On June 9th, as the stock market came within 5% of its previous record high, my portfolio reached a new all-time high. That day, my portfolio nudged just above its prior record high made on February 19. Credit for this outperformance (since the broader stock market has yet to clear its previous high) goes to (a) my new stock purchases that were made in February/March when stocks were cheap and (b) my blue-chip technology holdings. Let’s dig further into both these factors.

Since June 9th, the market had dropped again by 5 percentage points. Today (on July 6th), it’s still about 1.5 points below the June 9th mark. I started writing this post in early June but couldn’t finish it until now. While June 9th appears to be a near-term high and the market has given up some of its gains since then, the points (no pun!) I am making in this post still remain relevant today.

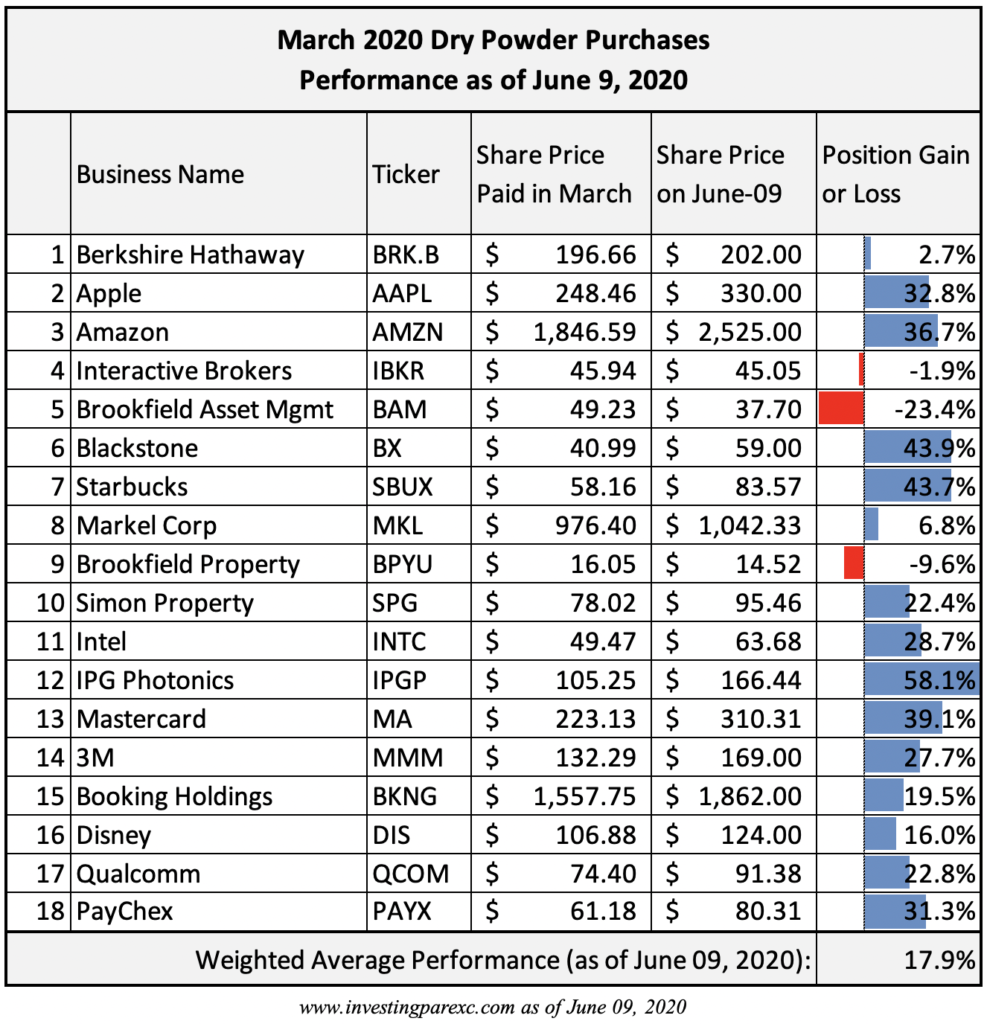

February-March Purchases: I wrote two blog posts in March this year (Be greedy, Seeking wisdom in trying times) on my stock purchases that were made at the time when share prices were declining quickly. At the time, I wrote that I had kept some cash on the sideline (so called, my dry powder) that I had used then to buy stocks.

In one of those blog posts, I also shared a list of stocks I had bought. The following is an updated version of that same list. In this update, I show how those positions have performed since I bought them.

As you can see from the table, majority of these new positions have done very well since the time of purchase. As of June 9th (when my portfolio reached a new high), on average those purchases had gained about 18%. There are only two losing positions so far, and both belong to the Brookfield family: Brookfield Asset Management (BAM) and Brookfield Property REIT (BPYU). Since March, investors have soured on commercial real estate and thus the decline in the Brookfield companies. However, I like their prospects over the long-term and I am comfortable holding them.

Two positions that haven’t gone anywhere are Berkshire Hathaway (BRK.B) and Interactive Brokers (IBKR). Each is in a unique situation. Berkshire hasn’t done well because of the lingering concerns about rising claims and ensuing litigations in the P&C insurance industry. IBKR has treaded water in sympathy with the rest of the financials. I like them both and happy to keep them.

The rest of the positions have done very well since March. Their outperformance has more than made up for the four laggards.

Big Tech Flying High: As I said earlier, the other factor that contributed to my portfolio’s outperformance is how the big-tech has performed in this post-COVID recovery. I wrote a blog post on March 2nd—just when the market was at the cusp of this bear market—where I pointed out how my portfolio has become top heavy. Today, my top-ten stock positions are a bit more than half of my entire portfolio’s net worth. My top-twenty positions make up more than three-quarters of it. Nevertheless, back then and even today, I am comfortable with this concentrated portfolio. Peter Lynch had likened selling winners to cutting flowers, and I agree with him. I don’t intend to sell my winners either.

Many of my top-twenty stock positions are in mega-cap high-tech businesses like Amazon, Apple, Microsoft, and Facebook. In that March 2nd post, I had shared a table of my top-20 positions. Not much has changed since then. All those stocks today are still on my top-twenty list, with the exception of one: Simon Property REIT (SPG) hasn’t done so well lately, so it is replaced with 3M (MMM) in the new list. I haven’t sold any SPG shares though. See this updated list:

Out of these twenty stocks, half of them (those are circled in green) are at or near their record highs today. These all happen to be technology companies (or where technology plays key role in their products). It has been a main theme of this market recovery: Big tech companies have gained strength as some other traditional businesses are faltering. Even before this downturn, a good portion of my portfolio had consisted of technology stocks. Today, some of these big tech names have grown to be even bigger. This is fine with me. While I am no longer aggressively adding to my existing technology stakes (like Facebook or Amazon or Apple), I am content in holding on to them. They are durable and dominant businesses with significant growth runway ahead of them. I wrote in a blog post in January (Buy Right, Sell Never) that I take inspiration for my investing from the book 100 Baggers. That book recommends an investing approach where we buy good businesses and hold on to them for decades. If we are patient (and lucky), some of our holdings may even turn into 100 baggers.

Breakevenitis, anyone? I listened to Fisher Investments’ market update this weekend (check out this Market insights episode at 05:35). The podcast host pointed out that as the stock market recovers majority of its losses, as is the case today, some investors get antsy. They consider bailing out as they are more or less at a breakeven point. They might have persevered through the decline, not wanting to sell and lock in the losses but now that they have broken even, it’d be tempting to sell everything. He called this investor behavior trap, breakevenitis. [This article is a great read on this breakevenitis phenomenon.] Needless to say, Fisher Investments cautions against falling into this trap.

As my portfolio has broken past its previous high, do I feel like bailing out on stocks? In other words, am I also afflicted with breakevenitis? The short answer is no. Given how my portfolio is mainly in stocks, I am accustomed to fluctuations in my net worth. As I wrote last year (A gauge for my portfolio), I prefer to think of my portfolio’s value as a range, rather than a single number. The low end of this number range is a good reminder of what a severe market decline could do to the portfolio. Today I am well above that low number, as one might expect. If stocks go down again from here, I might test that low end once more. It would be OK if that were to happen. I am invested for the long-term growth and I expect there will be bumps along the way.

Leave a Reply