I admit that my stock portfolio is not doing well this year. Nearly all my major holdings are down by double digits. More than half are down by a third or more. Five are down by 50%. My top 25 holdings make up vast majority of my stock portfolio – about 88% of it. Here is the full table:

As you can see from the table, only two of my positions are in green this year: Activision and UnitedHealth. Both are anomalies in today’s widespread market downturn. Activision Blizzard (ATVI) is in the process of getting acquired by Microsoft, so it hasn’t trended down with the market. UnitedHealth Group (UNH) has also bucked the trend; managed health care businesses have been resilient in this bear market.

The rest of the stocks are all in a sea of red ink. Year to date, these top-25 positions are down by an average 29% since January. My overall portfolio is down by about 25%.

What am I doing to address this dismal performance? Not much. My positions are down because (a) the market is down and (b) there are lingering concerns about the global economy. I don’t expect my stocks to turn green until the overall market sentiment improves. Meanwhile, I have been buying more shares with my dry powder cash.

A year is too short a time frame to grade our stock holdings. Stocks are volatile assets and near-term performances reflect ongoing economic conditions. Longer term, I believe these top-25 businesses are on sound footings. I expect them to weather the current storm and do well once the economy gets going again. Some will do better than others, but they are all strong businesses with durable business models.

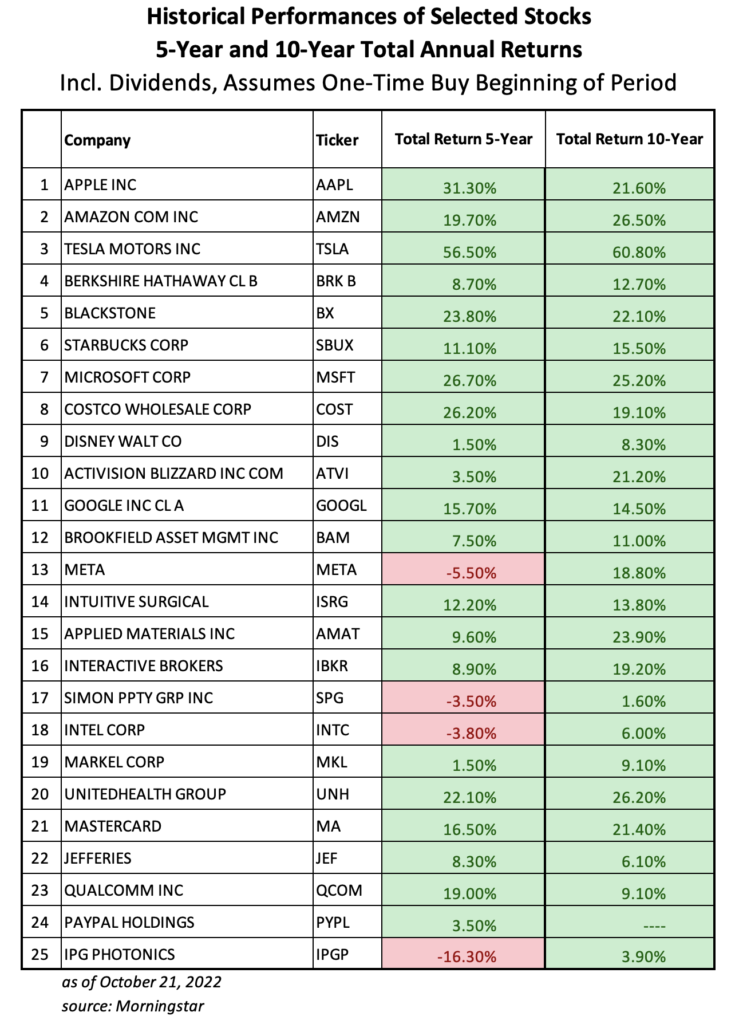

Take a look at their 5- and 10-year total returns (including dividends) in the table below. This assumes that investors bought shares once and held them for the following five and ten years.

These historical returns are not too shabby. Only four have negative returns in the last five years. And none of them caused any losses to investors who held them for ten years. It shows the quality and longevity of these businesses. Of course, these are theoretical performances, only achieved on paper by some hypothetical investor who buys once and holds them.

However, my own real-world portfolio results are even better. I have held most of these businesses for longer than ten years. In fact, my weighted average holding period is 12.5 years. So how have these stocks fared in my portfolio. Here are my real-world dollar-weighted performances:

As you can see, I’ve had great returns since I first bought them. There is just one company, Brookfield, where I haven’t generated profits (yet). But it is also my newest position. I only started buying its shares three years ago. It is too early to judge Brookfield since I buy for a minimum 5-year period. Combined, these 25 positions (considering first and all subsequent purchases I’ve made plus dividends collected) have resulted in 22.4% total annual return in my portfolio.

It’s true that past performances do not guarantee future results. I don’t expect these stocks to behave exactly like they did in the last five or ten years. But there are two takeaways from studying their history. One, for good businesses, longer term performances can easily outweigh any single-year declines. Two, high quality businesses ride through recessions and bear markets just fine. One example from my portfolio is Starbucks (SBUX). First bought in March 2008, it has gone through two severe recessions (2008 and 2020) and is in the middle of an on-going one. Yet, my average annual return today is a healthy 17.4%, notwithstanding that SBUX shares are down 26% this year.

Three years ago, in October 2019, I shared a list of stocks that I’d held for ten or longer. See this: Stocks Held for a Decade. Today, I have several new entries to add to that list. Barring any adverse changes in the industries they operate in, I expect that all my top-25 stocks that I shared above would eventually make it to that list. Good businesses are for keeps.

Good Day,

Thanks for your post. The information is very interesting. I’ve followed you for about 4 years, maybe a bit longer and know that you have moved away from mutual funds as your investing style evolved. May I ask if your performance these last 12 months or so wouldn’t have been better in a cadre of mutual funds run by a firm like Dimensional Fund Advisors? I like the fee structure ($0) of owning individual stocks and own some myself, but the work of Eugene Fama, Paul Merriman, etc, have convinced me against individual stock selection unless one has the time and mental discipline to master Ben Graham’s process of value investing. Not picking a bone with you, just wanted to hear your prospect. Your long term results are great. I just wonder how much risk you’re accepting with your approach vs the one I alluded to.

Thanks again for sharing.

Best,

Joel

Good question, Joel. I have indeed moved away from MF/ETFs to individual stocks gradually over the last 10-12 years. Five years ago, I still had some low cost index funds. Today, I have none in my portfolio. However, I’d never discourage someone from investing in low-cost index funds/ETFs. It is an excellent way of long term passive investing as I’ve said all along in my blog posts.

Why I am not indexing? I believe I can produce higher returns by picking individual stocks. Plus, I am trained in finance, enjoy business analysis, and have time required to do due diligence.

One year returns don’t really matter for long term investors. I showed my 3- and 5-yr IRR from Dec 2021. I did better than the S&P 500 on both counts. I will do another update in January. See this: https://www.investingparexc.com/2022/01/31/my-stocks-in-2021/

How much risk I am taking with this approach? This is difficult to quantify. Most efficient market theorist equate volatility with risk. Buffett & Munger vehemently disagree with this. They say risk is not how volatile one’s portfolio is. Risk is the probability of permanent loss. I am in Buffett camp on this. I aim to carefully pick businesses that are dominant and durable in their industries, thereby minimizing possibility of permanent losses.

Having said all that, indexing is a great way to save and invest for the future, no question. It is how I also built my 401K portfolio when I was working for a Fortune 100 company. In my view, the key difference between successful and unsuccessful investors is whether they’ve acquired a long-term buy and stay invested mindset, not so much if they invest in funds or individual securities.

Best of luck in your investing endeavors!