Last week, John Rekenthaler of Morningstar wrote an article on worst alternative investments of the decade. Market-neutral funds were among his top-five worst investments. Average annual return from the funds in this category was 0%. He wrote this, tongue in cheek:

… Market-neutral funds gently fluctuated around a mean of zero. (Perhaps they should be called “return-neutral” funds.) So gently that the category never gained nor lost as much as 3% in any year. One needs to pinch the funds to ensure that they are alive.

What exactly are market-neutral funds? These funds try to generate steady — albeit low — returns that are independent of how stock or bond markets perform. Most of them employ a long/short strategy to drive returns — short some stocks and go long on others. By offsetting longs by shorts, they try to generate profits independent of how stocks move. Others try to profit from corporate events like mergers and spinoffs. But the overarching idea is that same — generate steady returns in all kinds of market environments.

These funds’ low return variability might appeal to some novice investors for the so-called ‘peace of mind’ but the price paid for it is too high. The returns don’t change much year to year but when the average return hovers around zero, it does not look attractive from any perspective. Generally speaking, these funds don’t have a place in a long-term minded individual investor’s portfolio.

Morningstar tracks about 140 different funds in its market-neutral category. Their average return over last five years has been a paltry 0.59% with the three-year record equally dismal at 1.19%.

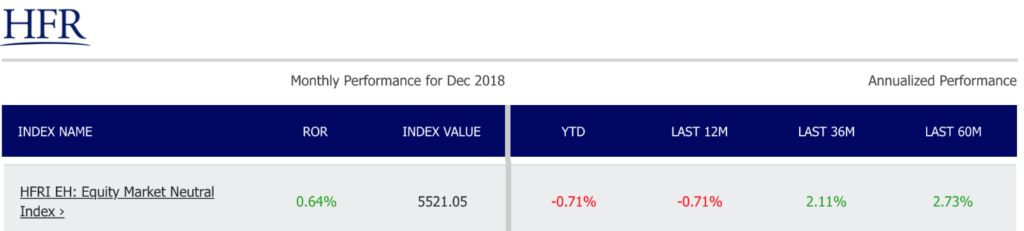

There are also market-neutral hedge funds out there. Hedge Fund Research, Inc. (HFR) publishes data on these. From their numbers, the mean annual return of the Equity Market Neutral index for the last 60 months has been 2.73% — last three years is 2.11%. Not very confidence boosting either but a shade better than the Morningstar’s index. Keep in mind though that most of these hedge funds are out of reach for individual investors — they cater to institutions primarily.

Along these lines, I also checked out Joel Greenblatt’s Gotham Funds family. Greenblatt is a very well-known investor — someone who I also greatly admire. He’s written some outstanding books for small investors. Among them are The Little Book That Still Beats the Market and The Big Secret for the Small Investors – two books that I’d highly recommend to every aspiring individual investor. Among a variety of funds Gotham has available, there is also one market-neutral fund called Gotham Neutral Fund (GONIX). Naturally, I went looking. Unfortunately, even its long-term performance has left much to be desired. Since inception in August 2013 and after adjusting for fees, it has only returned 1.05% annually — 1.44% in last 36 months. This does not look too appealing either.

Why do we care about market-neutral funds? Most of us, individual investors, shouldn’t. These market-neutral funds come with a big caveat. They won’t ever come close to the common stocks’ long-term superior performance. In fact, Morningstar measures their performances relative to the 12-month Treasury Bill index. In the last five years, the S&P US Treasury Bill 9-to-12-month index has returned an average of 0.81%. That’s how low the performance expectations are!

If we don’t care about them then why am I still talking about them? Two reasons: First, it doesn’t hurt to study other types of investments that are offered to investors (even if we may not want to take advantage of them). Second, there is one possible situation where my portfolio could consider investing in these market-neutral strategies.

You see, I have a dry powder strategy. I won’t bore you with all the details since I’ve written multiple times about it in this blog. Read these posts to catch up: I use cash as dry powder and Revisiting my dry powder strategy

That cash I keep as dry powder has an opportunity cost associated with it. I never know when I might need it. So I need to keep it semi-liquid (not tied up for multiple years at a time) and at the same time, it would be good to generate higher-than-cash return from it. Enter market-neutral strategies. Because the historical performance of market-neutral funds has not been stellar, I’ve developed my own home-brewed long/short options-based strategy. See Get more out of your cash for details on this.

What I needed was a strategy that allowed me some upside exposure to stocks but very limited (or no) exposure to their downside. Isn’t this what all investors want? Yes – we all would prefer to minimize our downside exposure if we could. But as we see with market-neutral funds, limiting downside risk also limits upside reward — and rather severely. I would never want that for my portfolio. Limiting upside to single-digit returns in the best of times is not the road to success. But for strictly my dry powder cash, I’d accept a strategy that nearly eliminates my downside risk while still let me participate in some upside reward when stocks move favorably.

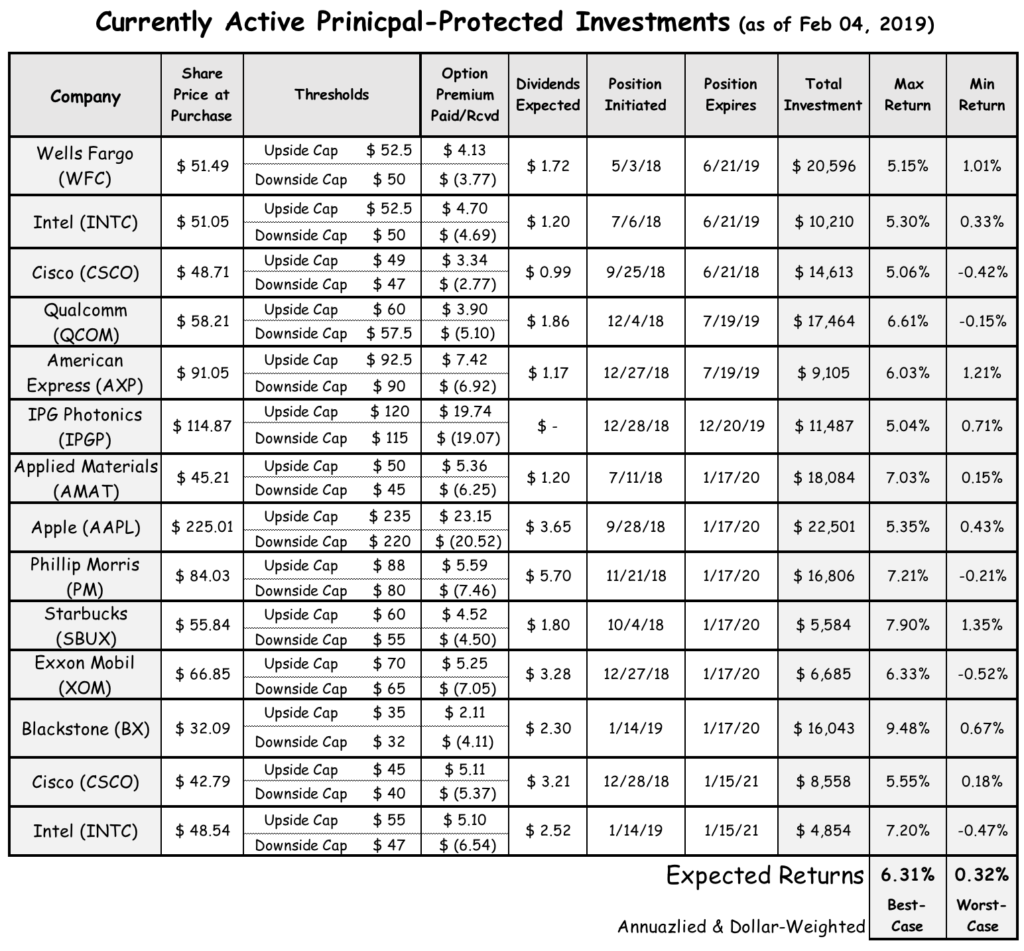

In my previous post, Investing Amid Volatility, I showed realized returns so far from this some-upside/no-downside options strategy. Those were positions that had expired already. Below table shows my open positions where a range of outcomes is still possible. As I pointed out in that previous post, I could capture an upside of 6.32% (annualized) if the stock market moves up — or I could barely break even (0.32%) if stocks drop from here.

You might ask: what’s the catch here? It doesn’t seem right that I could earn a positive return that is higher than any short-term liquid asset (such as CDs, Bonds, Money Market, etc.) while not getting exposed to the downside risk of traditional risky assets (such as common stocks, long-term bonds, etc.) It turns out that there are indeed some hidden risks. Let’s look at them one at a time below:

What if all my long stock positions drop below my cost? That is not a risk per se as this possibility is already accounted for in my worst-case return calculation. If a stock drops below its Put strike price (no matter how far below) when the position expires, my long Put position will compensate me proportionally. In other words, my loss will be limited by my long Put strike price.

What if dividends are cut? Note from the table that I am counting on dividends to make me whole when my stock position doesn’t deliver. Dividend cuts don’t happen very often. Full suspension of dividends is even rarer. And the companies I take positions in are all sound businesses. Chances of any one of them reducing or eliminating dividends are pretty slim. But still, I calculated my return for such a scenario where all stocks expire below my bases and all of them cut off dividends. In this unlikely but still possible scenario, my total return would be -3%.

What if these businesses go poof? It wouldn’t be any worse than the dividend-cut scenario. Why? Because holders of Put options still get paid even if a company goes bankrupt. See the explanation from The Options Clearing House (OCC) here. Similar outcome is expected in case a company is acquired, goes private, or merges with another. I might not get remaining dividends, but my option contracts will still keep me protected below the downside threshold.

What if my short Calls are called early? Remember that I buy Put options and sell Call options. Since I am short Calls, it’s possible that the Call holder (my counterparty) might exercise it early and force me to sell my shares at the Call strike price. But this only happens when those Calls are in the money — meaning that the underlying shares have gone up and beyond my strike price. In other words, if my Calls get exercised prematurely, that means I’ve already gotten maximum capital gains out of my shares. So, it would be OK for someone to take them away from me. I’d miss remaining dividends, but my position would also close profitably. I won’t lose money when that happens.

To wrap up this discussion of risk factors, I suppose it would be more accurate to say that my absolute worst-case return from current positions could be as bad as negative 3% (annualized) rather than positive 0.32%. However, as I explained earlier, this is a highly improbable scenario. I expect these investments to generate somewhere between +0.3% to +6.3%. This is the likely range. Getting the low-end of the range would mean that most (if not all) of these stocks have gone down in value. Likely because the overall stock market has gone down as well. That would be a time to make this near-cash work for me.

Before closing this post, I should also mention that there are certain other market-neutral investments out there. Many of them are only accessible to accredited investors and also carry high management fees. I am referring to the various kinds of structured notes that large investment banks offer to their clients. These notes also offer similar risk-reward tradeoff like my long/short protective-collar strategy. I’ve researched them in the past and decided not to invest. In a future post, I will spell out my analysis and reasons for passing them over.

Market-neutral investing could only serve a very limited purpose. In my case, I use it for dry-powder cash that is awaiting market corrections. Nonetheless, the vast majority of my funds are in stocks, stock index funds, and real-estate. These are the assets that have unbounded growth potential — as I long as I remain steadfast when facing near-term volatility. I wouldn’t recommend anyone go all in on market-neutral funds. Your returns will be severely diminished.

Hi

I appreciate that you use your option strategies to achieve some return on your dry powder reserves, but presumably short term bonds would also provide a small, but safe return if you did not wish to enter into option strategies

BTW I agree that market neutral funds generally have a lack lustre performance as do most real return funds

I agree. Short-term bonds would be a fine way to keep dry powder cash (until you need it). With my option strategy, I am hoping to generate a bit more return but it does take more effort and time. Not everyone has time or inclination to get into them. Happy investing!