What a quarter that was! The US stock market first reached a new high in October and then dropped 10%. It bounced around for a while. And then in late December, it dropped again—this time more than 15% off its peak. By some measures, it actually dropped 20% briefly (intra-day) before recovering some. I was able to deploy my first 10% tranche of dry powder and then another 20% when the market dropped below 15% from its high.

Looking back further, the entire year was quite interesting. Recall that stocks had done well in January and then dropped 10% by early February. That was the first time I was able to buy more stocks with my dry powder cash. And then the market took nearly six months to recover—only to give it all up again in the last quarter. Such are the vagaries of the stock market!

As readers would know from my previous blog posts, I don’t try to anticipate what the market will do next. Neither do I emotionally attach myself to one specific outcome. I set up my investing plans ahead of time and follow through whenever some milestone is achieved—or some hurdle is overcome. I prefer rule-based mechanical approach to investing that does not rely on intuitions or impulses.

Why stocks dropped in December? I like to listen to Ken Fisher’s market analysis. His commentary on the state of the stock market is always very insightful. Fisher is among the few investors whose advice I highly respect. He suggested in a recent interview that this sudden late December market drop could have been caused by hedge funds that were trying to wind down their funds before the year ended. The reason for the wind down, he speculated, was that they were way under their high watermarks, and it was no longer viable to keep them running profitably. All that selling caused the big market drop. It would be interesting if it turns out to be true. Nevertheless, this is only of peripheral interest to me. My investing style does not rely on correctly predicting near-term stock movements. See Ken Fisher’s podcast here.

I have a dry powder cash strategy where I keep a portion of my portfolio in cash—ready to deploy when stocks go down. I have previously written about it here and here. This fourth quarter of 2018 was second such quarter in the year where I was able to invest a portion of this cash. I deployed the first time in February and then replenished cash by selling some stocks by October when the market had hit a new high. This chart shows where I deployed (and replenished) the dry powder cash in 2018.

By some measures, the market breached the 20% hurdle in December. Per my dry powder rulebook, that would have triggered the next tranche (30% of cash) of buying. However, it happened on the Christmas eve December 24th and only for a couple hours—a day when most investors were elsewhere. I didn’t get to take advantage of that drop either. Since then the market has steadily climbed up. Looking back, do I regret not being there—ready to buy some more? No. I am a patient investor. I might have missed an opportunity to buy at even better prices. But I know that the market drops frequently. There will be other such opportunities down the road.

I have been using the S&P 500 Price Index (SPX) to measure the market performance since it is widely quoted everywhere. This doesn’t include dividends though. For that, you’d have to switch to another index S&P 500 Total Return Index (SPXT). In 4Q 2018, SPX went down approximately 20% from its peak while SPXT went down by about 18%. To measure short-term movements, it doesn’t really make much difference which one I use. However, for long-term measurements, it is best to use a total return index such as SPXT. As I wrote in this post, Revisiting the lost decade of U.S. stocks, dividend reinvesting makes a big difference when one invest for a decade or longer.

The S&P 500 is also a large-cap stock index representing top 500 U.S. public companies. If I measure the market performance of small-cap stocks (represented by the Russell 2000 index), the market was actually down a lot more (about 28%) in December. If I measure only the mid-cap stocks, the S&P Midcap 400 index was down by about 24%. You can see that the market was worse for the small and mid-cap stocks than the large-cap ones. Overall, the entire US market as measured by the Morningstar US Market index was down by 20%.

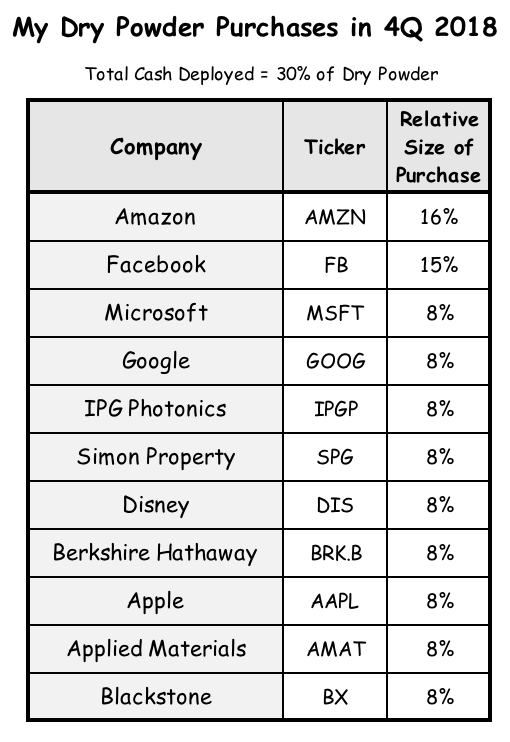

Regarding my February stock purchases, I wrote about them in a previous blog post here. This last quarter, I purchased more individual stocks. None of them were new to my portfolio. I just added to my existing positions. See the table.

I consider all of them to be good long-term franchises. I expect them to continue to reinvest for growth, and in some cases return a portion of their earnings via dividends and buybacks. Many of them have already done well for me over the last ten years but these buys were forward looking actions. I expect them to continue to do well for the next five years.

I have written about many of these businesses previously. See the links here: Amazon, Facebook, IPG Photonics, Simon Property, Disney, Berkshire, Apple, Blackstone.

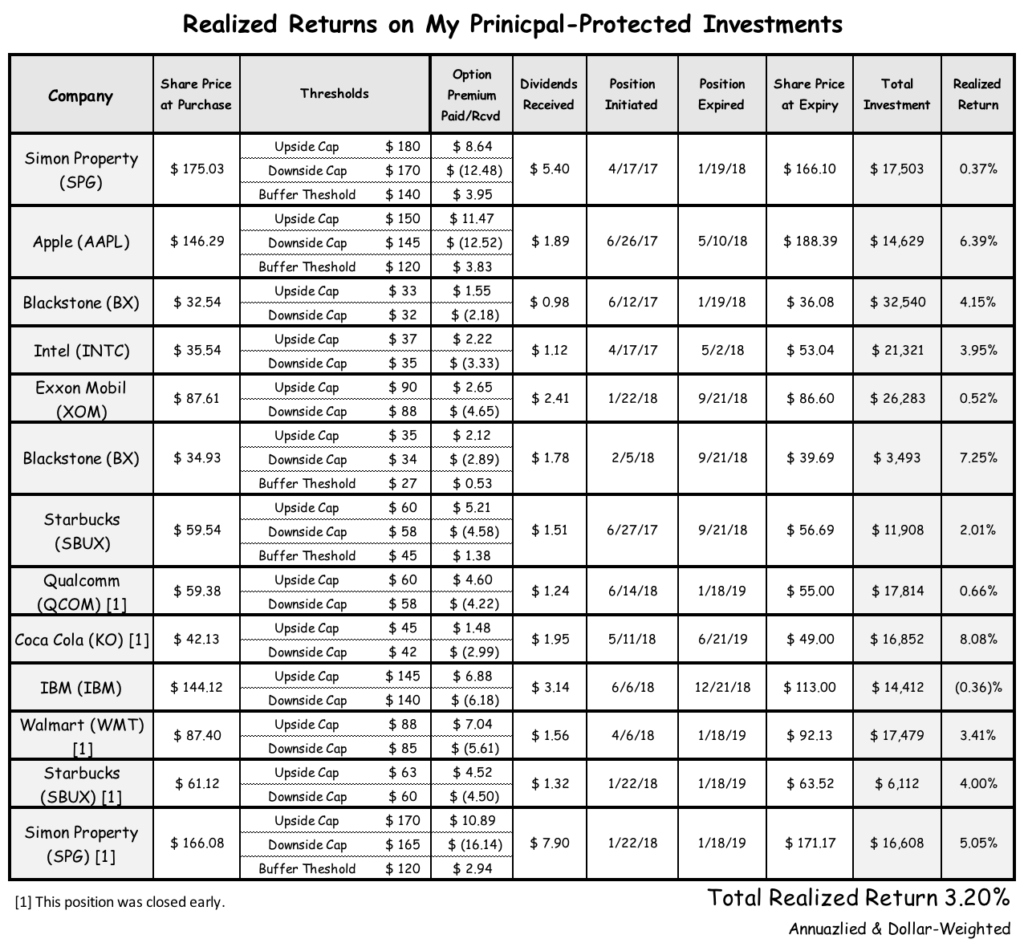

Return on Cash? Next, some words on my cash returns. You may recall from my earlier posts that I keep cash in my portfolio for two reasons: As rainy-day funds and for my dry powder buying. As I explained in my post on portfolio benchmarking, I have an investment strategy for my cash that allows me to participate in stocks’ upside growth (up to an extent) while keeping the principal protected from a downturn. In other words, it is like a market-neutral strategy with some upside exposure. These positions are tied up for 6 to 12 months at a time, but I stagger them so every 3 to 6 months, I can liquidate some positions if I need to.

I previously wrote about this market-neutral strategy in my posts in July and in January last year. As I reported in the January post, at the time my positions were yielding a return of 3.87% (annualized). Since then, as positions expired and cash was released, I opened new positions. I started this options-based strategy about two years ago (first position opened in April 2017) and since then my realized annualized return has been 3.20% (dollar-weighted). See details in the table below.

This 3.20% return is nothing to write home about! But still keep in mind that I took no principal loss risk and no long-term capital lockup. This is what I wanted because this cash could be needed on a short notice, as we saw in the last quarter.

As for my current principal-protected positions, expected aggregate return would be in the range of 0.3% to 6.3%. If all my stocks cooperate (and my toast falls jelly-side up), I could make a very decent 6.3% return. Worst case if stocks tank from here, I might just about get my principal back—or 0.3% gain if you are a nitpicker. In a future post, I will share more details on this.

Leave a Reply