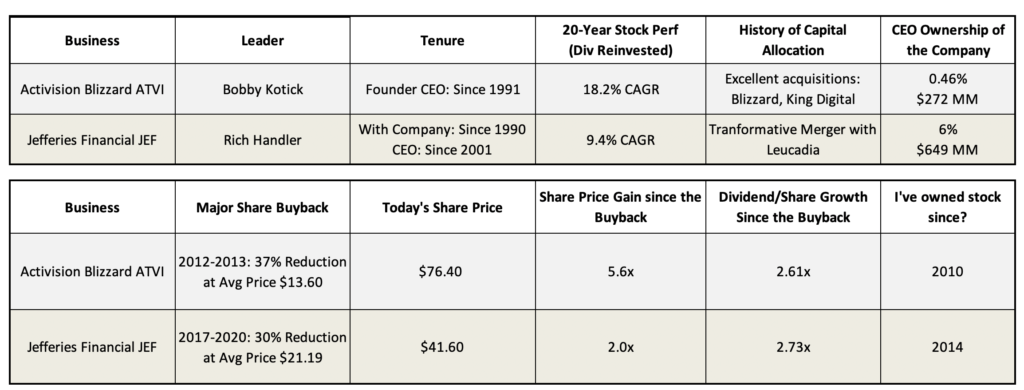

I own shares in two companies whose CEOs have been at the helm for over twenty years. These two businesses are not in the same industry. They don’t have much in common—one is in the video game business, and the other is in investment banking. As you can imagine, their business models and financials also look very different from each other.

Not only that these two CEOs are very long tenured, but both are also significant owners of their own businesses and excellent capital allocators to boot. Over the years, they have built their respective businesses practically from ground up—with organic growth and strategic acquisitions.

The two gentlemen are Bobby Kotick of Activision Blizzard (ATVI) and Rich Handler of Jefferies Financial Group (JEF).

In 2018, when I graded CEOs of the companies I own (see this post), I rated Bobby Kotick (of Activision Blizzard) as ‘Excellent’ in capital allocation on the basis of his strategic acquisitions of Blizzard and King Digital—two great video game franchises that thrived under Activision’s stewardship. At the time, I also rated Rich Handler (of Jefferies) as ‘Jury is still out’. Today, I would bump up Handler’s grade to ‘Pretty good so far’. It took a while for Jefferies to digest Leucadia assets and take advantage of its improved balance sheet but the results of the last two years have been outstanding.

In this post, I want to share two specific occasions where these two companies bought back (and retired) a hefty chunk of their own shares when those shares were trading at discount. One immediate effect of those repurchases was a significant drop in outstanding share count, resulting in increased ownership of the remaining shareholders (myself included). Our share of company’s earnings, free cash flow, and dividends increased proportionally—thereby raising our stakes in the business. A longer-term effect can be seen in subsequent dividend per share growth. With a significant portion of outstanding shares retired, the business could also afford to quickly increase per-share dividend as its business grows. We will see this effect in play in below charts.

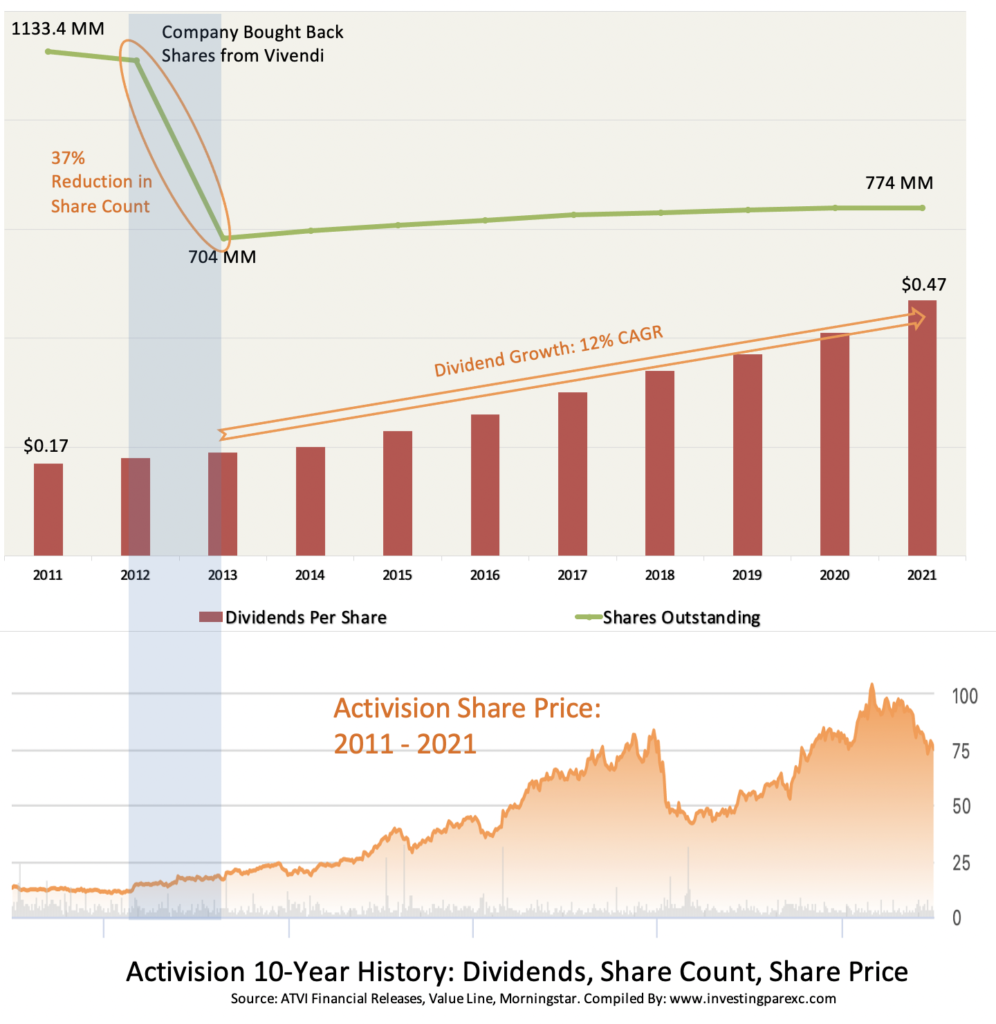

Let’s start with Activision Blizzard (ATVI). The company was founded by Bobby Kotick in 1991. [Technically, he acquired a dying business near its bankruptcy then.] He’s been leading it ever since. Thirty years and going. He’s 58 today. I have been a shareholder since 2010—eleven years into a much longer stake, I hope.

Activision is the leading video game developer in the world. Over the year, Kotick made several smart acquisitions to grow the business. He merged with Vivendi in 2008 to acquire the popular World of Warcraft game franchise. Five years later, he led the buyout of Vivendi’s stake in the company, turning Activision Blizzard into an independent business. In 2015, the company acquired King Digital, the maker of Candy Crush franchise, to get into mobile gaming. Along the way, ATVI also continued to invest in internal game development and in other third-party game developers like Infinity Ward, the original Call of Duty developer.

For this post, we focus on Activision’s buyout of Vivendi’s stake in 2013. Before that transaction, Vivendi had a controlling 52% stake in ATVI. To finance the purchase, Activision used a combination of cash on hand and newly issued long-term debt. When completed, the buyout resulted in 37% reduction in shares outstanding at the average purchase price of $13.60. Today, ATVI shares are trading around $76—a whopping 5.6x gain in eight years. See below chart.

Not only that the shares have grown more than five times since that repurchase, ATVI has also grown its dividend per share at a good pace. Since 2013, dividend per share has grown from $0.19 to $0.47, at 12% CAGR. In eight years, Activision managed to buy out one third of its shareholders at a low price and then rewarded remaining owners like me with double digit gains in share price and dividends. This is shareholder rewarding behavior at its best.

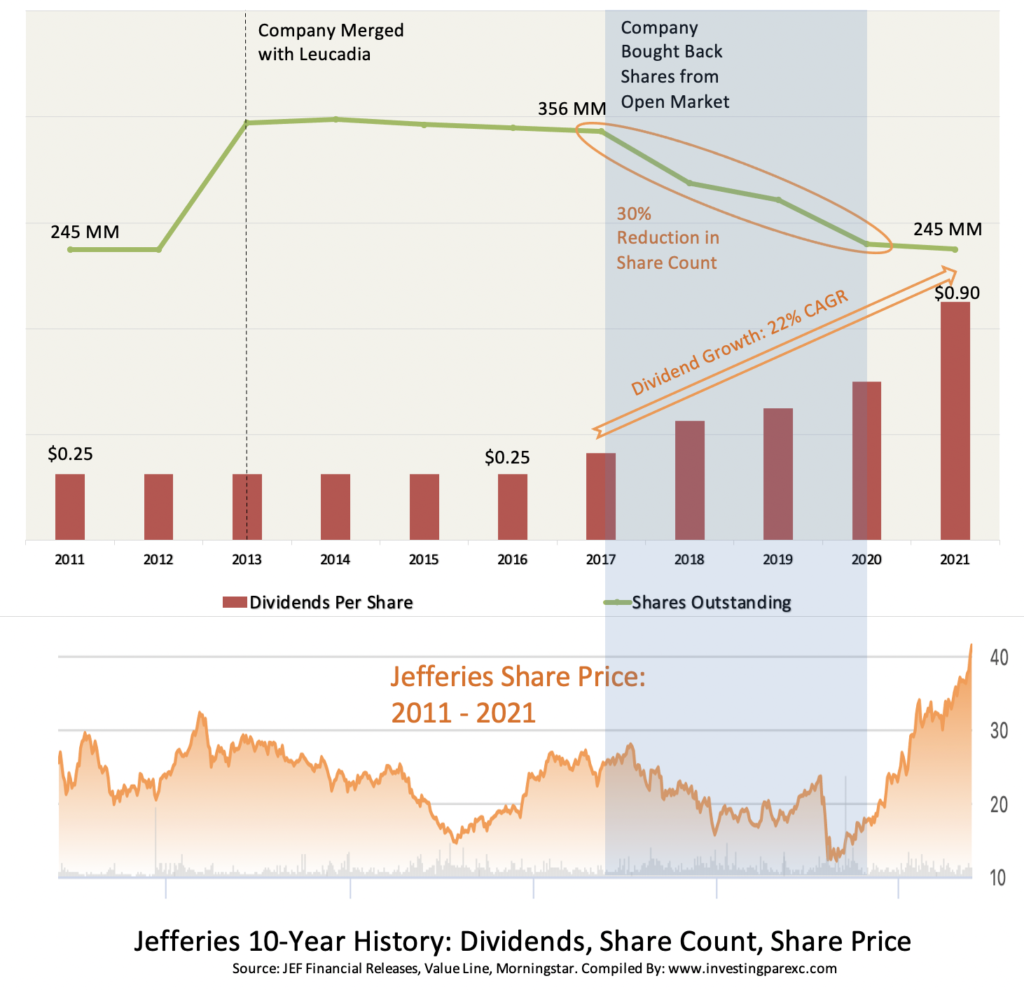

The other company I want to highlight is Jefferies Financial Group (JEF). It is an investment bank that also offers various other financial services to businesses. Unlike Activision, Jefferies does not lead in its industry. Though, it is ranked among top-10 in investment banking and M&A services. Rich Handler is its long-time CEO. He joined the company in 1990 and became its CEO in 2001. He is 60 today. I have been a Jefferies shareholder since 2014. At the time, it had just merged with Leucadia National (LUK), a business holding entity whose owners were retiring. This merger between JEF and LUK, completed in 2013, was a stock swap arrangement that resulted in a large jump in Jefferies outstanding shares. See the chart below.

Since then, CEO Handler has worked on streamlining the combined entity with increased focus on investment banking. Over the year, he divested many of Leucadia’s original holdings, all of them sold at premium to their cost bases. The resulting equity was used to shore up its own balance sheet and reinvest in its other business segments. The company continued to pay dividend at a fixed rate from 2011 to 2016. Then in 2017 as the company began to realize benefits of its business makeover, it started aggressively buying back its own shares. Between 2017 and 2020 as Jefferies stock range-traded between $15 and $25, Jefferies was able to cut its share count by one-third at an average price of $21. Today, about a year later, its shares are trading at twice that level. As we can from the chart, Handler also raised per-share dividend aggressively since 2017—at an annualized rate of 22%. Investors like me are well rewarded for holding on to our positions.

Activision stock has dropped about 25% from its peak this year. I increased my position last month. Conversely, Jefferies has continued to make new highs this year. I still like the business and I am keeping my position. But I am not inclined to add at today’s price. See my portfolio here.

These kinds of large share buyback opportunities don’t come about very often. But when such an opportunity knocks at the door, no one is better positioned to take advantage of it than a long-term minded business owner-leader. This is why I prefer to invest with them. It is also why I invest for a decade or longer. For patient shareholders like me, a long-term strategist CEO is always preferable to a short-term hired gun.

Leave a Reply