Activision Blizzard (ATVI) is getting acquired by Microsoft (MSFT). Activision shareholders will be paid $95 per share in cash if the proposed acquisition is approved by various antitrust bodies worldwide. I am a long-time shareholder of both Activision and Microsoft (13 and 15 years respectively). I think that Activision Blizzard’s industry-leading franchises (like Call of Duty, World of Warcraft, Candy Crush) will do well under Microsoft, and possibly even get a leg up on its rivals. With Microsoft’s deep pockets, its other AAA game franchises (e.g. Halo, Minecraft), and a captive gaming console (Xbox), Activision games can possibly get to a much larger scale than if it stays independent.

So, as a Microsoft shareholder, I like this transaction. However, given Microsoft’s already huge scale in enterprise, consumer, and cloud software, incremental revenue/earnings from Activision won’t move the needle much. I believe this move is more about deepening Microsoft’s moat and increasing its consumer brand loyalty.

Conversely, as an Activision shareholder, I am not so thrilled. I believe Microsoft is getting Activision for cheap. It’s a quality franchise run by excellent long-term minded management. While $95/share by Microsoft is a reasonable offer (peak share price was $103 in February 2021) in today’s market, Activision has good prospects in continuing to grow its game franchises at above-market rates over the next few years. I’d have happily stayed on as an Activision shareholder if given an opportunity. I think the market would value Activision’s growth higher if it were trading as an independent business.

Last year, I profiled Activision founder-CEO Bobby Kotick. I wrote about his excellent capital allocation moves with Blizzard and King Digital acquisitions. I also highlighted Kotick’s timely buyout of Vivendi’s stake in 2013 which resulted in 37% reduction in shares outstanding. From 2013 to 2021, Activision managed to buy out more than one-third of its shareholders at a low price and then rewarded remaining shareholders with double-digit gains in share price and dividends.

In that blog post in October, I wrote that I have been a shareholder for eleven years and hoped to stay in much longer. Today, that seems unlikely. Activision stock is trading at around $75 (20% discount from the offer price) which means the market thinks there is a chance that this acquisition may not go through. On the other hand, some key investors (Warren Buffett has been buying Activision shares since the deal was announced) believe that this merger will eventually go through. For now, I am also keeping my Activision position (with a tax saving twist as described below). If the transaction completes, ATVI shares should trade about 20% higher. If it fails, I will just hold on to my Activision shares.

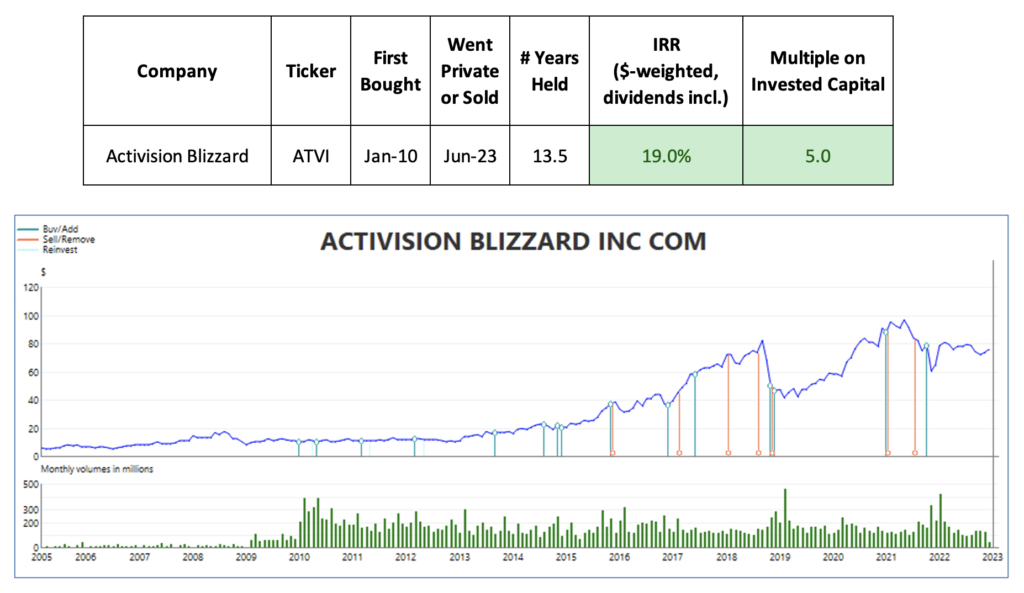

If this acquisition closes at the current offer price by mid-2023, my dollar-weighted return would be about 19% IRR. This takes into account all my incremental purchases/partial sales since January 2010 (when I first purchased ATVI) and annual dividend payouts. Total MOIC (Multiple on Invested Capital) would be 5x over a period of 13.5 years. See this chart.

Unlike Mr. Buffett, I don’t do merger arbitrage. I just don’t think I have any information edge in assessing probability of success in M&A transactions. But I do have fairly significant unrealized capital gains locked up in Activision shares (as you can tell from the table above). To reduce my potential tax liability in case this deal does go through, I have moved a portion of my position (shares that were in taxable account) into my Schwab Charitable DAF (Donor Advised Fund). I was due to make a charitable contribution this tax year and this Microsoft deal came just in time. By moving those shares into my DAF, I am able to take a tax deduction of the full amount (current market value of the shares) and not pay any capital gains tax on them either. What about that potential 20% further price gain if this deal goes through next year at $95? Not to miss out on that, I also bought same number of Activision shares elsewhere in my portfolio. If this deal consummates in 2023, I will still partake in that $75 to $95 share jump (albeit it will be short-term capital gain).

This is a risk we individual investors face. Whenever public company valuations are down like they are today, we face prospects of a deeper pocketed buyer scooping up good businesses cheaply. We don’t get fair price for our stocks and unfortunately there is not much we can do to prevent this from happening. Perhaps a business run by its founder who still has substantial stake in it would be able to resist a hostile takeover. In Activision’s case, even though CEO Bobby Kotick is its founder, he does not have a very large current stake (less than 0.5%) in it.

In my years of investing in individual stocks, I have faced such go-private situations a few times before.

In August 2017, Amazon acquired Whole Foods Market (WFM). I was a WFM shareholder back then. I was forced to sell my WFM shares then, resulting in a small capital loss to me. I wrote about that transaction four years ago here. I was also an Amazon shareholder back then (and still am). At the time I wrote that I picked up more Costco (COST) shares with the capital released from the WFM sale. I suspect that my Costco share purchase then has more than made up for the lost opportunity of holding on to my WFM shares. Since June 2017 when Amazon announced its WFM takeover, Costco share price has nearly tripled, plus its quarterly dividends.

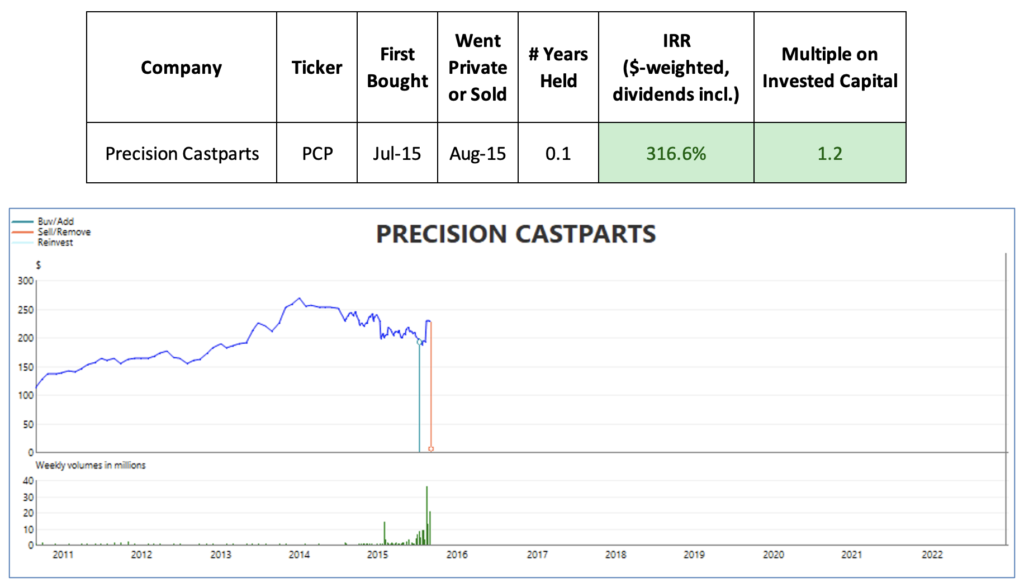

Precision Castparts (PCP) is another company whose shares were taken away from me in August 2015. This time again, the acquirer was a company I also owned, Berkshire Hathaway (BRK.A, BRK.B). I had only owned PCP shares for barely a month before it announced the acquisition. I made a small profit on that transaction, as seen in the chart below.

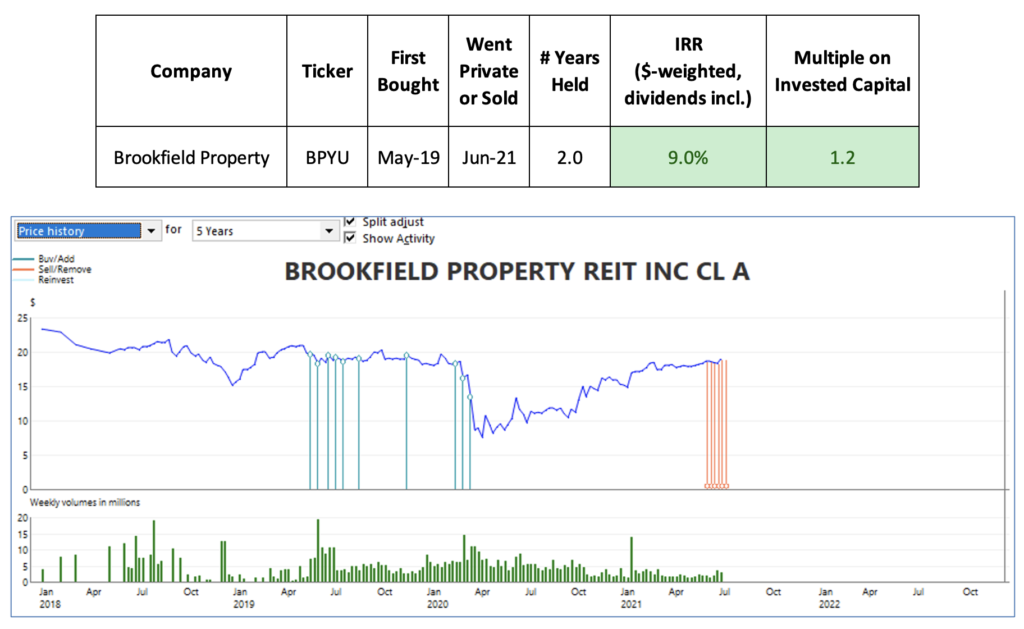

I also owned a public REIT, Brookfield Property Partners (BPYU) for two years before it was taken private in 2021. I previously wrote about BPYU here and here. I had owned BPYU for two years before it went private. This time, the acquirer was its own parent company, Brookfield Asset Management (BAM). As I wrote in June 2021, this wasn’t my desired outcome. I was happy collecting a nice dividend from BPYU while waiting for its share price to recover. However, that was not to be. For the two years that I had owned BPYU, I made about 9% IRR.

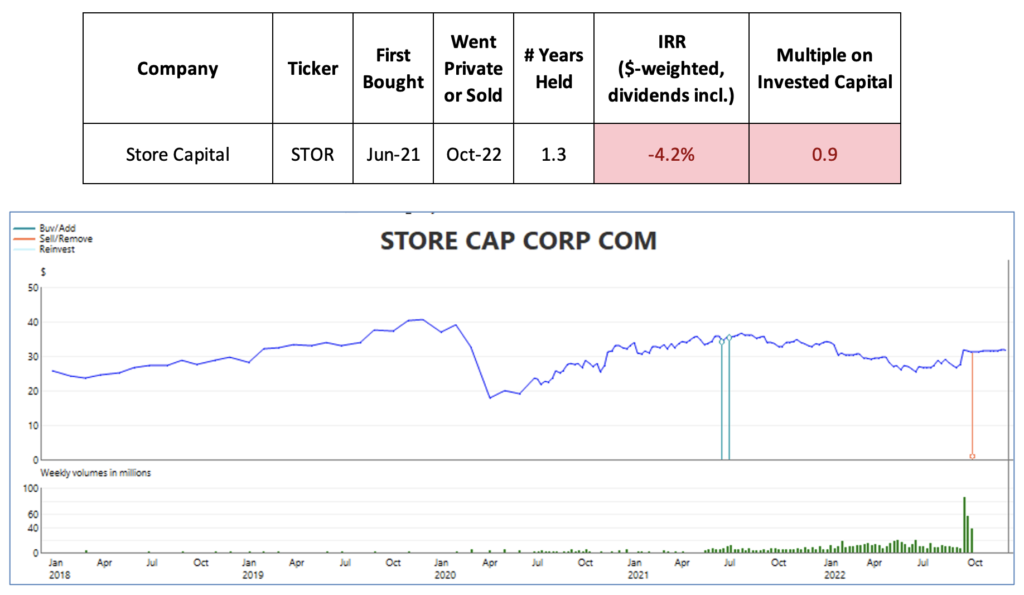

As a follow-up to Brookfield Property going-private transaction, I wrote another post where I shared names of five companies that I had bought from the money received with BPYU sale. One of those five companies was another REIT called STORE Capital (STOR). See my profile of STOR here. Just over a year later (September 2022), STORE Capital also announced that it is going private. This time, the acquirer was a sovereign wealth fund, GIC. My position lasted barely 16 month and resulted in a small capital loss for me. STORE Capital was cheap when I bought it in 2021 but went down further this year as the rest of the REIT market also tanked. I was confident in the quality of STOR’s net-lease real-estate assets and knew that its share price will eventually recover (while I continue to collect quarterly dividends). But it didn’t quite work out for me, as there were other well-funded buyers who also thought highly of STOR’s properties.

These were all lost opportunities for me. I can only speculate how these positions would have fared in my portfolio if I were able to keep them longer. We become stranded investors when we are forced to give up our ownerships in good businesses. It is a risk that does not get discussed often.

I’d be remiss here to not mention one big near-miss I had in 2018. I was lucky that that go-private transaction eventually fell through. Else I would have been a forced seller one more time. I am talking about Tesla’s 2018 go-private move. In this case I don’t need to speculate — I can calculate exactly what I might have missed if that transaction had taken place. More on this in my next blog post.

Leave a Reply