I have written about my dry powder investing several times before. I am not going to rehash all that stuff here. [You can check out all my previous Dry Powder related posts here.] Instead, in this post I will just focus on performance of my hedged stock positions where I keep this dry powder cash. Today, about 70% of this dry powder is invested in stocks. As I wrote in this blog post, I took advantage of the market plunge in March to put this cash to work.

Here’s a quick recap of how I invest this dry powder cash. I need to keep this cash accessible (and not tied up with long duration investments) since I can’t predict when I might need it. At the same time, I also look to generate better-than-cash return from it.

In my portfolio, I allocate about 10% to this dry powder cash. I also keep two to three years of living expenses in rainy day funds. The rest are all invested in long-term assets like public stocks and real estate/REITs.

For last three years, this dry powder cash has been invested in hedged stock positions (protective collars, mostly) where I try to generate positive return with the help of dividends and some capital gains. These positions are hedged with long-short stock options such that my downside risk is minimal, but the upside gain is also capped. See this blog post for more details on how I structure the protective collars.

I realize that these protective collars aren’t for everybody. To do them well, one must pick an underlying individual stock and understand how stock options work. A simpler alternative to this would be to invest in a short-term bond fund or ETF. Those are liquid and usually generate returns somewhat better than cash. There is expected to be some price volatility but sticking with investment grade corporate bond ETFs is generally quite safe.

Another investment alternative could be a market neutral ETF. These ETFs also try to generate better than cash returns while trying to avoid stock market volatility. Most of them do not have good investment records though. Last year, I wrote a blog post on market neutral funds and how they have failed investors. See here.

What exactly are market-neutral funds? These funds try to generate steady albeit low returns that are independent of how stock or bond markets perform. Most of them employ a long/short strategy to drive returns—short some stocks and go long on others. By offsetting longs by shorts, they try to generate profits independent of how stocks move. Others try to profit from corporate events like mergers and spinoffs. But the overarching idea is that same—generate steady returns in all kinds of market environments.

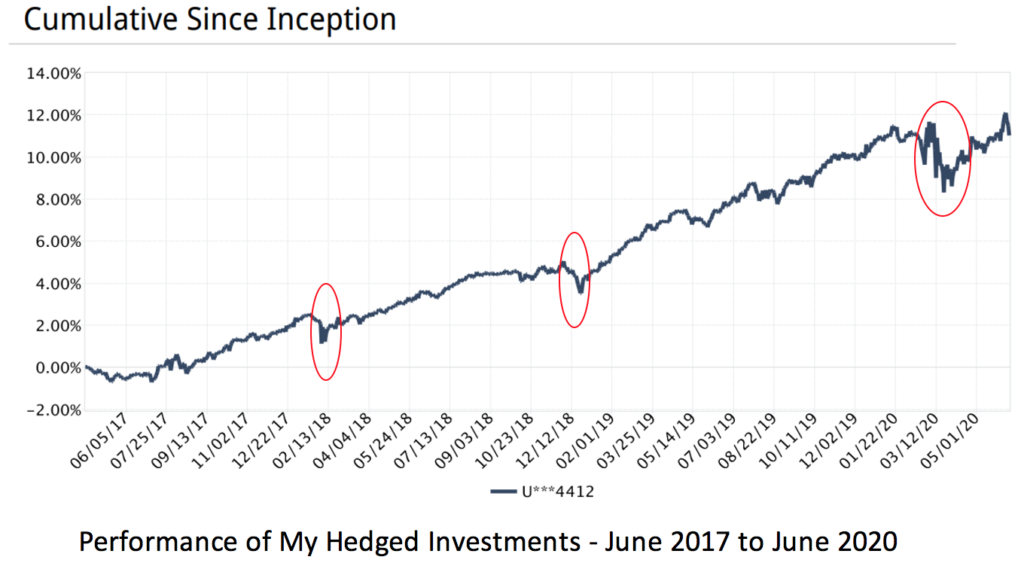

I have been investing in these protective stock collars for three years. Since June 2017, my annual compound return to date is 3.37%. In January 2019 post (Investing Amid Volatility) I showed my then active principal-protected investments. At the time, my realized return was 3.20%. Today, about a year later, it has improved to 3.37%.

Most of these hedged positions are two years in duration. Some I close early, and others expire over time. Usually within a few days of closing a position, I open a new position. It could be with the same underlying stock or another one. But in all cases, I limit my pickings to one of the stocks that I am very familiar with and have confidence in its business model. Most of the time, the stock I choose is one that I already own in my long-term stock portfolio.

During the three years of investing in these, the stock market has had two corrections that were greater than 10% each (in February and December 2018) and one bear market (still on-going since March 2020, about 35% drop so far). On each of those occasions, my protective collars did not decline much. My positions dropped less than 2% during the two 2018 corrections. At the peak market drop this year, my positions only dropped about 3%.

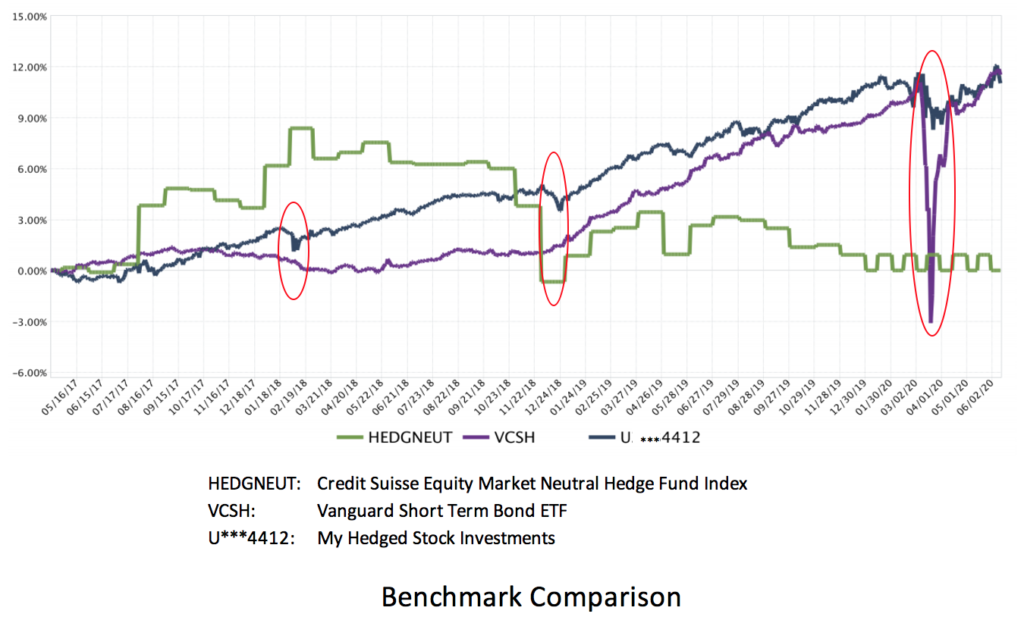

Here is another way to look at the volatility of these investments. In below chart, I show two benchmarks overlaid with my positions’ performance for the same three-year period. The first benchmark is Vanguard Short-Term Corporate Bond Fund (VCSH) and the second is Credit Suisse Market Neutral index (HEDGNEUT). In that period, the market neutral index has basically stayed flat, returning 0%. On the other hand, the bond index return matched with my returns, albeit with much greater volatility. See the big dip VCSH suffered in March this year when stocks were tanking:

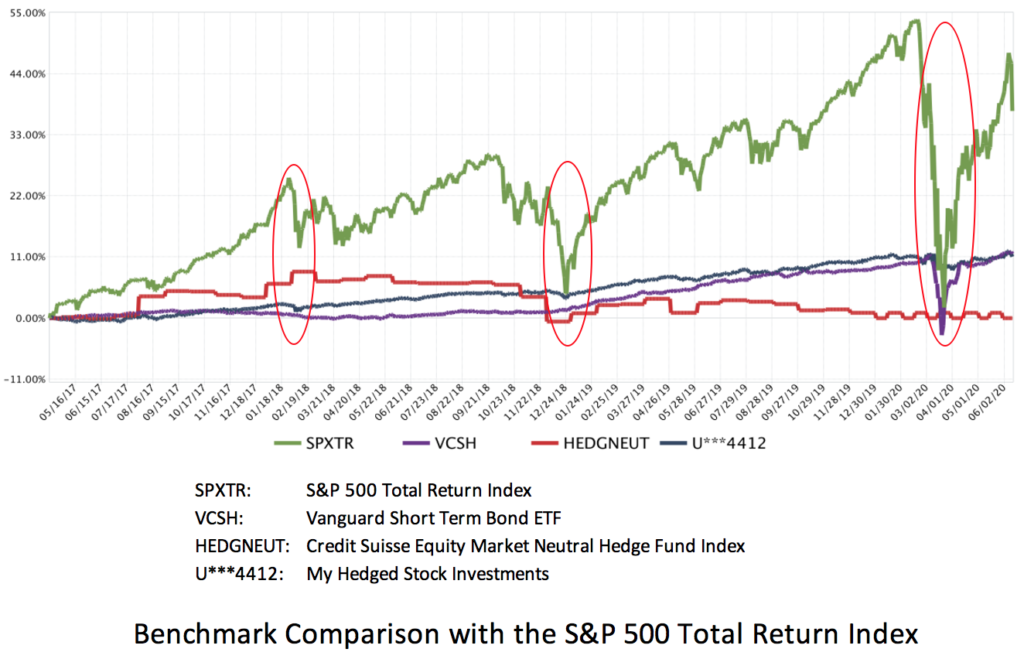

For further context, here is the same chart with the S&P 500 Total Return index (SPXTR) overlaid. You can see how flat all those charts look when compared to the stock market itself:

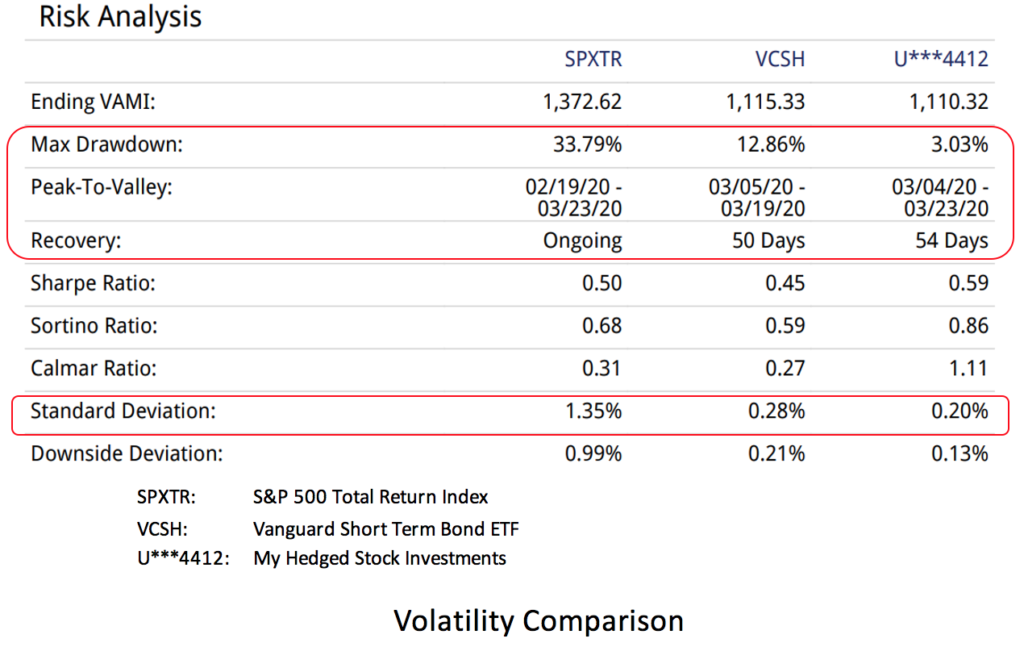

In this next table, I compare relative volatility of my investments with the S&P 500 index and the Vanguard ST Bond ETF. It’s clear from the table that my investments have been far less volatile. That much was also clear from the previous charts, but this table shows actual numbers. During the March stock crash, my positions suffered maximum drawdown of 3% while the SPXTR dropped by 34% and the VCSH by about 13%. Also, my positions’ return dispersion has been less too, with 0.2% standard deviation versus 1.35% for S&P 500 and 0.28% for the ST bond ETF.

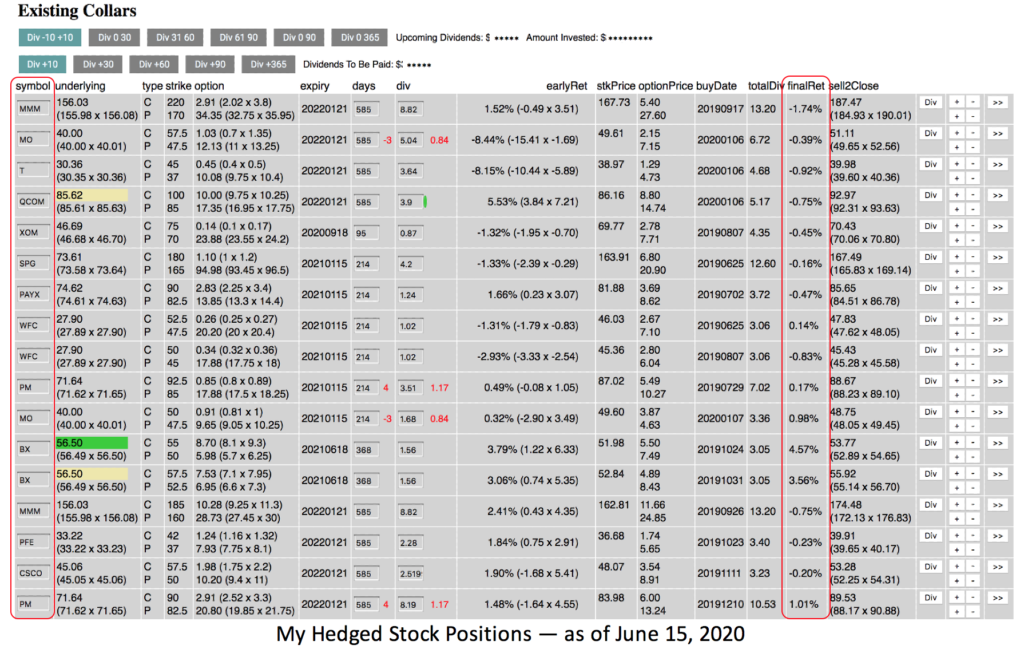

Here is a snapshot of my active hedged stock positions today:

These are far too many to cover in detail here. But they all follow the same protective collar structure: a long stock position coupled with long Puts (for protection) and short Calls (to pay for Puts). Each stock position is identified by its ticker symbol in the far-left column. Many of these positions do not expire until January 2022. Meanwhile I collect dividends and if a stock closes at a price higher than my cost basis, I also stand to get capital gain. The ‘finalRet’ column show my total return if that position would expire at today’s share price. Many of the positions show slight negative returns today but that would improve as I expect stocks to gain from here on out over the next two years. Let’s see how it goes.

Not a wealth generator: It’s important to make a key distinction here. These hedged positions are not expected to beat the overall stock market over the long term (five years or longer). Ipso facto, I would never consider keeping anything beyond my dry powder cash in this asset category. Majority of my portfolio continues to be invested in public stocks. That is where I expect to generate majority of my long-term returns.

To drive this point home, here is one final table I want to share:

In the three years since I started investing in these hedged positions, my cumulative total return (including all dividends) has been 11.03%. For the same duration—and even with two market corrections and the ongoing bear market (that drove stocks down by 35% at one point)—the S&P 500 cumulative return has been 37.26%. A whopping three times higher than this dry powder approach—albeit with much higher volatility as evident from previous charts. Though, I am good with this meager 11% return since it serves its purpose well. That is, it returns higher than a bank account and with reasonable liquidity/stability so I could withdraw whenever I am ready to buy stocks.

Thank you for sharing both the strategy and the performance.

I am curious what tool did you use to generate that snapshot of your hedged positions?

–Mike

This is a custom web app that we’ve developed to monitor our structured investments. It is not a standard tool available from brokerages. We use Interactive Brokers’ web APIs for this, and then do our own processing to present data in our preferred format. If there’s interest in this, I would do a blog post on this in future.

— emcee