I just finished reading Semper Augustus’ 2023 shareholder letter. Chris Bloomstran, its well-known CIO, writes detailed annual letters. They are full of well-researched data and, while long, always make interesting read.

This year’s letter was no different. About a half of it was dedicated to a Berkshire Hathaway deep dive. It’s a major holding of his fund (and mine too) and I appreciated his research on the topic.

The rest of the letter covered various other topics but what caught my attention was his write-up on the so-called Magnificent Seven stocks. He titled the section, in jest I suspect, “The Fabulous and The Magnificent”. These seven companies are Apple, Microsoft, Amazon, Alphabet, Meta, Tesla, and NVidia. In his letter, he argues against owning these stocks for the next ten years. He doesn’t think they are market beaters anymore.

His main argument is not that the Magnificent 7 are at extremely high valuations (though it is one of his concerns). Or that their businesses are not durable. His primary argument against the Mag 7 is that their combined market cap relative to the rest of the S&P 500 constituents is too big to sustain.

As he pointed out in his letter, the Mag 7 have gone up from 8% of the S&P 500 in 2011 to 30% today while their share of the total profits has moved from 8% to 21%. In other words, the combined valuation multiple the market has assigned them has grown much faster than the fundamentals over the last decade.

He further writes:

What now? There is no way the seven stocks can be repeat performers … I simply find it nearly impossible that seven companies will earn more than a third of all index profits.

He concedes though that they are bound to grow from here (at what rate though?) Could they become even bigger share of the S&P 500 (and consequently the global economy) in the process?

Or would their future growth be hampered by regulatory authorities, new competitors, brand backlash, geopolitical tensions, etc.

He writes:

Paying 32.5x earnings at year-end 2023 for companies earning a 20.7% profit margin leaves little margin of error… I don’t find a single one of the Magnificent Seven safe enough at current prices to buy and hold for a decade or more.

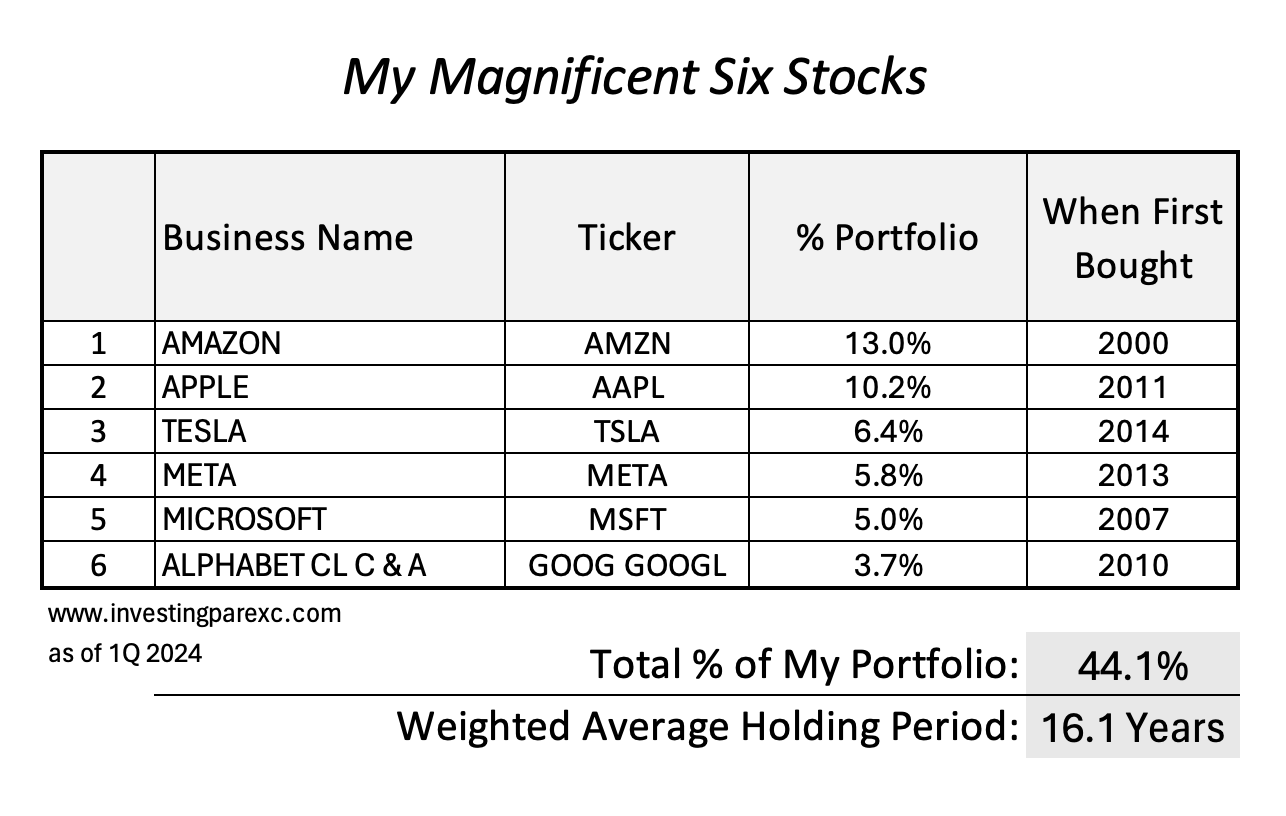

As I’ve noted in a previous post, I own six of the Magnificent Seven stocks. I like to call them my Magnificent Six. They are among my top-15 holdings. These six stocks make up about 44% of my portfolio today.

I own Amazon since 2000. And Microsoft since 2007. Then Alphabet, Apple, Meta, and Tesla, in that order. My portfolio’s weighted average holding period for these six stocks is 16.1 years. See this table.

I didn’t set out to make my portfolio such top heavy. It just happened over time as these stocks outran the rest of my portfolio in terms of performance.

Should I sell my Magnificent Six stocks in light of what Chris Bloomstran wrote in the letter? No, I don’t plan to.

Why? On the one hand, I understand Bloomstran’s concerns about their growth prospects. On the other hand, I have enjoyed their tremendous ride during the last sixteen years. Unlike him who gave up on Microsoft too soon:

We owned Microsoft for numerous years after the stock dropped 75% from its 2000 high and regrettably sold the position before their cloud business made the company again wildly successful.

I have large capital gains in these positions; some of them in taxable accounts. I follow these businesses closely and have good understanding of their business models’ strengths/vulnerabilities. I am also an insider, having worked all my professional years in the tech industry.

Another reason for holding on to these is that good companies tend to remain good companies, and poor companies tend to remain stuck in the mud. This was the conclusion from a 2013 Credit Suisse research report that studied 25 years of public company records. See this: Invest in High-Quality Businesses

Above all, I let my winners run. It’s not easy to find high-quality businesses run by excellent owners/managers. Clearly the six that I was lucky enough to pick more than a decade ago are among the best out there. If I dump them today for high valuations and uncertain growth prospects, where’d I invest the money? The risk of getting into bad new investments is higher than the risk of sub-par returns from one or more of these.

Two weeks ago, I returned from the annual Berkshire meeting in Omaha. While there, we learned that Berkshire has reduced its huge Apple stake by 13% in the quarter. Nevertheless, Buffett said during the meeting that he expected Apple would remain its biggest stock position. Even after this position trimming, Apple is a whopping 41% of Berkshire’s stock portfolio—a huge vote of confidence from the greatest investor of our time. My 44% concentration in the Magnificent Six (that also includes Apple) pales by comparison.

I suspect Buffett’s reasons for holding on to Apple shares are similar to what I’ve noted above. For further insight into when Buffett closes his stock positions, I searched through the CNBC archives of past Berkshire Hathaway’s annual meeting transcripts.

Buffett was asked in the 2009 meeting: How does he justify holding stocks forever when fundamentals have permanently changed? He replied that he didn’t always hold them forever. He said: We sell when:

- We made a mistake in our initial purchase decision or

- The business’s competitive position has significantly weakened or

- We lose confidence in the management.

He further added that when in doubt, our natural inclination is to keep holding. If we made the right decision in the beginning, we’d like to ride and hold on for decades.

On another occasion (2002 annual meeting), he was asked how he decides when to hold forever and when to sell. He replied that it’s not our natural inclination to sell. He would sell if he needed money for something else but that had not been the problem for the last 10 or 15 years. He said today he’d only sell if he was reevaluating the economic characteristics of that business.

Chris Mayer, another long-term investor, was asked about his fund’s position sizing in a recent episode of The Investor’s Podcast. Chris is the author of 100 Baggers and the co-founder and portfolio manager of Woodlock House Family Capital. I follow him for his thoughts on the power of long-term compounding in the stock market. I wrote about him and his book in a 2019 blog post: A Coffee Can Approach to Investing.

He responded [podcast: 00:54:10] by explaining that he doesn’t like to make an initial position bigger than 10%. But he’s also happy letting it compound and grow into a bigger position:

I think the source to outperformance comes from an investor’s willingness to let something become a bigger part of their portfolio. Let them really ride their winners.

He doesn’t like to trim his positions unless they become really egregious (in valuation).

So you can see that I am in good company when it comes to avoiding closing out my winners. I do trim a bit on occasions though. For instance, I recently sold small fractions of each of my top-10 positions (including the so-called my Magnificent Six). This was part of my recouping the dry powder cash—the capital that I had deployed during the 2022 bear market decline. Those incremental investments had since grown by 48% and as the market reached a new high this year, I trimmed some positions to recover the original cash.

I don’t plan to divest from my Magnificent Six holdings, notwithstanding Bloomstran’s dismal prognostications. The next ten years however will be interesting to watch.

Leave a Reply