The median tenure of public company CEOs is about five years [1]. They come and go. Many of them are paid handsomely to run a company—in either cash or stocks that vest in 3 to 4 years. They’d own some shares while they work for the company and then cash out as they leave. They might be incentivized to see that the company do well for a few years, but they are not there to make long-term strategic decisions for the business.

The median tenure of public company CEOs is about five years [1]. They come and go. Many of them are paid handsomely to run a company—in either cash or stocks that vest in 3 to 4 years. They’d own some shares while they work for the company and then cash out as they leave. They might be incentivized to see that the company do well for a few years, but they are not there to make long-term strategic decisions for the business.

On the other hand, I, as a long-term investor, have a much longer time frame in mind. I would rather hold my shares longer than 3 – 4 years and let the magic of compounding take effect. Unlike many CEOs, I don’t get paid much in the near-term. Unless the stock pops for some reason but I don’t count on such things. Majority of my gains come from the steady growth of a business that produces consistent profits. Profits, that are either reinvested for future earnings or returned to shareholders. It is this compounding effect of reinvesting that builds wealth over time.

So, I am always looking out for long-tenured business leaders who also have significant skin in the game. It’s even better when it’s a founder-led business where he (or she) is still at the helm and has a long-held large stake in the business. Founder leaders who have spent their careers building a business are a unique class. Not only their personal wealth is tied to the business but also their reputation and legacy. Within that group, those leaders who have excellent capital allocation track record and good shareholder communications stand out even further. It is this select group that I am very interested in investing with.

I am happy to see these CEOs paid well for their contributions. I prefer that majority of their compensation is in form of long-dated stock awards—rather than cash. I am happier though if they refuse generous compensation. Especially those who are already very rich given their long-held large stake in the business. In an earlier blog post (CEOs who take pay cuts), I wrote about some CEOs who go even a step further and request a pay cut when shareholders are hurting. I consider this a good sign—they are thinking like us, regular share owners.

All of this do not imply that I ignore the quality of the business itself. After all, Warren Buffett said this once:

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

Business quality is first and foremost. Before I bet on a jockey, I first need to assess the horse. As an investor, I still need to do due diligence on other aspects of a business: its position in the industry, the industry prospects, its financials, economic moat around the business, etc. Basically, all the things that I’d do to assess any business that I am considering investing in.

There is another, often overlooked factor, that helps me stay invested with founder-led businesses. As I’ve written previously, I gradually build my stake in a company – taking advantage of inevitable share price volatility. All this time, I’d be paying attention to its management’s communication with shareholders—quarterly conference calls, business presentations, annual letters, media interviews, etc. Over time, I become familiar with the CEO. This connecting the company with a real person is helpful in times of stress. When share prices take a tumble, perhaps due to stock market downturn or some industry change or even a company specific event, I am no longer just focused on a three-letter ticker symbol and its fluctuating price. I take comfort in listening to the business leader who is invested in the company alongside us, the regular shareholders. If he’s been with the company long enough, he probably has been through similar situations before and I could trust him to steer the ship safely this time too.

Of course, not all founder led businesses will be successful. And when they do well, they won’t all be successful to the same degree. As I said before, good leaders are no match for poor quality businesses. Even outside the business quality concerns, there are two other key risk factors I see in founder-led businesses.

One is ‘key-person risk’. What if a founder leader decides to step down, pushed out by activists, or otherwise no longer available to run the company? Is there a good succession plan—someone ready to step up to the plate? For instance, even though Amazon could prove me wrong on this, I believe that Jeff Bezos is still key to its future success. It’s not clear to me as an investor how Amazon would fare in Bezos’ absence. Conversely, I think that Berkshire’s key-person risk is relatively low today. Buffett had many years to plan for this. And when he says he has a good succession plan in place, I tend to trust him.

Another risk is possible shifting motivations of a founder leader who’s already grown rich building his company. What’d happen if he is no longer interested in aggressively pursuing business growth. What if she’s satisfied with the status quo? This doesn’t happen often though. Founders are as much driven by their reputation and legacy as the pursuit of riches.

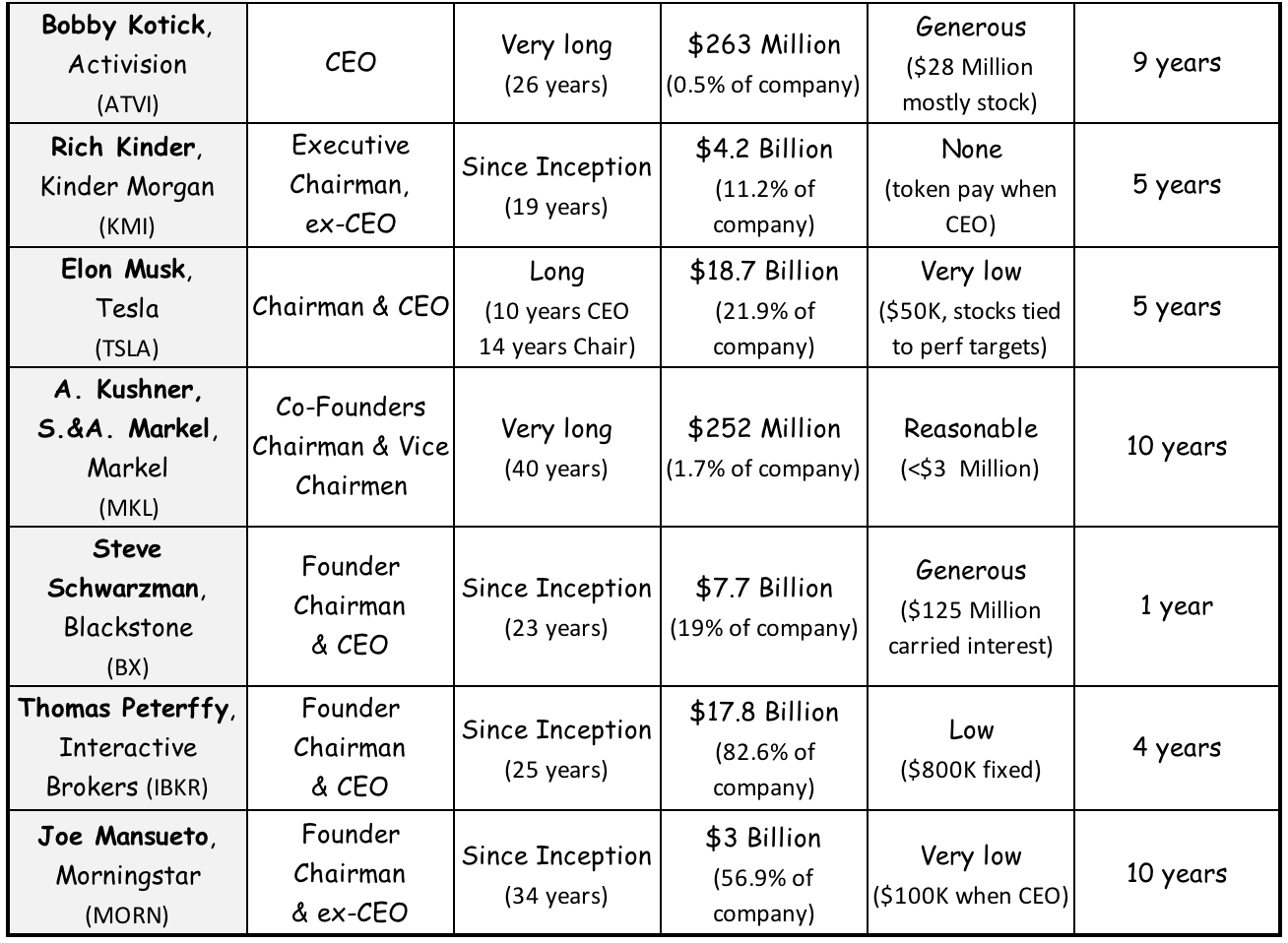

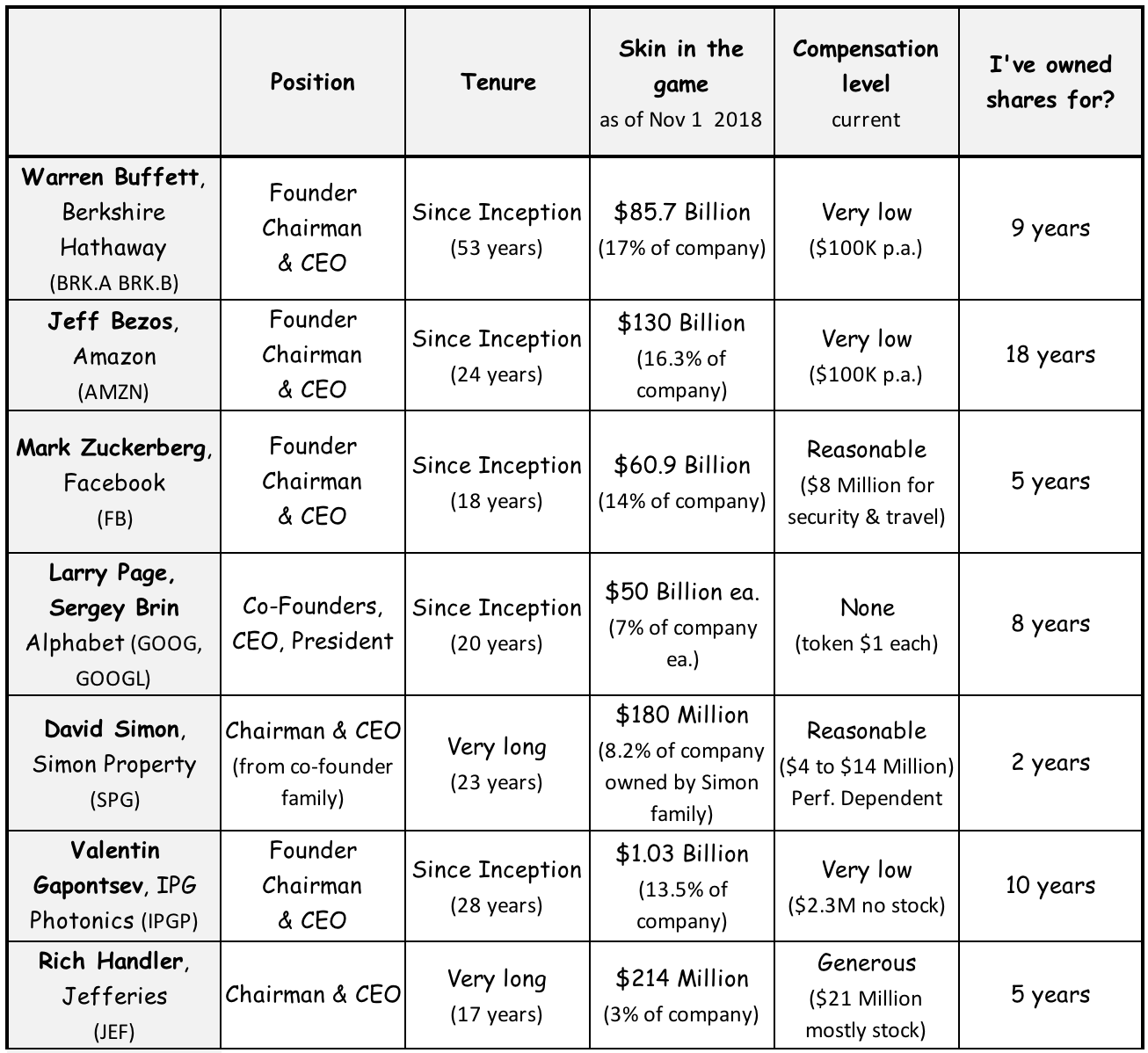

So, without further ado, here’s a list of all founder-led businesses I’ve invested in over the years. As you can see from the table, there are some I’ve been invested in for over a decade. Others are relatively recent investments. Not all of them have been runaway successes for me but I am happy holding all of these so far. I watch them closely, listen to managements’ updates, and on occasions add to my stake when prices are right. I’ve written about some of them in previous blog posts: Berkshire, Amazon, Facebook, Simon, Kinder Morgan, Tesla, Blackstone. In a follow-up post, I’ll write more about other aspects of these businesses. Those that I didn’t cover in this table such as how each founder’s stake has changed over time, their capital allocation track record, quality of shareholder communication, my assessment of key person risk, etc.

Leave a Reply