One of my all-time favorite authors on investing is Howard Marks. He is a practitioner (not an academic) but also has a way with words. It’s not just me—Marks’ memos are widely read. His first book, The Most Important Thing, was a best-seller. His memos—which he regularly publishes—are freely available online to anyone who cares to read them.

I have mentioned this in a previous blog post: I prefer learning from investors who are in the practice of investment management. People like Ken Fisher, David Swensen, and Warren Buffett. Howard Marks is also one of them. He is the co-founder of Oaktree Capital Management, a highly regarded global asset manager. Oaktree Capital is a public company. Its stock trades on NYSE with the stock ticker OAK.

In March this year, Brookfield, a large asset manager, announced its plan to acquire most of the Oaktree. While I had never owned any shares of Oaktree or Brookfield, the news of the acquisition intrigued me enough to take a closer look. I knew that Oaktree is majority-owned by Marks and his co-founder Bruce Karsh. So the acquisition could not have taken place if the two weren’t interested in selling the company. From the press release, it was clear that this wasn’t a hostile takeover either. It turns out that it was a long-term deal where Brookfield would initially become the majority owner, but Oaktree founders will have independent control of its operations. Oaktree founders would then gradually sell their remaining stake to Brookfield over the following ten years. Brookfield could become the 100% owner of Oaktree by 2029 at the earliest.

Oaktree wasn’t in any trouble and its owners weren’t in hurry to sell out. The two co-founders continued to have full operational autonomy for another ten years. This Brookfield deal, in reality, was their succession plan, which makes sense given that Marks and Karsh today are 73 and 63 respectively.

This led me to Brookfield. Who were these guys? I didn’t think that Howard Marks would hand over his company and his clients to just another asset manager. This turned out to be my lead into the Brookfield opportunity.

Brookfield Asset Management (BAM) is a highly regarded and one of the largest alternative asset managers in the world. Somehow, I had never paid attention to it until this Oaktree deal surfaced. As I checked my old notes, I also realized that Tom Gayner—another investment manager I closely follow—had brought up his long-time Brookfield ownership in a Markel shareholder meeting that I attended two years ago. Turns out that Markel Corporation, where Gayner is the co-CEO, owns Brookfield shares for a very long time.

Brookfield passes my sniff test easily. It is no fly-by-night operation. It is a well-known name in its industry, has a strong market position, and has been around for decades. If anything, it is somewhat embarrassing to admit that I didn’t know much about it until now. In any case, Brookfield appears to check all the boxes when it comes to the key traits that I expect in a promising investment. Its business model and scale are such that it can fend off most competitors—in other words, it has economic moat. It also has long-term oriented shareholder-friendly management with significant ownership in the business.

The industry Brookfield operates in is alternative asset management. Specifically, it is known for managing real-estate, infrastructure, renewable energy, and private equity assets for institutional clients. With Oaktree under its wing, it now manages distressed credit securities too.

I’ve previously written about alternative asset managers in my blog post on Blackstone last year. Brookfield and Blackstone are competitors. Both are considered the top dogs in the industry. Both are similar to each other in respective business models. However, there are two things that sets Brookfield apart from Blackstone:

(1) Brookfield invests its own capital into the assets it manages. This is unlike Blackstone which runs a capital-light model and distributes most of its earnings to the shareholders every quarter.

(2) Unlike Blackstone whose private funds are only accessible to institutional-level investors, Brookfield’s funds are also available to ordinary individual investors (people like us) through its publicly-traded partnerships (PTP).

Since Brookfield retains a majority of its profits to reinvest in its growth, you can see that its dividend yield is much lower than Blackstone’s—1.3% versus 3.2% today. It’s not an investment candidate for those seeking high dividend returns. But I am fine with this since the management has proven they are good capital allocators. In a blog post last year (Grading CEOs as capital allocators), I wrote about Reinvesters and Dividend Payers. Both types can be good businesses to own for the long-term.

PTPs: Brookfield has four publicly listed subsidiaries—Brookfield Property Partners (BPY, BPR), Brookfield Renewable Partners(BEP), Brookfield Infrastructure (BIP), and Brookfield Business Partners (BBU). We can invest in any one of these independently. It is unusual to see a publicly traded company spun off four separate subsidiaries—each one of them an independent entity. Brookfield (BAM), the parent company, retains substantial ownership in each of its PTPs. And it also exclusively manages assets that belong to each entity. For its services, BAM receives asset management fees from the subsidiaries.

Private Funds: Just like Blackstone, Brookfield also runs private funds on behalf of its institutional clients. These funds are individually focused on real-estate, infrastructure, energy, and private equity. What’s unique though is that Brookfield also invests its shareholder capital into the same funds. If I buy shares of the parent company or its subsidiaries, I get to profit from its private funds’ performance too. When I revisited my Blackstone investment in April, I said that I’d have loved to invest side by side with the institutional investors—but I can’t. In Blackstone’s case, those private funds are out of reach for individual investors. In Brookfield case, I do have access to them—albeit indirectly. And that’s another reason for my interest in the business.

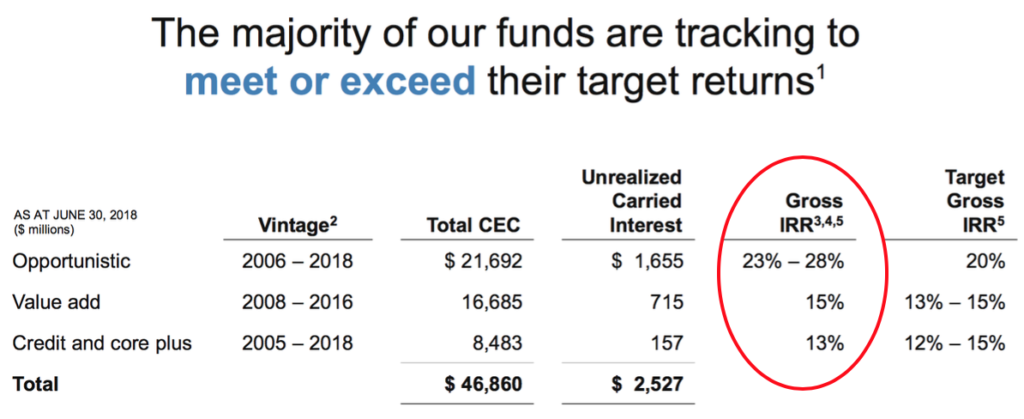

As seen from the below table provided by management, Brookfield has excellent historic returns on its funds—13% to 28% annualized. Those are the kind of returns I don’t believe I could earn by investing directly myself. Putting my capital into Brookfield shares allows me an opportunity to partake in such returns.

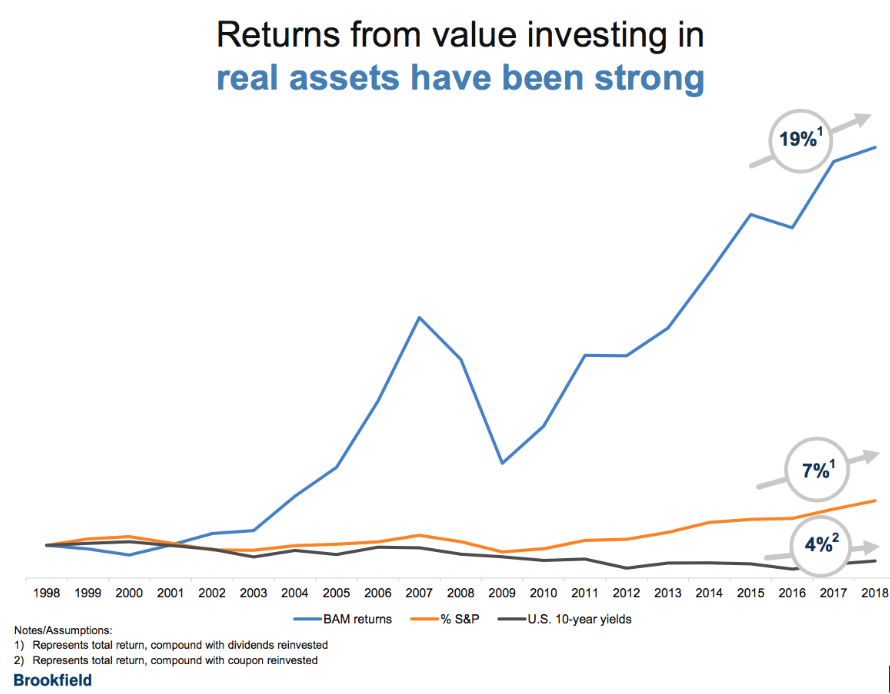

Readers of my blog know too well that I love founder-led businesses—especially those where the founder has significant ownership. I wrote a blog post last November on this topic: My investments with founder CEOs. Brookfield is not a founder-run company—though its current CEO has a very long association with the business. Bruce Flatt has been its CEO for 16 years—he’s also been with the company since 1990. Brookfield itself is a 100-plus year-old company—though Flatt has turned it into a premier alternative asset manager over the last fifteen years. It is mostly known as a savvy owner-operator of real-estate and infrastructure assets—what Flatt calls real assets. The company has certainly done very well investing in these real assets—handily beating the overall stock market. See the chart below:

Current and previous management of the company—including Flatt—owns 20% of BAM equity in form of Class B shares. Their economic interest aligns well with ours. Flatt personally owns 42.6 million shares that are valued today at about $2 billion. He writes good quarterly shareholder letters that I’ve found to very informative. Lots of details and insightful.

Brookfield Property REIT: So out of all the various Brookfield entities, what did I end up buying? I didn’t buy the parent company—at least, not yet. I might consider it down the road. At the moment, I am building my stake in the Brookfield real-estate business. There are two versions of it—both economically equivalent though. Brookfield Property REIT (BPR) is meant for U.S. investors while the Property Partnership (BPY) is the global partnership. I chose BPR so I won’t have to deal with the tax consequences of partnership income.

Why Brookfield Property (BPR)? Two main reasons: One, I have been on the lookout for opportunities to increase my real-estate allocation. Two, it is significantly undervalued by the market today. Let’s look into each in some detail.

As I explained in this blog post (How am I investing in commercial real-estate), my real-estate investing is entirely through REITs (publicly traded real-estate trusts). Through my REIT holdings, I am invested in high-end shopping malls (both US and international), retail strip malls on the west coast, cellular towers around the world, and some other holdings. Brookfield REIT (BPR) gives me access to prime office properties, top regional malls, and value-add opportunities via its private funds. About 40% of Brookfield’s assets are in class-A regional malls, another 40% in office buildings in top cities, and the rest in multi-family, storage, logistics, hospitality, etc. By adding BPR to my portfolio, I gained more diversity. For instance, I didn’t have office, multi-family housing, or hospitality assets before this purchase.

Valuation: I prefer to compare Brookfield REIT with Simon Property Group (SPG)—another premier REIT that I closely follow. As I explained in this post from last year (Why I like Simon Property Group), I like Simon management and have been a shareholder. Both Brookfield and Simon have similar operations—both are top-notch regional mall operators. At today’s prices, BPR is valued at 12.8x last twelve month’s FFO (Funds from Operations) versus Simon at about 13.5x. But FFO, by definition, doesn’t include gains from LP investments (i.e. private funds)—profits that BPR has but Simon doesn’t. Taking into account the LP income—even though it is volatile in nature—BPR today is valued even cheaper at about 9.2x. Whether I consider LP income or not, paying 10- or 12-times current income for a business that is expected to grow income (FFO, in this case) by 7 – 9% (management’s target range) is a good deal.

Another way to value both businesses is via their dividend yields. Today, Brookfield REIT yields about 7% while Simon is at 5%. Brookfield has grown its dividend by 6% CAGR in last five years. Management’s target for the next five years is between 5% and 8%. If they hit their target range, my return-on-investment could be in the range of 12% to 15% annualized. Simon’s current yield is lower, but it has grown faster—at about 10% CAGR.

I believe both Brookfield REIT and Simon are good value for money today. However, I am focused on Brookfield REIT today. I believe it has higher growth potential in the next five years and it adds more diversity to my portfolio.

Why’s Brookfield selling cheap today? I don’t think there is one thing I can point at. From what I could tell, it’s a combination of factors. For one, brick-and-mortar retail REITs have been in disfavor and Brookfield being the contrarian has recently acquired a large chunk of prime regional malls via its GGP acquisition. It has also been aggressively expanding its asset base during last five years—buying up opportunistically and paying with new share issues. In 2013, the parent Brookfield (BAM) owned 90% of the REIT. Since then, BAM’s ownership has gone down to 51% as it issued new shares to buy assets. Another factor is that unlike most other REITs that focus on one area of real-estate, Brookfield REIT invest in all kinds of real-estate—as I pointed out earlier.

Today Brookfield REIT is an unloved stock—and hence it’s also undervalued by the market. Net Asset Value (NAV) of its properties was estimated at about $29 per share as of September 2018. Today, its shares are trading at $19 a piece. Mr. Market is handing me a good deal. And with a time-tested long-tenured management at the helm, this is a no-brainer investment for a patient investor like me.

Leave a Reply