My investing in commercial real-estate is mostly via publicly traded REITs (Real Estate Investment Trusts). Over the years, I have added several REIT positions in my portfolio. See this table for my REIT holdings.

From time to time, I’ve also researched certain non-traded commercial REITs but had never pulled the trigger on any one of them. For instance, see my Blackstone BREIT analysis here.

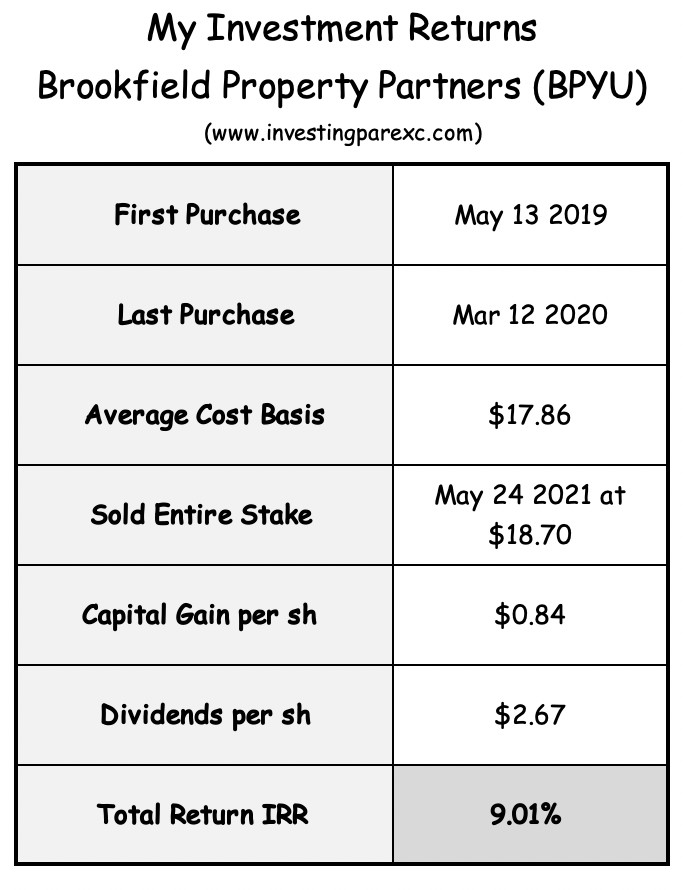

Within commercial RE, one of my recent focus areas has been the retail real-estate. It’s an unpopular real-estate category among REIT investors and hence good investing opportunities can be found there. Brookfield Property Partners (BPY or BPYU, formerly BPR) is one such retail REIT that I am invested in. I first bought its shares in May 2019 and then continued adding to my position over the following twelve months. As I first wrote about it in a blog post in July 2019, BPYU was significantly undervalued by the market, selling at about 10 times free cash flow. Its dividend yield was also a generous 7% at the time. I thought it was a good bargain—generous valuation and a well-run business.

Brookfield Property Partners is the owner and operator of regional malls, shopping centers, office buildings, and other institutional real-estate assets. It is run by a highly regarded Canadian asset manager named Brookfield Asset Management BAM. At the time, BAM owned about 50% of the REIT itself.

I consider BAM a very well run and savvy long-term operator. I profiled them here. In fact, one appealing aspect of BPYU investment was indeed its owner-operator parent—BAM. At the time, BAM was expected to grow BPYU free cash flow by 7–9% every year. This did not materialize though when the pandemic hit last year. BPYU stock subsequently dropped by 50% in March 2020. I bought some more shares at those bargain basement prices. Later in the year, BAM management thought BPYU is still trading well below its NAV (Net Asset Value) and bought more of the stock. Its ownership went from 50% to 65%. However, as BPYU shares stayed well below its asset value, the parent BAM decided to take over the entire company. On April 1st this year, BAM announced a deal to buy the entire business and merge it with the parent company at the share price of $18.17. At the same time, BPYU also announced that no further dividend payments will be made (March was the last distribution), pending the proposed acquisition.

It wasn’t my desired outcome. I continued to believe in the long-term prospects of this business, and I was happy collecting a nice dividend every quarter while waiting for the share price to recover. However, I am just a minority investor in the business. I have no real say in whether this acquisition ought to take place or not. I fully expect this transaction will go through. Per the agreement, I as BPYU shareholder could choose to get cash for my shares or parent BAM shares or preferred units.

Stranded Investors? When a business is trading at a significant discount to its underlying value, it’s not just us the long-term minded individual investors that get attracted to it. Other much larger institutional players also take interest. These investors have deeper pockets than we do. They are often willing to pay a premium over current market price to persuade the business to merge. Depending on when an investor like me has bought the stock, the offered premium might not be enough to make us whole. It is a risk that does not get discussed often. Over my investing journey, I’ve had several such situations (or close encounters) to deal with. I plan to write about them in a future post.

Since BPYU has stopped paying dividends and this transaction is not expected to close until the third quarter (if approved), I thought it’s good time for me to part ways (albeit regretfully) with this REIT. I sold my entire stake at a little above the offered going-private price on May 24th. My rate of return over the two-year period where I built this position and collected dividends came out to be 9% IRR. This isn’t a bad return, but of course I was fully expecting to generate double-digit returns if I were able to hold on to my shares for a few more years.

As you can see from the table below, most of my returns came from the dividends I received. My capital gains were bare minimum as I sold shares just a shade above my average cost.

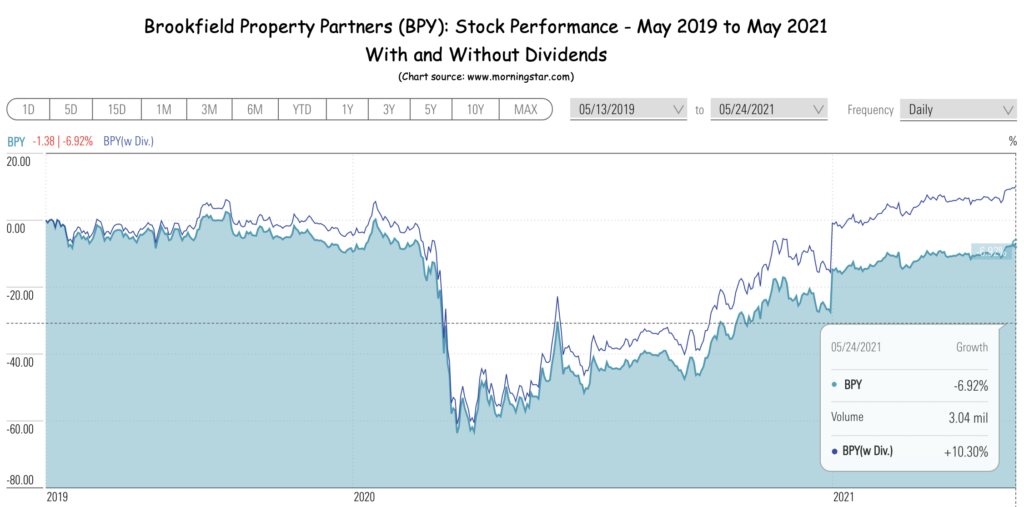

The chart below shows BPYU share price over the last two years. When I sold my shares, its shares were trading 7% below the price I paid for my first helping. But I had bought more as the stock went down in March 2020, so my average cost basis had also gone down. Also from the chart, BPYU did far better when taking into account all the dividends I received. Had I just bought once in May 2019 and did not receive any dividends, my final return would have been negative.

Other Investment Candidates: Now that my entire BPYU position is liquidated, I plan to reinvest this money in other real-estate related businesses. They don’t need to be REITs per se. Any business that earns majority of income from some real-estate activity would be a good candidate here. In this bucket, I have some good prospects—some of these I am already a shareholder in. Others I have been following for a while and like their business potential.

One obvious candidate is the parent company itself, Brookfield Asset Management (BAM). BAM is an excellent business, run by smart long-term oriented owner-management. See my profile of BAM CEO here. Even though I started investing in BPYU first, since then and especially with the onset of pandemic drop, I had started building a position in BAM. One downside of swapping BPYU with BAM is substantial loss of current income in favor of long-term outperformance. As I pointed out earlier, BPYU has been a prolific dividend generator for its shareholders during the last two years. BAM, while a very profitable business, reinvests most of its profits into further growth—rather than paying it all out in dividends as REITs do.

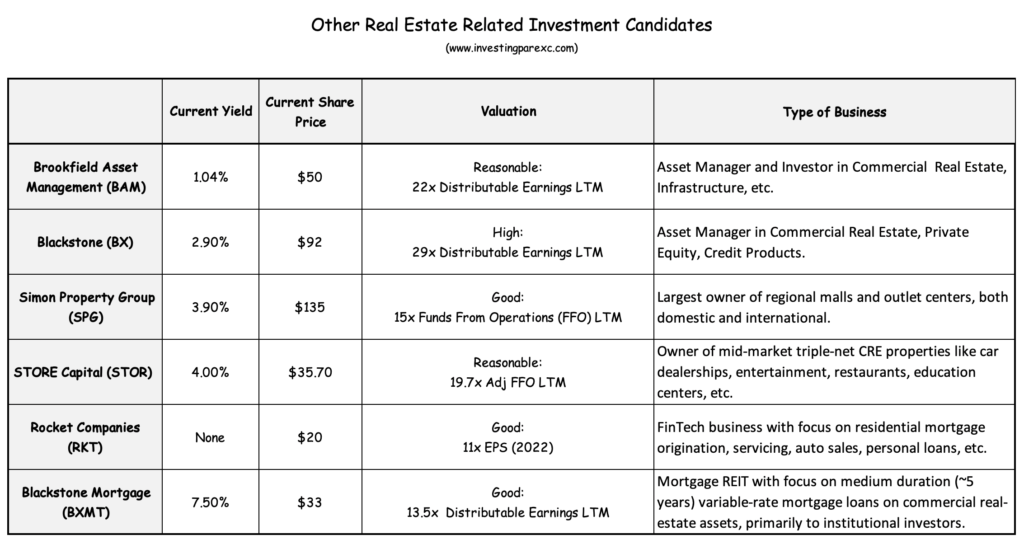

There are other good real-estate related businesses that I have had my eyes on. See the table below. They are not all significant dividend payers. They also focus on various real-estate types and therefore have different growth profiles.

In the next few weeks, I plan to pick one or more of these businesses and invest my BPYU proceeds in. In my next blog post, I will write more on each of these. Stay tuned.

Leave a Reply