The S&P 500 is a popular index among US investors who prefer hands-off dollar cost averaging way to invest in stocks. It is a market cap weighted index which is perhaps the most suitable form of an index for passive investing. Why? Because it does not require any rebalancing among the stocks that make up the index. If one stock does better than another, it will grow to become a higher proportion of it. Over time, relative weights of individual companies grow and shrink as their individual business prospects change.

There are other such market-cap weighted indexes available in US and other stock markets. I am using the S&P 500 as one example.

It is also like what happens when one buys a diverse group of stocks and hold them for a long time. No subsequent sales or rebalancing of each individual position. Over ensuing years, some businesses will be more successful than the others and thus become a bigger part of the portfolio. Others may also do well and yet still see their shares shrink because of relative underperformance. This is portfolio concentration.

Of late, the S&P 500 index is in the news more often for being too “top heavy”. Top five stocks make up about 23% of the index today. It is reportedly the highest concentration in the index’s top-five holdings since at least 1990.

Top seven stocks in the S&P 500 (termed Magnificent Seven by the financial press) have outperformed the rest of the index hands down in recent years. These few top stocks have contributed much to the index’s performance this year. According to IBD, the S&P 500 is up 11.7% so far in 2023 whereas its sister index the S&P 500 Equal Weight index is only up 0.3%.

The S&P 500 Equal Weight is an index that periodically rebalances all its 500 member stocks to be of same weight, unlike the more popular S&P 500 index which does not rebalance.

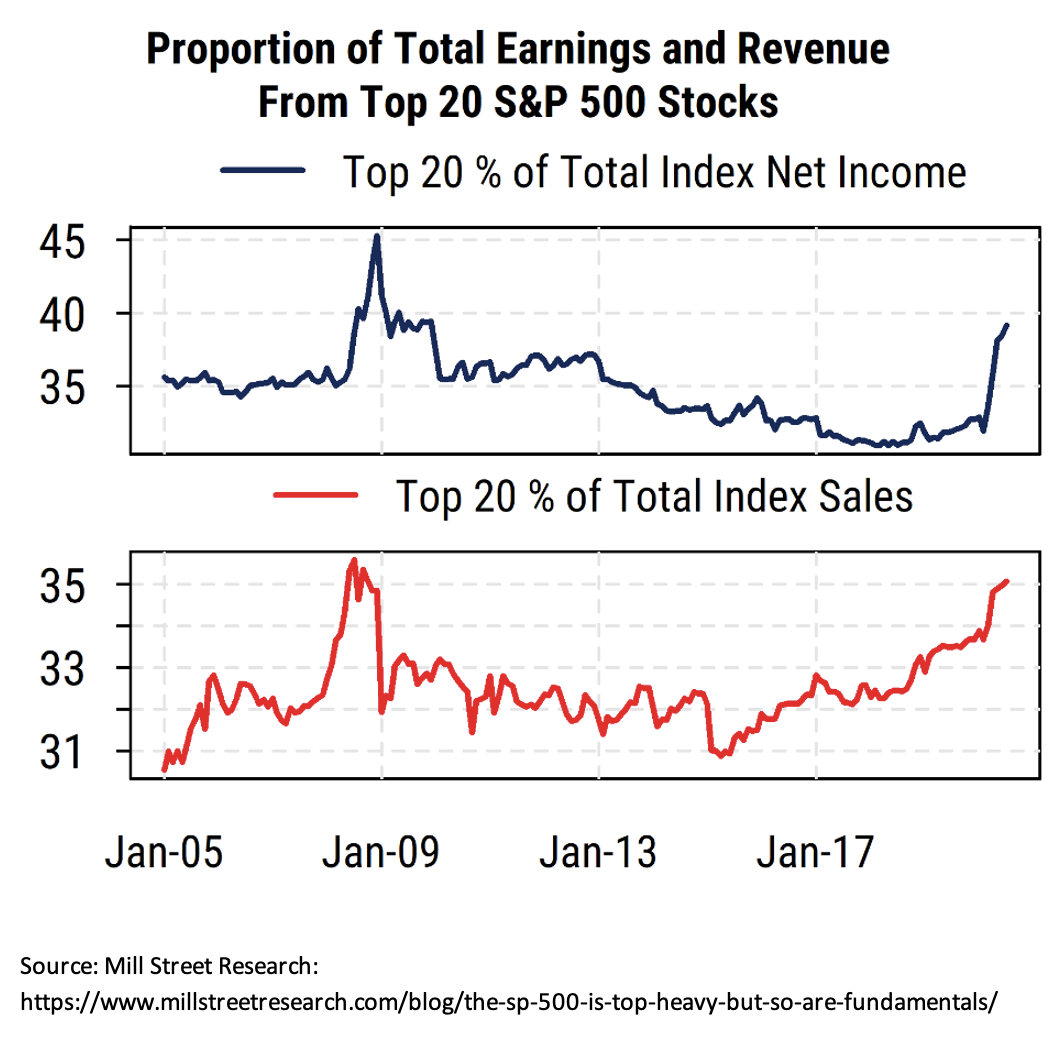

But this outperformance of a small set of stocks is not entirely unjustified either. These select businesses have also grown their revenue and earnings disproportionally. These companies have highly profitable and very defensible business models. The market recognizes their business strengths by valuing them higher than others. See from this chart how top 20% of the S&P 500 companies have contributed an increasing larger portion of the index’s overall sales and earnings. Today, top 20% of the stocks contribute nearly 40% of the index’s total income.

For sure, there are also some drawbacks to continue investing in a top-heavy index. For one, a top-heavy index tends to be more volatile. It is also less diverse. When one invests in such an index, more dollars go to buying these top stocks. When market falls, these top stocks could see bigger drawdowns, affecting the index disproportionately due its high exposure to them.

On the other hand, as I wrote earlier, these top stocks represent some phenomenally successful businesses. If I am a long-term investor with ten or more years of investing horizon, do I really want to reduce exposure to them? Paraphrasing Peter Lynch, selling my winners is akin to cutting the flowers. For more on this, see this post: My portfolio is getting top heavy

Over long periods, really good businesses outshine others. Naturally, their stocks also outperform. Exhibit A of this is Berkshire Hathaway’s stock portfolio. Warren Buffett has bought and held certain stocks for decades. Today, Berkshire’s portfolio is extremely top heavy. His top-five positions account for about 78% of his entire portfolio. Just one holding, Apple (AAPL), is about 50% of it. But he didn’t quite start out this lopsided. He bought bulk of his Apple stake in 2016 through 2019, investing $just 35 billion. Today, that position has more than quintupled and is worth about $178 billion. Buffett’s other big positions in Coca Cola (KO), American Express (AXP), and Bank of America (BAC) are multiple decades in the making and have also handily outpaced other small positions in its portfolio.

I don’t follow the Magnificent Seven but I have six of them (except Nvidia) in my top-25 positions. Magnificent Seven though is a just a backward-looking term any ways. When I was investing in these stocks, they weren’t called that. I picked stocks that I thought were durable businesses with good growth prospects. Some of them turned into these mega businesses.

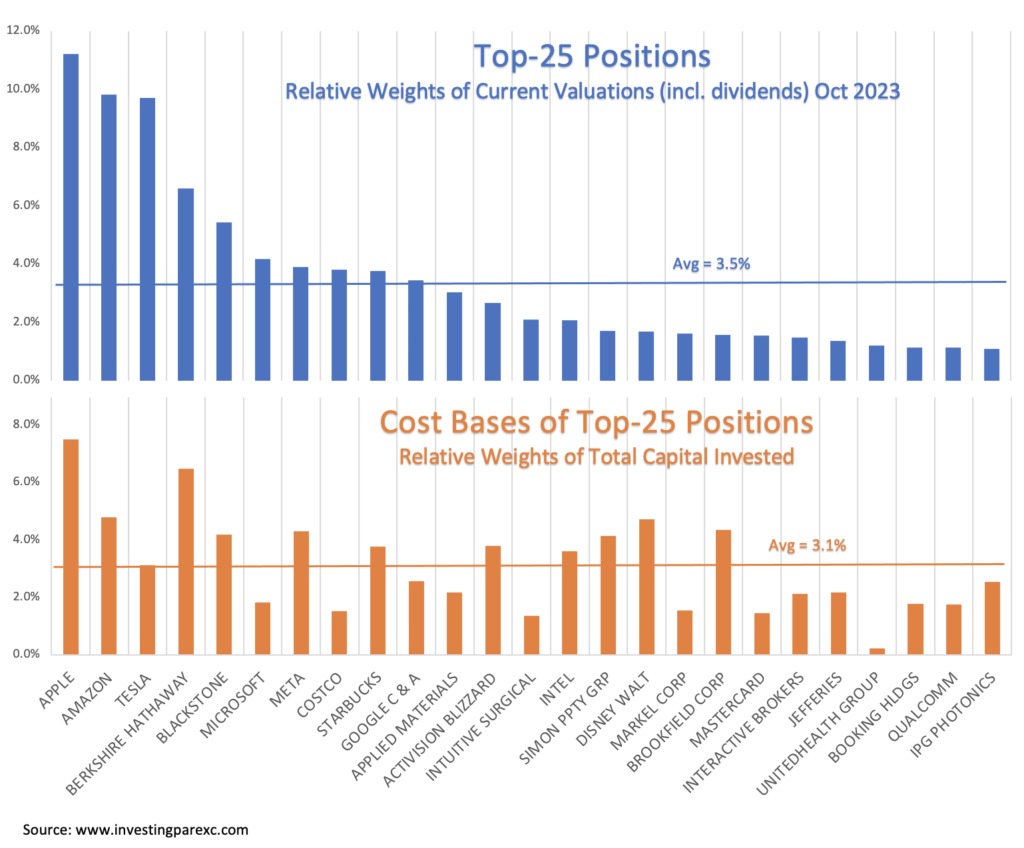

To give you a sense of how I historically allocated cash into my top positions, I share the following graph. The bottom bar chart shows how I allocated my capital into various stock positions over the years. These were my cost bases in these positions.

The top bar chart shows where each of those stock positions are as of today, relative to the current valuation of my portfolio. These include both capital gains and any dividends received since I bought shares.

As you can see, I started out with somewhat even distribution of my cash over these top-25 positions. But over the years, some of these positions have handily beaten others in performance. These were all good businesses to begin with, but a few have gone on to become extraordinary. So today, relative weights in my portfolio have begun to show a roughly pareto distribution (aka the power law). Pareto distribution holds that 80% of a portfolio’s return can be traced to 20% of the investments. My portfolio is not quite there yet, but it shows early signs of it. Average size of the positions hasn’t changed much over the years (from 3.1% to 3.5%) but today individual holdings show significant dispersion from the average. Top 3 positions account for 30% of the portfolio whereas half of the positions are at or below 2% each.

If you are indeed a patient long-term investor, odds are that your portfolio does not hold stocks in equal proportions. This would be true whether you are picking individual stocks (like me) or passively investing in a very low-cost index fund (those that tend to be market-cap weighted). We all would have some positions that have done better than others. I don’t recommend that we rebalance our positions by periodically reducing highflyers and scooping up underperformed securities. [For index investors, this would amount to investing in an equal-weight fund/ETF instead of a traditional market-cap weighted index.] I only reduce a position if there is a fundamental reason for doing it unrelated to just the size of the stake. I might be increasing available cash, concerned about a recent change in the business, or unsure of new management. On occasions, I am forced to sell a position on account of a company going private (Brookfield Property REIT in 2021) or getting acquired by another (like Activision this month)

To see more of my thoughts on this topic and understand why I prefer to keep my winners, see these two blog posts: A coffee can approach to investing and Buy right sell never.

Leave a Reply