I prefer investing in established well-run businesses that have defensible business models. Even though some of them are technology companies, I invest in them not because they are considered tech but because they have dug some level of economic moat around their businesses. You can see my portfolio here.

I understand technology very well—I worked with computers all my working life. And yet I tend not to invest in rising new tech startups. It’s not that they are not in my circle of competence. It’s mainly because most high-growth technology companies that make it to an IPO tend to be overpriced and speculative. There is a reason why IPOs are jokingly called It’s Probably Overpriced!

In recent years, the closest I’ve come to investing in a tech IPO was Facebook (FB). Still, that was months after its IPO and after its share price had fallen well below its IPO price.

I did buy Amazon in March 2000 but that was nearly three years after its IPO, and it had already gone up about 4x when I made that first buy. I didn’t consider it a startup investment then. As I wrote about it in a previous blog post, that purchase was mostly influenced by the Internet hype of the era.

What about those yet-to-be-public pre-IPO companies? Unfortunately—and even if we want to invest in them—individual investors don’t have easy access to them either. Those are usually funded by Venture Capital (VC) firms (companies such as Andreessen Horowitz) These VC firms typically raise capital from institutions, endowments, and wealthy family offices. Individual investors can’t invest directly.

There are some mutual funds and ETFs that buy small stakes in pre-IPO startups. However, there aren’t many and their public holdings easily dwarf any private investments. It is my understanding that mutual funds are allowed to invest in private businesses—it’s just that many don’t. One big reason is liquidity. Stakes in startups are not very liquid—funds cannot sell them on short notice to generate cash for redemptions or other investment opportunities.

There are also crowd-sourced funding platforms. They can take capital from small investors and let them invest in startups. But I stay away from them. These platforms don’t really have access to premier high-quality startups. Those still just go directly to big-name VC companies where they not only get capital but also their expertise and influence.

The bottom line in terms of investing in startups is that I neither have good access nor right skills to identify promising rising stars. Those few among many who could turn out to be future Amazons, Googles, and Facebooks of the world.

Enter SoftBank Group (traded in US as SFTBY or 9984 on Tokyo Exchange). This is not a new company. It was founded in 1981 in Tokyo and went public in 1998. It has gone through several major business transformations since then. However, one thing that has remained unchanged since its start: Its founder CEO, Masayoshi Son, is still at the helm. The company started out as a distributor of packaged software, went into Internet publishing in the 90’s, and then became a mobile broadband operator in the mid-2000s. Today, it’s a holding company with subsidiaries running mobile phone services in Japan and US, has direct investments in major Internet related businesses, and operates the world’s largest VC fund that is focused on tech startups.

What made me interested in SoftBank is its founder CEO and his focus on pre-IPO technology investments. Given our otherwise lack of access to good quality startups, this could be an opportunity to indirectly invest in them via SoftBank. I don’t know of any other public investment vehicle available today where individual investors could do that.

Masayoshi Son has been a tech entrepreneur and an investor for nearly 40 years. His biggest success story was his investment in Jack Ma’s Alibaba (BABA) in the year 2000 when it was still a tiny private company. He kept nearly all his stake since then—today SoftBank’s share in Alibaba is worth about $116 Billion. Masa also sits on Alibaba’s board and has been a good friend of Jack Ma (Alibaba’s founder).

I had previously heard of SoftBank in other contexts, but I had never paid much attention to it. Even recently, as SoftBank was being covered more widely in the US media, I wasn’t sure what to make of it. I was tempted to dismiss Masa Son’s Alibaba investment as one big lucky break for him—likely not to repeated in future. But as I researched him more, listened to his interviews, and read SoftBank’s annual reports, I realized that he is more than just a one-lucky-break guy. While Alibaba was hands down his best performing investment so far, he had also made other successful investing moves.

He is sharp, tech-savvy, and long-term oriented. When I hear long-term investing, I think ten to twenty years ahead, but Masa talks about his 300-year plan for the company. It’s hard not to laugh at it—and I suspect he’s only half-serious whenever he brings it up—he often reminds people that there were many dynasties in Asia that lasted for 300 plus years. But aside from his grand 300-year vision, the guy has had other notable successes besides Alibaba. In 1996, he created a joint venture with Yahoo! Inc. to establish its Japanese subsidiary, Yahoo! Japan. Today Yahoo! Japan is a profitable public company and a very popular Internet portal. By some accounts, more popular than the Google Japan site.

In 2006, Masa bought a struggling third-string mobile-phone operator from Vodaphone Japan, and over time made it a profitable well-run business (Softbank Corp.) known for offering cutting-edge products and services. In December 2018, Softbank Corp. (SOBKY) was spun off in the largest Japanese IPO ever.

Masa was also an early believer in the iPhone and convinced Steve Jobs to let him license it exclusively for Japan. In July 2008, SoftBank became the exclusive Japanese operator to offer an iPhone.

Today, Masa’s grander vision is to turn SoftBank into a premier tech investment manager by taking substantial stakes in rising tech startups—those who are best positioned to succeed in an increasingly AI-driven (Artificial Intelligence) data-enabled business world. And act as a catalyst for increased collaboration between his companies. He calls it his “Cluster of No. 1 Strategy”. He only invests in late-stage funding rounds where he could invest a minimum of $100 Million in businesses that have already developed leading market share positions. He prefers to become the leading outside shareholder in each but not take a controlling stake. He doesn’t believe that owners/founders of startups would be willing to give up control. He’s content with playing the role of an advisor and an influencer.

Masa Son’s reputation and financial interests are certainly tied with SoftBank’s shareholders. He, after all, has run this business since its inaugural year in 1981. He owns 22% of the company and takes only a modest salary every year. Clearly, he’s incentivized to make the SoftBank’s strategy successful. From what I could tell, he’s still very passionate about running SoftBank. So much so that his heir apparent, Nikesh Arora, left the company two years ago because he felt Masa was not ready to give up control. I like it that Masa is not yet ready to hand over his company’s reins. As I explained in a blog post last year, I like passionate founder-owners. I own several businesses that are run by founder CEOs.

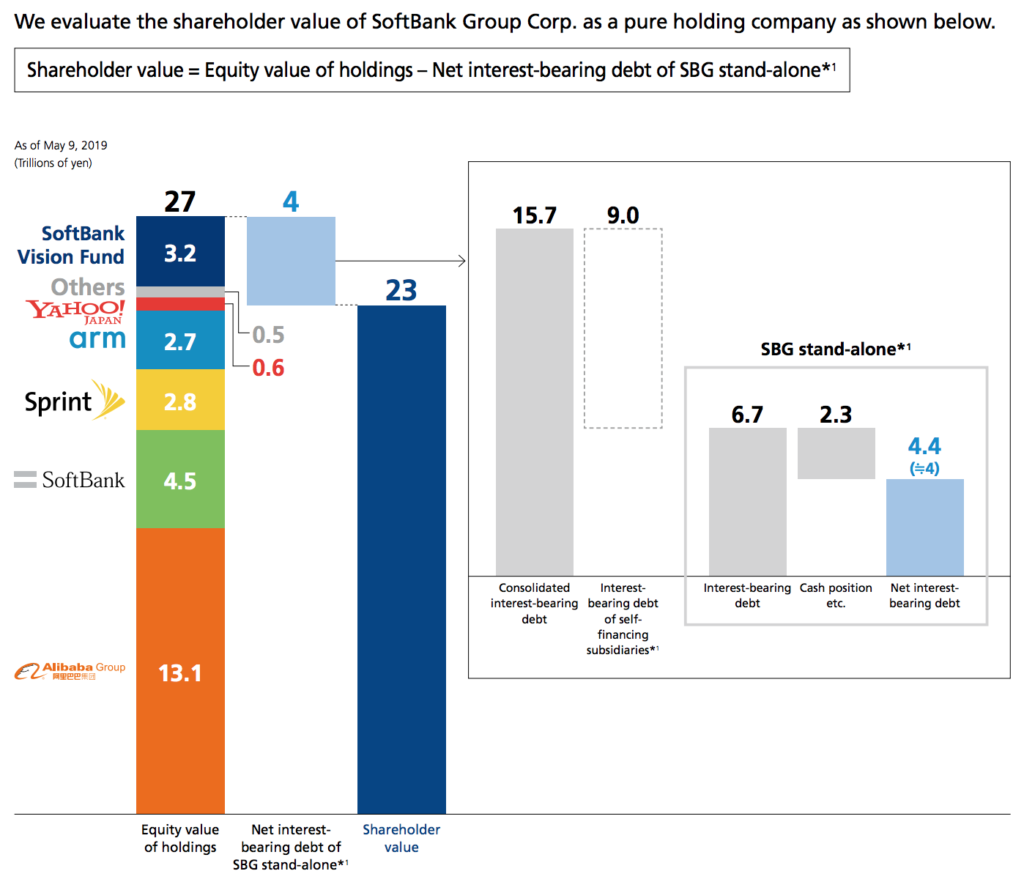

Valuation: What intrigues me further about SoftBank Group is its current valuation. Since it has transformed from an operational business to an investment holding company with large stakes in other public/private businesses, it’s best to value it on sum-of-the-parts (SOTP) basis. Many of SoftBank’s current holdings are public entities, and so their valuation can be measured off of their current market values. Alibaba is its largest stake and itself accounts for nearly half of SoftBank’s total equity. See the chart below taken from SoftBank’s recent annual report. Other significant public holdings include SoftBank Corp., Sprint, and Yahoo! Japan. Two of its biggest private holdings are ARM Technologies (which it acquired in 2016) and the SoftBank Vision Fund (SVF) where it manages third-party capital.

I won’t bore you with details here. The SOTP valuation has been independently done by others recently. See these links from Barron’s and Morningstar’s. Barron’s and Morningstar’s analyses are in line with SoftBank Group’s own analysis, pegging its value at about 30% to 50% higher than where it is trading today. More precise valuation is difficult given some of its holdings are private entities. SoftBank’s own SOTP analysis doesn’t take into account capital gains tax it may have to pay on Alibaba’s stake (if it ever decides to sell), while Barron’s/Morningstar’s do include it.

But regardless, it’s clear that today SoftBank Group is trading at a significant discount. In fact, its overall market cap of roughly $100 Billion today is just about the same as the value of its 25.8% Alibaba position (not counting taxes). Notwithstanding the rest of its businesses.

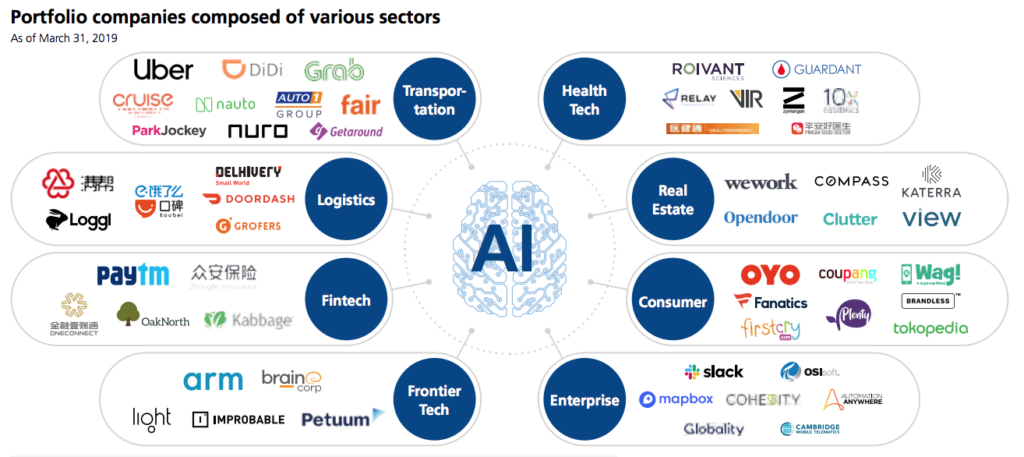

SoftBank Vision Fund (SVF) is where Masa Son is focused today. In a recent interview, he said that today he’s 97% an investment manager and only 3% an operations guy while it was nearly the opposite a few years ago. His operational businesses like Softbank Corp., Yahoo! Japan, and Sprint are now run by his deputies. Some of them have also been spun off to public. They are still good sources of cash flow to the parent firm, the SoftBank Group. It’s the Vision Fund where he has institutional and sovereign capital—along with $26 Billion of SoftBank’s own money—invested in a variety of young tech startups. There are too many names to count here, but the list also includes major names like Uber, Slack, WeWork, Didi, DoorDash, etc. His goal is to invest in market leaders, push them to aggressively develop their products, and encourage them to work with each other to increase market share.

In many ways, this is similar to what private equity (PE) managers do. (I wrote about Blackstone and Brookfield before.) One key difference being SVF not taking controlling stakes in any company, and not using debt financing. Instead of debt, SVF has sold preferred shares to its investing partners that yield 7%. Like other PE firms, SoftBank gets 1% management fees and 20% performance fees over a minimum hurdle of 8%. Also like other PE firms, I expect that SVF will gradually get out of companies that have gone public—such as Uber and soon WeWork—and recycle capital to younger upstarts.

The inaugural Vision Fund is nearly fully invested and SoftBank has already announced a follow-on fund, the Vision Fund 2. It’s also possible that SoftBank may decide to offer the first SVF to public via an IPO. This would lead to more capital inflow and enable SoftBank to invest in future funds.

Investing in SoftBank Group is essentially a bet on Masa Son and his acumen for identifying tech superstars of future. But let’s not forget that for every dollar invested in SoftBank, we also get 40 to 50 cents’ stake in Alibaba. I like this setup. I have never owned a Chinese company before. And Alibaba is arguably the best public enterprise in the greater China. And its market cap shows it too.

There are risks associated with a SoftBank investment. First and foremost—given that it’s positioning itself as an investment holding company—there is significant risk with the next market downturn. How many of the tech startups would survive a slowing economy and tightening capital? Only time will tell, but I like SoftBank’s chances better than any other pure-play VC fund. It has cash flow generating subsidiaries in form of mobile operators, Internet portals, and not to forget, a sizeable stake in Alibaba.

There is reputational risk just like with any other fund manager. If SoftBank make one or two big mistakes in investing its partners’ capital, it would become much harder for it to raise funds again. Along the same lines, there is also key person risk with SoftBank. Masa Son and SoftBank are forever linked with each other. If something happens to Son or he steps away, SoftBank would take a big hit. Those would be big shoes to fill for his successor.

Finally, there is also telecom industry risk with SoftBank given its controlling positions in SoftBank Corp. and Sprint (US mobile operator). The Japanese operator, SoftBank Corp., is a good source of cash flow but Sprint has not done well under Masa so far. T-Mobile’s takeover of Sprint will allow SoftBank to reduce its stake but it’s still pending regulatory approvals.

I took a small first position in SoftBank this month. It’s a high-risk speculative investment but I still like its odds of success. On one hand I believe in the high-tech area where Masa Son is investing. But on the other hand, I have been through the tech boom (and bust) of the late 90’s. I understand the pitfalls of investing in promising but still unproven business models. I plan to monitor SoftBank’s progress closely, and I might increase my stake gradually as I gain more confidence in its evolution. Now that I am a shareholder, I am rooting for Masa-san’s success!

Sven Carlin just posted a video with an analysis of Softbank, you should check it out: https://www.youtube.com/watch?v=2hk7NJTZZM4