I have been singing the praises of Blackstone on these pages since 2018. I first wrote about the company in February 2018. Back then it was still a Limited Partnership (LP), and its shares were trading around $30. Then, about a year later, I wrote another post on it. Blackstone had just announced its conversion to a C corporation. Its stock was then trading in $40s. Last year I gave another update on the company. It was August 2020, and the shares were trading in low $50s. Since then, Blackstone stock has gone up another 2.5 times.

I bought Blackstone for income, and as a proxy for commercial real-estate. On both counts, it has done well. It has grown its average annual dividend by 35% since 2018. My current yield at cost is 12%. The shares have also grown much faster than the overall stock market.

There is a lot to like about Blackstone, the business. It is the market leader (in terms of AUM) in the private equity industry. It is the most recognizable brand, has been run by its passionate founder since the inception, and has long-term oriented owner-management.

Blackstone has also been growing its AUM at a rapid clip. Some of its fastest growing new offerings are designed for wealthy individual investors who may be seeking steady income. For instance, I wrote in detail about its non-traded REIT (called BREIT) last year.

This year, Blackstone has introduced a new non-traded investment product for individual investors, called BCRED: the Blackstone Private Credit fund. It is a Business Development Company (BDC), a provider of credit and equity to middle-market private businesses. See here to learn more about BDCs. Like a REIT, a BDC is also primarily an income-producing business that distributes at least 90% of its profits to investors.

BDCs are in a highly competitive industry, and there are many to choose from. MVIS BDC index lists 25 US-based BDCs that have market caps of at least $150MM each.

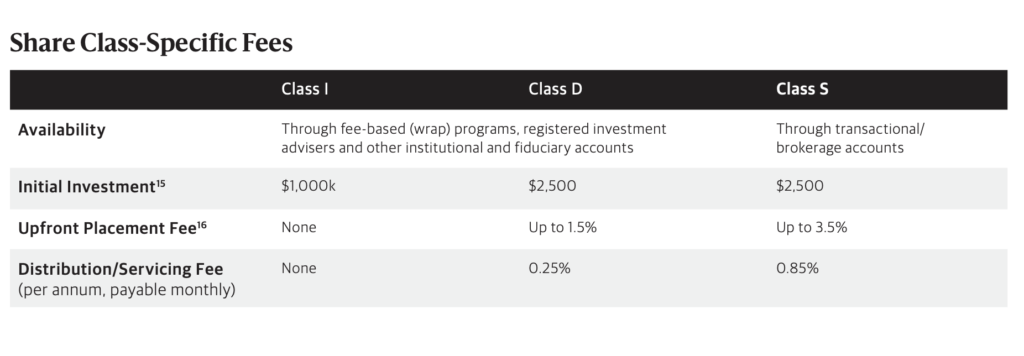

Why is Blackstone focused on non-traded investment products? First BREIT and now BCRED, both are public and registered products but not traded on any stock exchange. They are only available through the wealth management accounts of major broker-dealers or through registered investment advisors (RIAs). In either case, some upfront sales fees are charged when one makes an investment. Why Blackstone chose to go this route, rather than exchange-traded REIT/BDC is anyone’s guess. I suspect it’s partly due to their preference for wealthier individual investors who often work with an advisor. Those would also be more inclined (can afford) to stay invested for longer periods. As I pointed out in my BREIT post, these products have very limited quarterly redemptions that are not designed to move capital on a whim. Going through the advisor channel gives Blackstone better control over who their investors are and how to manage their expectations. It also gives these products the appearance of exclusivity (not everyone can invest in them).

There are also other well-documented benefits of non-traded REITs/BDCs, such as less perceived price volatility (since NAV is updated only once a month by the asset manager, rather than priced daily by market participants), better capital allocation decisions (limited redemptions mean less liquid short-term reserves), and less correlation with the stock market (market declines won’t necessarily bring down the NAV). All good things, but we must weigh them against the higher upfront costs paid by investors to get in.

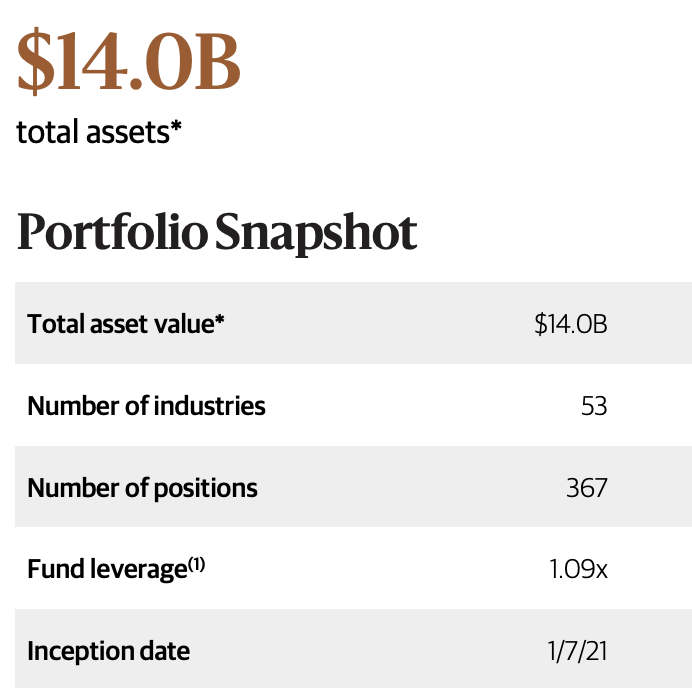

BCRED has a great start, much like BREIT had a few years ago. I’d have expected nothing less from Blackstone. BCRED has been collecting investors’ capital at a rapid clip: about a billion dollar every calendar month since its inception in January this year. CEO Steve Schwarzman said in Q2 earnings call that they are raising $4B every month between BREIT and BCRED. As of July, BCRED reported about $6.7B equity and $14B total portfolio size. This makes BCRED already about as big as the 3rd or 4th publicly traded BDC in the country. And it’s not slowing down.

However, this growth is from issuing new equity and therefore does not necessarily translate into per-share dividend growth for existing shareholders. Higher dollar income will be generated as BCRED successfully deploy its growing capital, but the total share count will also grow. This is generally the case with all REITs and BDCs since they are not allowed to retain profits for growth. See this chart where I showed how BREIT total distributions and shares outstanding both grew at the same rate during the previous three years.

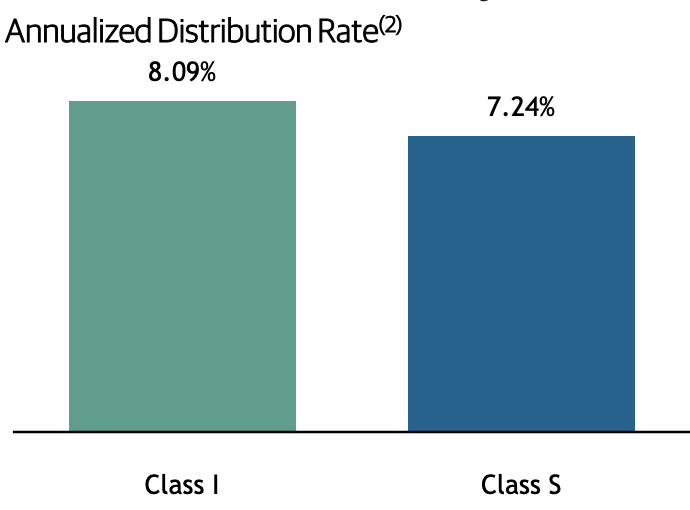

For this reason, I don’t expect BCRED to be able to raise its dividend yield much beyond what it is currently. Today, Class S and I shares yield 7.2% and 8.1% respectively. Most of its publicly traded BDC peers yield between 7% and 8%. As BCRED grows its portfolio, I also expect its yield to hover between 7% and 9%. For the same reason, I also don’t believe BCRED NAV per share would grow quickly either. Over the long term, I expect that BCRED investors can expect about 8 to 10% annual growth, but not much higher than that.

This would still be an excellent long-term return, given that BDC investors are in them for income, and not for high growth.

However, one question that comes to mind is why anyone would go with BCRED if there are other publicly traded BDCs available with similar yields. Being publicly traded has its own advantages after all. We won’t pay hefty upfront sales charges and redemptions (if needed) are quick and straightforward.

The answer, in my view, is twofold:

For one, as I alluded to before, BCRED being a non-traded BDC has the advantage of relative isolation from the stock market. Given that it is not offered on any stock exchange, the only two ways an investor can check its performance is how dividends are growing and what’s the current NAV per share. Both items are updated by the company once a month. If you need to sell shares, that can only be done once per month.

Secondly, BCRED’s management comes from Blackstone, one of the top global credit managers in the world. While BCRED does not benefit from an explicit guarantee from Blackstone, it is reasonable to expect Blackstone to manage BCRED well with strong risk management and underwriting performance. After all, Blackstone’s overall credit platform has about $163B of assets under management, and over 15 years of investing experience behind them.

This Blackstone edge can be substantial for investors who plan to hold on for a decade or longer. We want BDCs that not only pay good dividends but also be able to withstand severe market disruptions. Such as the one we experienced last year due to COVID. Even the strongest BDCs did not come out of that unscathed. Take for instance Ares Capital (ARCC). It is the largest publicly traded BDC. While it did not cut its regular dividend in 2020, it still ended up eliminating the special 2-cent “top-up” dividend it had paid in 2019. Another example is Apollo Investment (AINV) BDC whose parent Apollo Global is a well-regarded private equity manager. AINV was also forced to cut its dividend in 2020.

While there is never a certainty about future performance, BCRED does have a distinguished parent. We don’t know how well it would have performed in 2020 since it didn’t exist back then. But judging from its parent Blackstone’s long investing history in credit, I think it would have done fine. BCRED is a good investment vehicle for investors seeking income and those who have advisor managed portfolios. The upfront fees are high, but they are one-time, so in the long run, they won’t hobble performance.

In my portfolio though, I ended up not investing in BCRED. My reasoning was along the same lines as with BREIT (see this conclusion from my BREIT post). I don’t have an advisor directed portfolio, neither was I willing to open one just for this purpose. Still, I like the prospects of BCRED, and I will be rooting for it from the sidelines. I am a happy Blackstone (BX) shareholder, so I also benefit (albeit indirectly) from any Blackstone sponsored product.

What BDC, if any, did I invest in? I plan to write about it in my next blog post.

Leave a Reply