Over the last few months, I have written multiple times about real assets. So I won’t belabor the benefits and opportunities in real-estate (and other hard assets) investing here. To wrap up the series of posts on this topic, I’d like to roll up all my related investments and present an overall picture.

This blog post would make most sense if readers would first go over my previous related blog posts: How am I investing in commercial real-estate?, An opportunity to invest in real assets

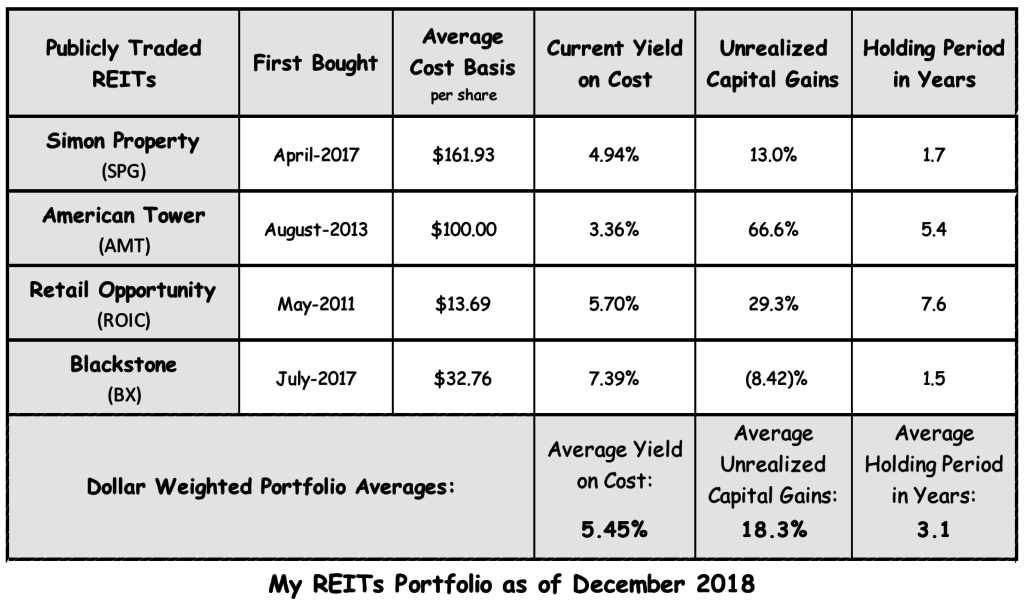

I shared my real estate portfolio in a blog post in December last year. Back then, there were four positions in it—three public REITs (Real Estate Investment Trusts) and one PTP (Publicly Traded Partnership). Those three REITs are owners and operators of top-quality regional shopping malls, premium factory outlets, cellular tower locations around the world, and grocery-anchored strip malls on the west coast. And that one PTP was Blackstone (BX)—one of the largest real estate investment managers in the world.

Here is the table from that December 2018 blog post.

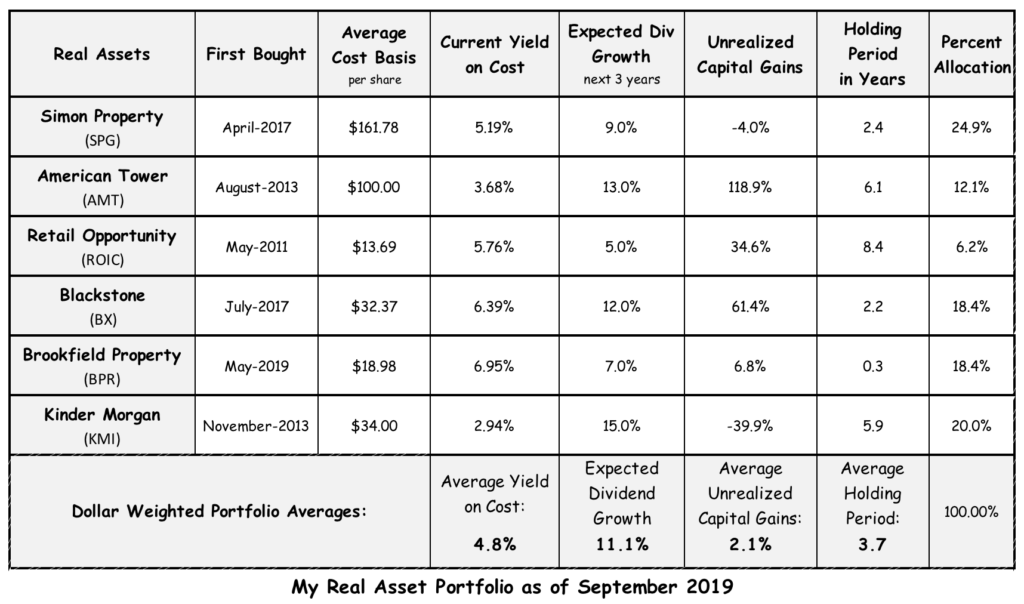

Since then, I have made a number of changes in my real asset holdings. The table below shows how my portfolio looks today.

Changes since December 2018: I’ve continued to add to my positions in Simon Property Group (SPG) and Blackstone (BX). Simon’s shares had been under pressure lately due to lingering concerns about brick-and-mortar retail. I consider Simon a well-run business with shareholder friendly management. I scooped up more Simon shares this year. You can see my detailed writeup on Simon here.

I have been an admirer of Blackstone’s business model even before they switched from a partnership to a C corporation in June this year. I made my investing case on Blackstone in this blog post in April. Blackstone does not just do real estate—it is also in private equity, hedge fund management, and credit investing. But for this blog post we are focused on just real estate, so I only allocated 40% of my total Blackstone position to the table above. Blackstone has about 40% of its AUM (Assets Under Management) in real estate.

Aside from adding to my existing positions in Simon and Blackstone, I’ve also been building a new position in Brookfield Property REIT (BPR). Brookfield, like Blackstone, is also a world-class investment manager. But unlike my Blackstone investment, here I have invested in a Brookfield managed REIT that focuses entirely on commercial real estate operations. I wrote about Brookfield in a blog post here.

For good measure, I also threw in my Kinder Morgan (KMI) position in the table. It makes sense to have it there. Kinder Morgan owns and operates oil and gas infrastructure assets. These are real assets too. I profiled Kinder Morgan and its business model in a blog post two weeks ago. As I explained there, KMI is a losing position in my portfolio. It also yields the lowest today. However, I am optimistic about its future and like its management. So I am happy to hold its shares and collect dividends on them. In the same blog post, I also pointed out that KMI is expected to increase its dividend by 25% next year.

Even though today Kinder Morgan is holding down my average dividend rate, I am still collecting a healthy 4.8% dividend on my entire portfolio (on my total cost basis) today. And I estimate that those dividends will grow at about 11% rate for the next three years. If I compare today’s dividend rates with those from the December 2018 table, the yields on Simon, American Tower, and Retail Opportunity have all increased since then. The only exception is Blackstone where my dividend yield has dropped a bit but that’s just the nature of Blackstone’s business. I wrote about Blackstone in a February 2018 post, Why I am buying Blackstone. In that post, I pointed out that its business model is such that the earnings (and the dividends) tend to be volatile year over year.

My unrealized capital gains have also gone down significantly by virtue of adding Kinder Morgan to the portfolio. But that is just a curious fact. It’s not a meaningful data point. Share prices are by nature volatile. For instance, notice how Blackstone shares have risen by more than 70% since December. For my real assets, I focus on just dividends.

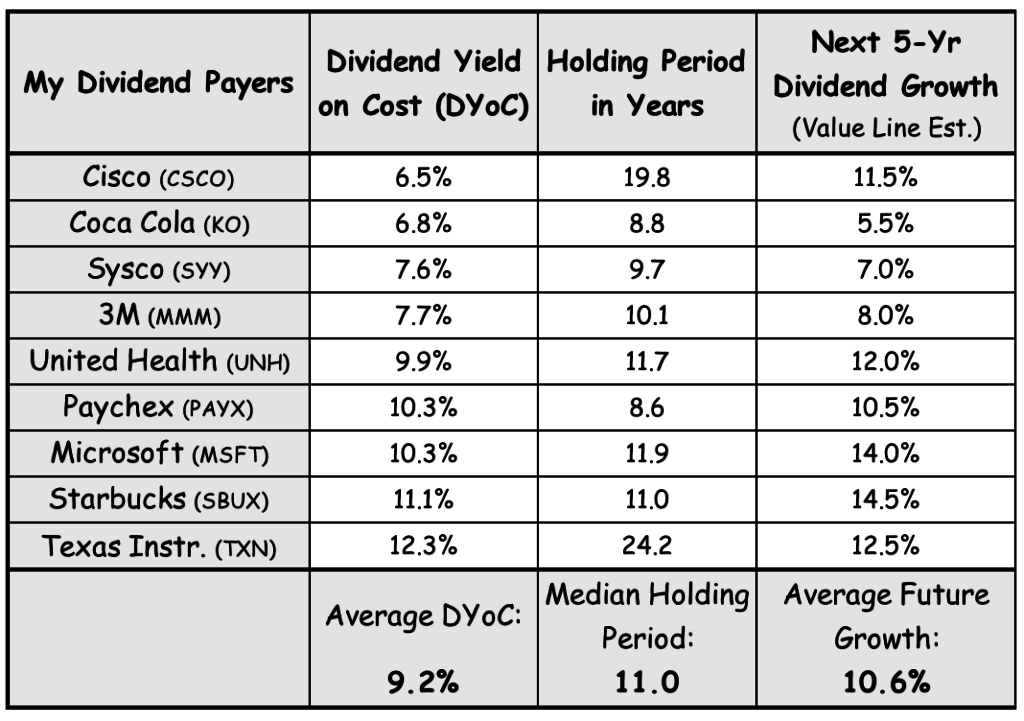

One final point about these holdings—it is a relatively young portfolio with an average dollar-weighted holding period of less than four years. Even though today’s dividend yield might not look so impressive, but it will do better as the portfolio grows. Consider how my other dividend generators’ portfolio (not real estate) has been doing. I called it my Uber Dividend Payers and wrote about it in February. My median holding period of those positions are eleven years and collectively they are yielding a bit more than 9% on my cost.

{kind=link}

Similarly, I expect this real asset portfolio to do well over the next five years. I am not yet done adding to these positions either. Today they make up slightly less than 10% of my overall portfolio. I have room to grow my share of real assets further. I am looking for any other compelling opportunity to invest, but at the same time, I am not in a rush to buy.

Leave a Reply