In June this year, the NBER (National Bureau of Economic Research) announced that U.S. had entered an economic recession beginning in February. This recession came after the longest economic expansion in the US history—from June 2009 through February 2020—of about 128 months in total. See the NBER announcement here. The NBER is de facto U.S. authority that marks beginnings and ends of recessions. That it took them four months to declare a recession after the fact happens to be par for the course. See my previous blog post on the NBER and recessions here.

Chris Davis is the well-known portfolio manager of Davis New York Venture Fund (NYVTX)—a fund that has been in operation since 1969. He is third-generation investment manager whose grandfather, Shelby Cullom Davis, was a also highly regarded investment advisor. I enjoy reading Chris Davis’s thoughtful commentaries on state of the markets even though I am not invested in any of the funds his firm manages. He is a patient long-term oriented value investor with very successful investing record. The NY Venture Fund has returned 11.22% since February 1969 versus 10.01% for the S&P 500. Davis Advisors is an employee-owned firm with over $2 Billion of its own money invested in the funds it manages. This level of skin-in-the-game makes Chris Davis’s market opinions even more credible to me.

Here is a good book to read on Davis Family’s investing career: The Davis Dynasty: Fifty Years of Successful Investing on Wall Street.

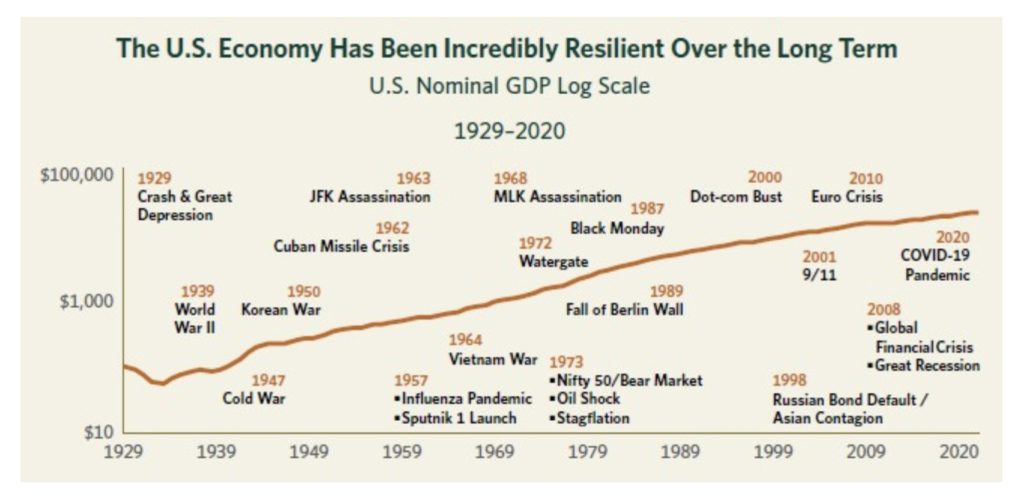

In April this year, Chris Davis had a wide-ranging conversation with Meb Faber. See Episode #221 of the podcast here. Chris talked about how the US economy has been incredibly resilient over the long term, and that this COVID-19 pandemic is another event on the long list of crises and corrections that have come to pass.

He said he buys stocks with expectation that he’ll hold them through a recession or two. In this recession, he mentioned in the podcast [at 00:33m], there are three categories of business that he looks at:

- One: Those that may not survive this recession due to high leverage, high fixed cost, or plummeting revenue. These are obvious ones to avoid.

- Two: Those that actually benefit from this environment, though their recent earning boosts might not last post pandemic. Examples would be video gaming, online retailers, social media, work-from-home businesses.

- Three: Those where we may not be able to estimate earnings for next one to four quarters today, but we still have enormous confidence in their resiliency to survive this downturn. These are most attractive to buy today.

As readers of this blog know, I also bought businesses during the peak of this market crash in February/March. See my post from March: Be greedy. Of those, how many do I think have strong chance to survive this recession? All of them.

While I don’t measure success in six months or one year, I showed in a blog post last month (Breaking out to a new high) how some of the businesses I bought are already thriving in this environment, and as a result being rewarded with high share prices. On the other hand, there are some that haven’t done so well. Two have cut dividends (Simon Property and Walt Disney) while several others have stopped share buybacks.

Many of these businesses have reported earnings declines. Some have reduced SG&A costs by laying off employees and cutting marketing budgets. Others are forced to shut down operations due to government mandated closures. Some of them are in industries that appear to be permanently (or perhaps for some significant time in future) impaired by the pandemic—such as travel and mall retail businesses. Most have also suspended revenue/earning guidance because of prevailing uncertainties.

Needless to say, I like to see any business I buy turn around quickly. But this doesn’t always happen. Some do really well but then there are others that the market continues to dislike for long time.

With this long prelude, below I share some additional information on each one of the businesses I had bought. I hope it sheds more light on why I believe in their long-term prospects.

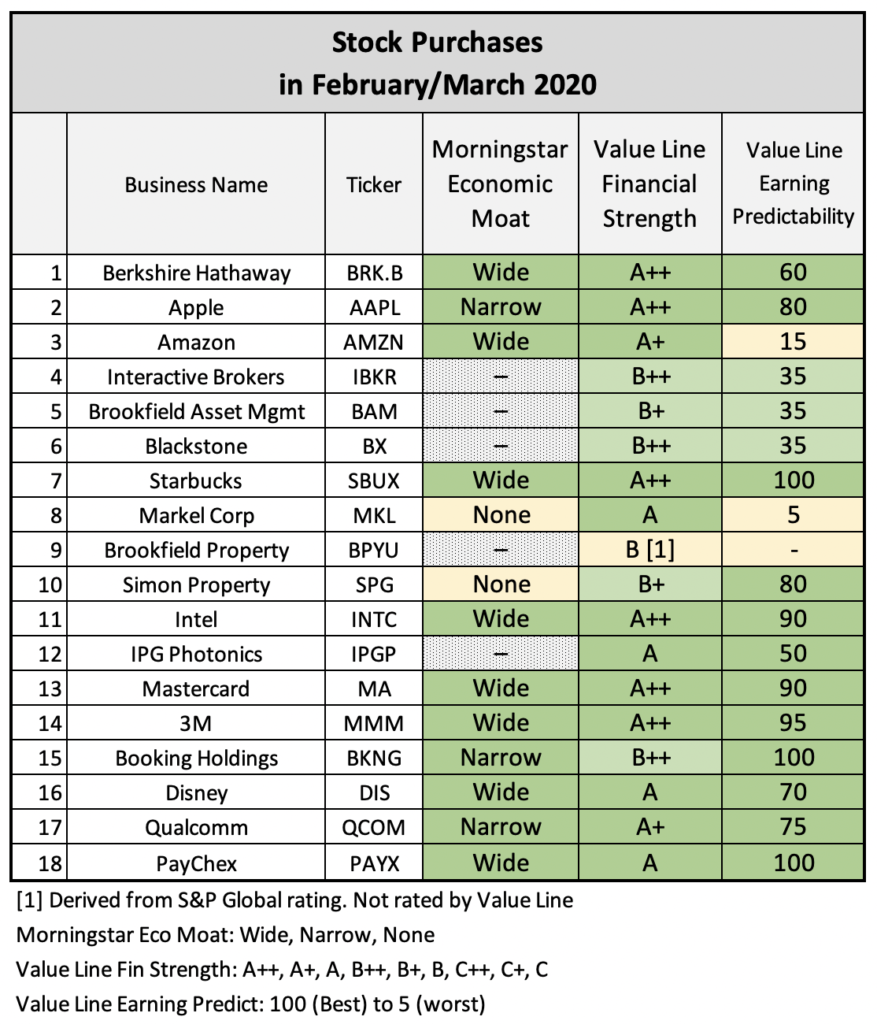

In the following table, I show Morningstar’s Economic Moat rating for each business. I also show Value Line’s Financial Strength and Earnings Predictability grades. Let’s first understand what each of these ratings mean.

Morningstar Economic Moat: It shows how durable a business is to withstand competitive threats. How long could it keep its earnings power? The deeper and wider the moat, the harder it is for competitors to surmount it. I did a blog post on economic moats—see this: What is an economic moat. Morningstar says this on a business’ economic moat:

A company whose competitive advantages we expect to last more than 20 years has a wide moat; one that can fend off their rivals for 10 years has a narrow moat; while a firm with either no advantage or one that we think will quickly dissipate has no moat. [Source]

Value Line Financial Strength: Value Line grades each company on nine-step scale that ranges from the strongest (A++) to the weakest (C). Financial strength of a business becomes even more important during a recession, as Value Line explains:

During a recession, cash flow falls, banks aren’t eager to lend, and pricing conditions are tougher when trying to sell shares or corporate debt. It’s during the hard times that a company’s financial strength shines through. [Source]

Value Line Earnings Predictability: This is Value Line’s judgment on how consistent and stable business earnings have been over the last eight years. It ranges from 100 (best) to 5 (worst). In my view, this is not nearly as relevant as the other two factors since (a) earnings (unlike cash flow) vary due to accounting related peculiarities and (b) some good companies (e.g. Amazon) have long capital investment cycles where earnings are unusually depressed for multiple years. Despite being of less value, I threw it in the mix to make a point (see further below).

You can see from the table that a lot of what I bought were businesses with either wide or narrow economic moat. If we go by Morningstar’s view, these businesses have competitive edge that could last for another 10 to 20 years.

Next, look at the financial strength ratings. Two third of these businesses are rated as high strength by Value Line (A++ to A). Others are also solid mid-range (B++ to B). None of them have low financial strength. I avoid business with weak financial structures.

And finally, the earnings predictability grades. Very few of them have below 50 ratings. Some that do are still outstanding businesses, notwithstanding their low ratings. For instance, Amazon and Markel are both great businesses but they are not managed for predictable and stable quarter-over-quarter earnings. And I am good with that because I understand their business models very well and consider their managements excellent capital allocators.

A final word: Looking at the big picture from the table, it appears obvious that some of the businesses are indeed strong and durable. They would easily survive this downturn, no matter how protracted it may be. These are the ones that aced their moat and financial strength ratings. Ergo, they were also my no-brainer purchases.

And then there are some others in the table that are either not covered by Morningstar or don’t have a moat. Many of these are also rated Average (B++ or lower) for financial strength by Value Line. Such as IBKR, BAM, BX, BPYU, and SPG. Do I still have faith in them? Are they resilient enough to survive this recession? Yes, and yes. Notwithstanding Morningstar and Value Line research, these are businesses that I have known for long. I have done my own due diligence on them. I have faith in strength of their business models and trust in their managers. I have also written about them several times in the past here—see below links. While they haven’t done as well in the market recovery since March, they will also endure and eventually do well for long-term investors.

See my previous notes on these businesses here: Berkshire, Apple, Amazon, Interactive Brokers, Brookfield, Blackstone, Starbucks, Markel, Brookfield Property, Simon, IPG Photonics, Disney

Leave a Reply