I have written several times in last two years about my investment in Blackstone (BX). Blackstone is the largest alternative investment asset manager in the world. I have been gradually building up my stake in it for two years. Its shares have mostly stayed flat since — somewhere between $30 to $35 per share. Until last Thursday, that is, when it announced first quarter earnings. But it wasn’t due to the earnings itself — even though it looked good and as expected. The stock jumped up to about $40 that day because the company announced it is converting from a publicly traded partnership to a C corporation.

You can read my full investment thesis on Blackstone here. In that post, I considered the possibility of its C-corp conversion. I called it a possible icing on the cake. Two reasons why this conversion is a good thing for investors: (1) It makes Blackstone eligible to be included in various stock market indexes. (2) Individual investors dislike the tax hassles that come with partnerships.

Blackstone pointed out that by ditching its public partnership structure, it would now be eligible for inclusion in the MSCI and Total Market indexes — nearly doubling the size of its eligible asset universe. Today only about 20% of its ownership is in index funds and ETFs whereas average ownership of its C-corp financial peers is in 60s. This is likely the big reason why the stock went up by more than 10% on the day of the announcement.

As for the tax hassles in dealing with partnership income, I can vouch for it. Partnership income is distributed to share-owners via Schedule K-1s. I have been processing K-1s for last couple of years in my tax filings. It’s certainly more work than regular dividends I receive from owning shares in public C corporations. All K-1s require special treatment but those from Blackstone especially require extra work since it is a large diverse organization with multiple business lines. This year, I had to deal with depreciation expense, return of capital offsets, and real-estate rental income, among other items. Unlike dividends from regular corporations, distributions from Blackstone are not treated uniformly under tax codes. A portion of it might be considered qualified dividend income but the rest could be ordinary income which is taxed at a higher rate.

A downside of this C-corp conversion is the margin dilution that could reduce its profits. I wrote in my previous piece that the company estimated about a 15% hit to its bottom-line profits. I expected a similar size cut in future dividends. So, it came as a pleasant surprise when management announced last week that there will be no immediate impact (2019) to its profits. They cited some IRS tax basis step-up rule (section 754) they plan to take advantage of. It has the effect of increasing the tax bases of existing assets and then amortizing the step-up bases over the next 15 years. The net result would be no impact to immediate earnings, and then 2% to 5% impact over the next five years, gradually increasing to 12% to 13% over the long term. This is good news for us investors. It’s the near-term impact that concerned me more. Over the next five years, I expect Blackstone to grow its AUM (Assets Under Management) rapidly — and therefore its fee related earnings. So the long-term tax impact of 12% would be mostly offset by the expected increase in its earnings power over time.

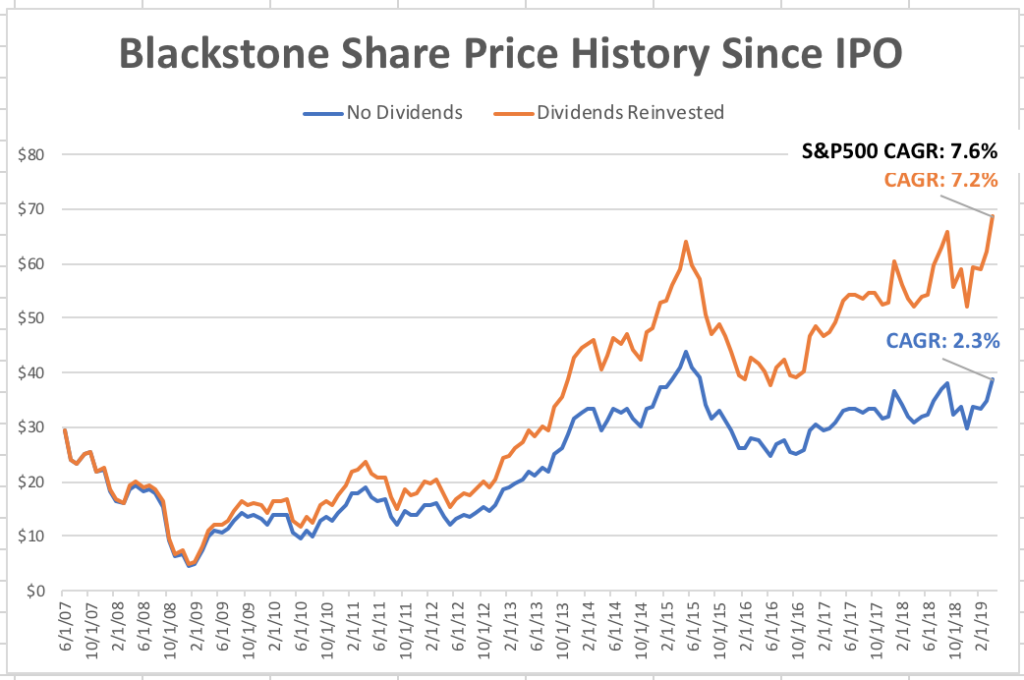

Since Blackstone’s IPO in June 2007, the stock has performed roughly at par with the S&P 500. But you wouldn’t know this if you just look at Blackstone’s share price itself. This is what most stock charts show — share price changes. However, unlike majority of the companies in the S&P 500 index, Blackstone pays out most of its earnings (about 85% of it) in form of dividends. It only retains a small fraction. It is worth pointing out here that the company has a bit of an unusual business model. It returns most of its profits in form of dividends like all REITs (Real Estate Investment Trusts) do. But unlike REITs and MLPs (think Oil and Gas partnerships), Blackstone’s business is very capital light (near zero corporate debt). All the capital it needs for investments belongs to its limited partners (like endowments, pension funds, etc.)

This chart shows the disparity in Blackstone’s returns — with and without dividends reinvested. If we take dividends into account, Blackstone’s average annualized return is 7.2%. Without dividends, it drops to a paltry 2.3%. Now that’s a very big difference given the time period we are dealing with — eleven years. In dollar terms, an initial $10,000 investment at its IPO would be over $22,700 today if dividends were reinvested. If no dividends were considered, it would only be worth $13,200.

Commonly available stock charts can be misleading if a company pays generous and growing dividends consistently over the years. We investors would do well to remember this key lesson: Dividends can make a significant difference in our overall returns if reinvested over a long time period. In a previous blog post, I pointed out how even in a flat 10-year period in the stock market, investors would have made a not-so-bad 26% gain if they had reinvested all dividends. See this: Revisiting the lost decade of U.S. stocks

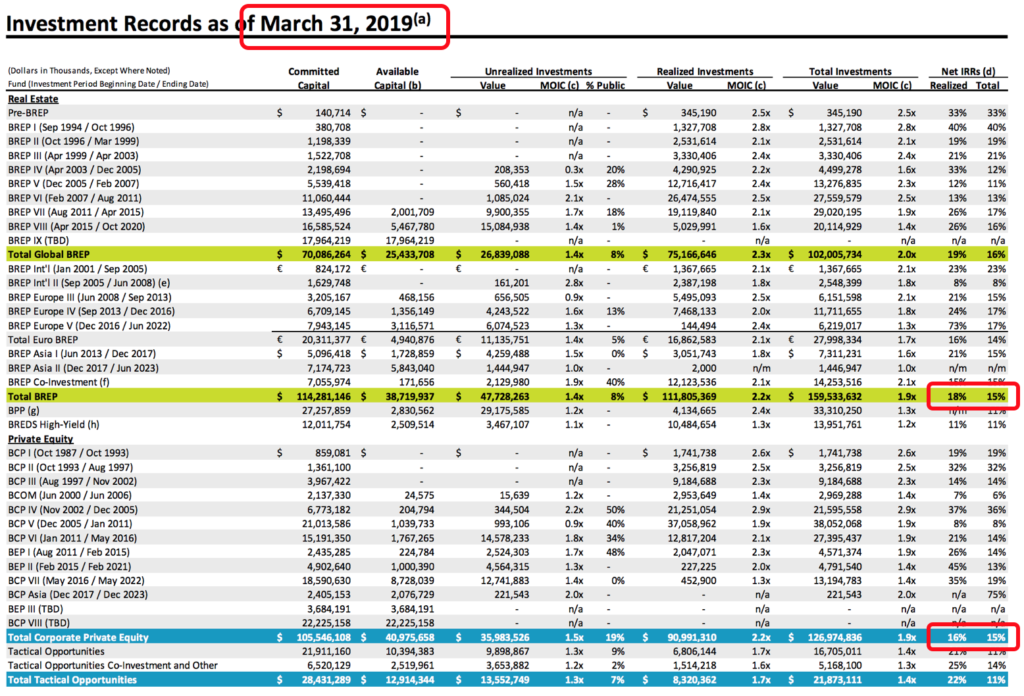

Not only that Blackstone is the world’s largest alt asset manager, it also has done really well for its institutional investor partners (aka limited partners) over the last thirty years. Take a look at this slide from its 1Q’19 earnings release:

Since 1987, Blackstone’s private equity funds have generated an average annualized return of 15%. And since it started real-estate funds in 1994, those funds have realized returns between 15% to 18% per year. I would have loved to invest in funds like these. Alas, even though I am an accredited individual investor, Blackstone’s funds are not accessible to me. They are meant for institutional investors with much deeper pockets. In a previous blog post (My quest for commercial real-estate), I shared my experience of researching a recent Blackstone real-estate fund that was open to individual investors. I did seriously consider investing into it but decided not to invest because the upfront fees were too high.

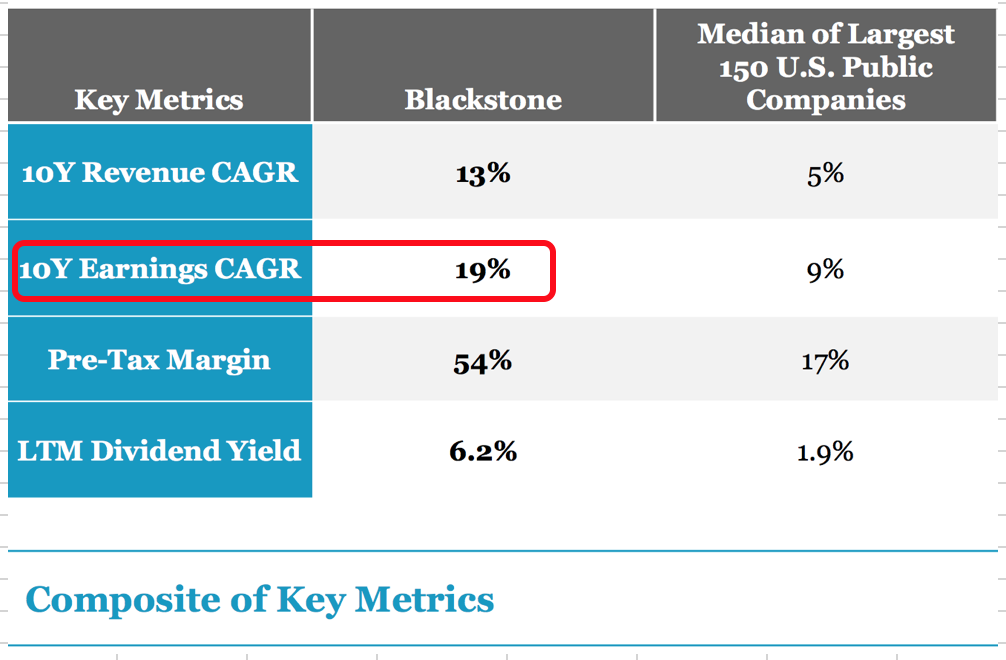

Blackstone’s excellent record of high returns for its limited partners have also resulted in high earnings and distributions growth for its shareholders. Since 2008, its earnings have grown at an outstanding average rate of 19%.

And above all else, it has well-respected founder-driven and shareholder-friendly management. Chairman and CEO Steve Schwarzman owns about 19% of the company. Executive Vice Chairman Tony James, who was previously the COO, is also the chairman of Costco — another company I deeply admire. The new COO is also the heir-apparent of the company, Jon Gray. His investing record at the company has also been excellent. He built Blackstone’s real-estate business from scratch and made some outstanding real-estate deals over the years (see Hilton and EOP deals).

However, despite its excellent record for its limited partners (and earnings for shareholders), Blackstone’s share price hasn’t done nearly so well — as evident from the stock chart. Its returns have barely matched the overall US stock market returns even though its earnings have beaten the market handily.

I attribute this underperformance to a combination of factors. For one, its IPO was badly timed (with 20-20 hindsight) in 2007. With the great economic downturn in 2008, the performance income dried up quickly. And even though the company came out unscathed and stronger at the other end, investors were turned off due to the early decline (and later, unsteady growth) in dividends. And then it didn’t help that the company was a partnership and not a C corp — reducing its overall appeal to would-be investors. And finally, among those remaining investors, those who were not focused on dividends alone would often pass up this company because the stock’s historical performance didn’t look all that impressive at first glance (minus the dividends, of course).

Nevertheless, I admire the business and its management. I had been a buyer for last two years. With this recent conversion, the company may have turned another corner and likely become more appealing to other investors.

One factor to consider when investing in alt asset managers is the state of the economy. Blackstone’s profits depend on two sources: management fees on assets and performance fees when it sells assets profitably. The former is relatively steady since AUM doesn’t change much even in downturns. The latter however depends heavily on market conditions. When assets are priced low in downturns, Blackstone tend not to sell much – thereby impacting its performance fees. It makes up for this when the tide turns. Overall result is that profits tend to drop when the market conditions deteriorate. And so does its share price.

Still, I am a long-term oriented patient investor. I don’t consider this to be a long-term risk. From my vantage point, there aren’t many risk factors that could permanently damage Blackstone’s business model. Alternative assets are here to stay, and I believe institutional investors will continue to flock to good alt asset managers. David Swensen of Yale popularized the use of alt assets in institutional investing, and they are here to stay. Succession was indeed an open question last year but with Jon Gray clearly getting groomed for the top job, I think that risk is no longer significant. Reputation is the single most important consideration for fund-raising in this industry. And Blackstone clearly takes good advantage of its best-of-the-breed reputation. There is always a risk that a few bad investing mega deals or a streak of under-performance versus the industry could lead to underwhelming fundraising down the road. I can’t rule it out as a possibility but having studied this management for a few years now, I feel comfortable knowing that the chances of permanent damage to its brand is quite remote.

Even so, I expect Blackstone shares to drop whenever the stock market declines next. I don’t know when it would be, but I will be ready to scoop up more shares then. I prefer buying when shares are cheap, and I keep some dry powder cash for such occasions. You can see from my 4Q portfolio update, I bought Blackstone shares (at about $28.60) in December last year when the market was down a lot.

Emcee,

I just discovered your blog and am fully enjoying exploring many of your posts. One thing that has struck me is the many examples and data points you have pulled out of your own investments. My own investments are closer to the Bogleheads 3 index fund model so are much simpler than yours. Even then tracking everything to fully wrap you head around what your money is doing can be a challenge when you spread it across multiple IRAs, 401ks, etc. What tools do you use to track your own investments to the level of detail you often show in your posts?

Thanks,

Brad

Hi Brad:

I will do a detailed post on this topic … but here are my quick comments:

I use Quicken Premier extensively. Just like you, I have multiple IRAs and brokerage accounts with several custodians. I have been using Quicken Premier for more than a decade and love it (despite some idiosyncrasies). It does a fine job collating all my accounts together regardless of where they are located. Also, I am a power user of Microsoft Office. Most of my charts and tables are done in Excel. Quicken makes it easy to export data into Excel.

Thanks, emcee