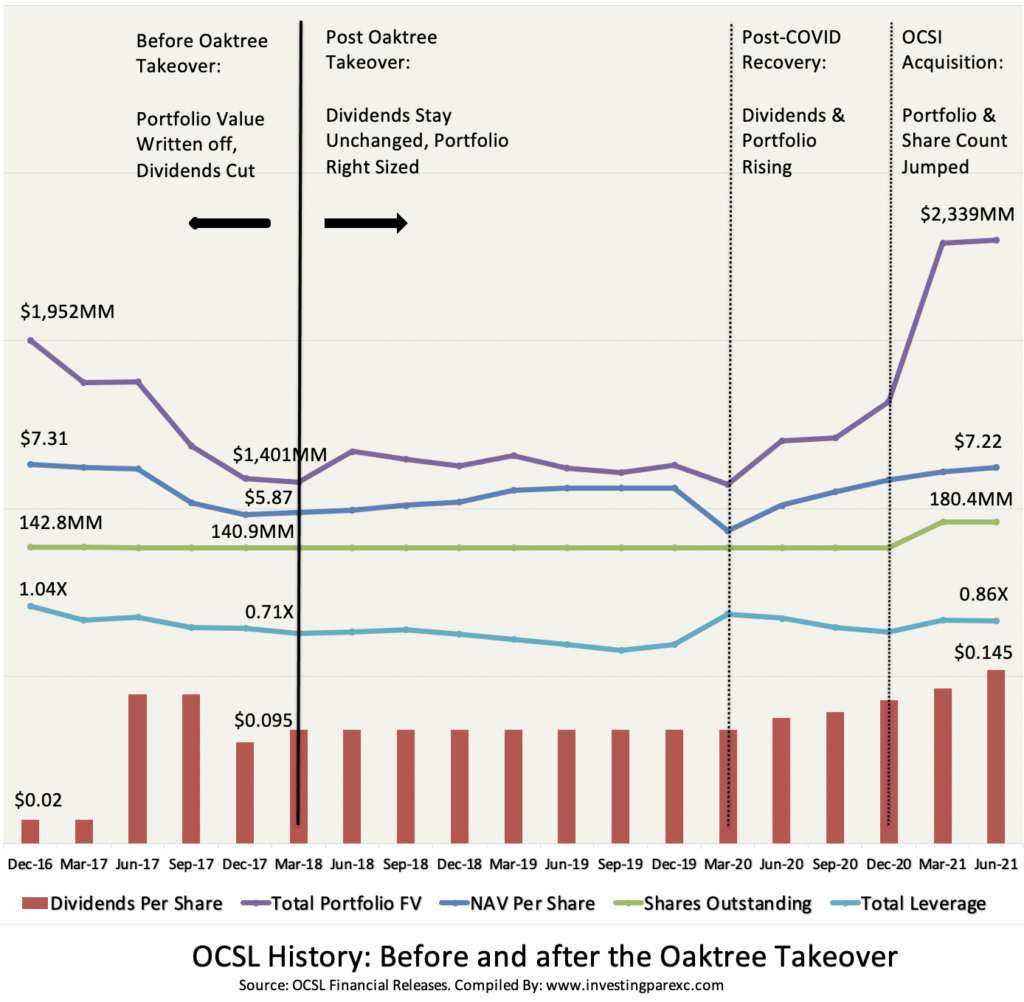

This chart shows recent history of OCSL, before and since the Oaktree takeover. Oaktree completed its acquisition in December 2017. In the previous two quarters, Fifth Street had tried to fix OCSL (or what was then called Fifth Street Finance Corp.) portfolio (but to no avail) by marking down its fair value (resulting in its NAV per share dropped by 20%) and reducing its leverage. Dividend per share was also cut by one-third. This BDC was in serious trouble before Oaktree offered to buy it.

Fifth Street’s management had not done a good job managing their two BDCs. They had several controlled businesses in their portfolios—valuations of those were always subject to management’s discretion. When Oaktree acquired both BDCs (yes, there were two, later named: OCSI and OCSL), there was much skepticism in the analysts’ community over the price it had paid and prospects for turning them around. An analyst said that a dividend cut was inevitable. There were concerns that Oaktree wasn’t known for direct lending. Distressed credit was what they did. Over time, Oaktree proved them wrong.

March 2018 was the first reported quarter under the new Oaktree management. Oaktree’s stated goals for the BDC were (a) to remove poor performing loans from the portfolio (it calls them non-core loans), (b) reduce financial leverage, and (c) use its underwriting expertise to add higher-quality credit assets. It largely succeeded on all three counts, though the results were not immediately obvious. From March 2018 until the pandemic struck (in March 2020), OCSL NAV would steadily improve (from $5.87 to $6.61) while the dividend stayed consistent. Leverage dropped too. During this period, Oaktree didn’t try to increase the size of the portfolio—it just focused on improving its quality.

The Covid pandemic put a lot of stress on all the middle market businesses, to whom OCSL catered. As a result, like nearly all other BDCs, OCSL also marked down the fair value of its portfolio. NAV per share also dropped. But unlike many of the BDCs, OCSL was not forced to cut its dividend. All the work that Oaktree had done since 2018—to right size the portfolio and reduce its leverage—paid off. Not just dividends, OCSL did not need to raise new equity at bargain prices either. The share count stayed the same throughout 2020, not diluting existing investors. Many other BDCs’ investors (and many REITs’ too) were not so lucky.

Post Covid low in March ‘20, OCSL did very well. Oaktree had taken advantage of the turmoil and put its considerable dry powder to work during the ensuing credit crisis. Since the March low, its NAV steadily grew every quarter. And even more telling is that it was also able to raise its dividend every quarter since then, while keeping the leverage reasonably low.

Then in March this year, Oaktree also merged its other BDC acquisition from Fifth Street (called OCSI) into OCSL. OCSI portfolio was mostly syndicated loans, not direct loans that OCSL offers, and hence were also lower yielding. In its merger pitch, Oaktree management touted two advantages: (1) Opportunity to further increase overall yield of the portfolio by rolling over syndicated loans into direct loans, and (2) increase OCSL scale and shares outstanding to make it more liquid and therefore more attractive to institutional investors. So, March ’21 was the first time in three years (or since the Oaktree acquisition) that OCSL issued any new shares. And further to Oaktree’s credit, with these new shares it acquired a fully functional portfolio that was already generating good income. Contrast this with a more common scenario where BDC would issue new shares to gain additional capital which in turn it would gradually invest in middle-market businesses. It takes time for a new portfolio to develop and start generating income, producing the infamous J-curve that is common in asset management industry. But OCSL investors didn’t need to wait for income growth. OCSI portfolio was immediately accretive, as you can see from the chart how dividend per share continued growing even with 30% jump in its share count.

Oaktree’s tie up with Brookfield opens up some new growth opportunities. Brookfield is a global powerhouse in real-estate and infrastructure asset management. It also has experience with private equity, though here it lacks the long-term resume of industry majors like Blackstone. One thing that Brookfield lacked was a solid credit investing strategy. And that’s why they took a stake in Oaktree. So far, Brookfield has mostly let Oaktree run its business independently. That was part of the deal. But it’s clear that over time Brookfield will use its vast distribution capacity to increase Oaktree’s reach. You can see this being played out over the next few months as Oaktree’s non-traded REIT will move under the Brookfield umbrella and change name to Brookfield REIT.

I suspect that OCSL could also benefit from Brookfield’s capital raising prowess. Someday, it could even be re-packaged as Brookfield BDC.

As I mentioned earlier, I ended up investing in OCSL, but not in BCRED. In either OCSL or BCRED case, I’d like to think that investors like me are betting more on jockeys, not so much on horses. Both Blackstone and Oaktree are trusted money managers. I am not sure I am capable of judging quality of their asset portfolios on my own, but I trust their underwriting skills. There are many other BDCs out there (both traded and non-traded kind). The S&P BDC index has 38 publicly traded US-based BDCs listed. I didn’t research any other BDC for potential investment. Though I suspect there are other good BDCs available in the S&P index. My short list of just two BDC candidates was inspired by the two asset managers who I knew well from previous research. Either OCSL or BCRED is a good choice for investors looking for high yield steady income (but slow growth), run by excellent managers. OCSL is now a small part of my portfolio.

Leave a Reply