As the stock market rose to a new high this month, it was time to divest what I had invested during the brief April downturn. I raise cash when stocks are reaching new highs and invest in them when they go down (my dry powder investing). As I considered what to sell, I noticed that the cost bases of each of my top 15 positions (about 80% of my portfolio) were spread all over. Some of my holdings have gained 9x–13x since inception. Some others show more modest 2x–3x gains and the remaining fall somewhere in between.

Here’s a table of my top 15 holdings and their MOICs (Multiple on Invested Capital).

Note that MOICs in the table are relative to average cost bases of each position, and not just relative to first purchases. I’ve shared my multi-baggers in previous blog posts too. Those were meant to show how much my initial purchases had gone up. I tend to gradually raise my stakes over time in good businesses even as their stocks rise; hence lower average MOICs in this table.

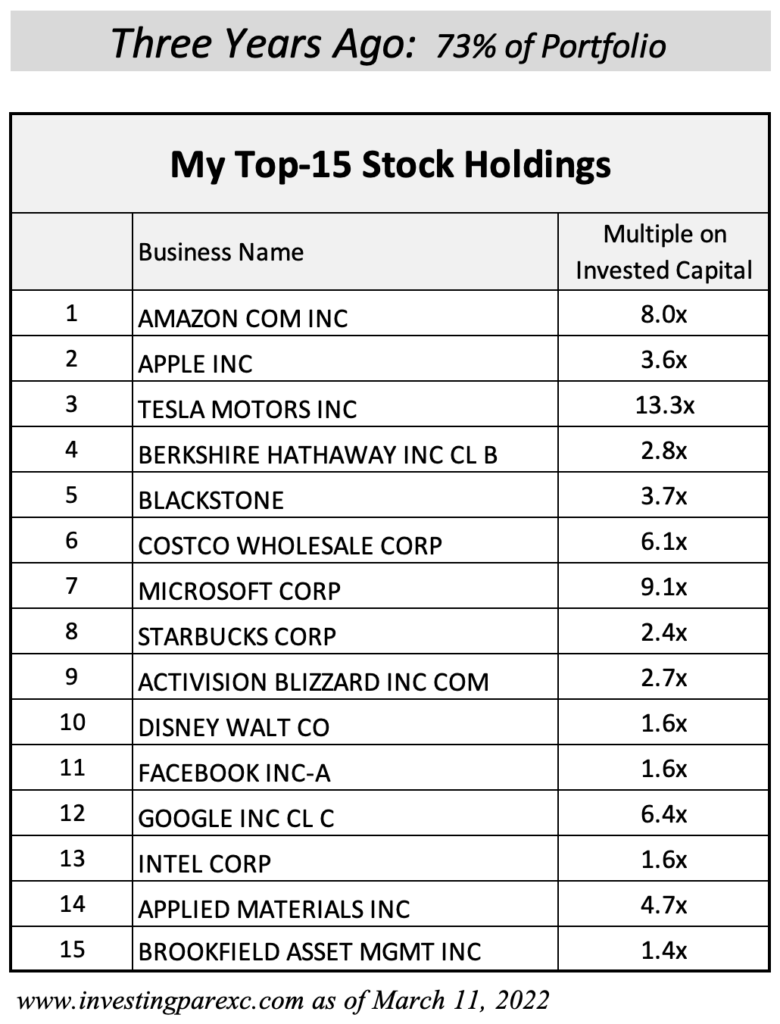

I shared similar table (reprinted below) three years ago in a blog post. Since then, most of my top 15 names have stayed unchanged. Intuitive Surgical (ISRG) and Interactive Brokers (IBKR) are new top stocks while Activision (ATVI) and Intel (INTC) have fallen off the list. Since March 2022, my portfolio (and the market) has risen about 50%. Today my portfolio is more concentrated with top 15 making up 81% of stock holdings versus 73% three years ago.

Do I sell only from those positions that have small cost bases i.e. my top multi-baggers? For instance, Costco where my cost basis is just 7% of the current value. Or Microsoft where my basis is about 10%.

Or do I just trim my top 3 holdings that have made my portfolio quite top-heavy? Top three holdings are about 1/3rd of my portfolio today. Or perhaps I just get rid of my performance laggards?

This made me think about how investors tend to look at their invested capital versus capital gains. Short-term investors always seem obsessed with their cost basis and where it stands relative to any unrealized gains. Profit taking is often top of their minds.

Take for instance the so-called house money effect. Once an investor has doubled his money, he is prone to take one-half of it (i.e. initial investment) out. And free riding the rest. They treat their profits as “house money” that is less valuable and more expendable.

This is like to going to Vegas for gambling with $1000 in pocket. If I do well, I will recoup my one grand early. And for the rest of the stay, I will just be playing with house money, knowing I won’t return home empty-handed. I could afford to take more risk with this money!

Another sign of short-termism is the breakeven effect. Or what Ken Fisher, the founder of Fisher Investments, calls breakevenitus. It is the urge to sell investments as soon as they’ve recovered from a loss and returned to their original value. If I can just get back to even, I’ll sell and not have to worry anymore.

By doing so, we anchor ourselves to the original cost basis. The primary emotional driver becomes the desire to “get out whole” and avoid the pain of another downturn.

Both the house money and the breakeven effects are pervasive among novice investors. The common thread between the two is the original cost basis. If we could just learn to ignore the cost bases and focus on future potential of each holding, we’ll do much better.

Our undue focus on cost basis also leads us to some interesting measures. One is the spiffy-pop moment, a term coined by David Gardner of the Motley Fool. It happens when a stock pops up in one day by more than its original purchase price. A single-day gain that is greater than our original cost basis. To be clear, David does not advocate we sell when a spiffy-pop moment occurs. He calls it a celebratory event, rather than a signal to sell and lock in the profits.

Another is a performance metric tied to original cost basis, the Yield on Cost or YOC. It is a measure of how much annual dividend is being distributed today by a stock relative to our original cost basis. I have shared yields-on-cost on my long-term holdings in previous blog posts (see here and here). Seeing my YOC grow from 2% to 10%–15% over time is a strong positive reinforcement for my long-term buy-and-hold strategy. The downside is that it is irrelevant for future buy/sell decisions. For those, we must focus on current yield and current share price, not what we had paid for them.

Do we long-term investors care about our cost bases? We do, but only for measuring portfolio performance or when planning for taxes. In most of our investing decisions, cost bases should not factor at all.

My cost basis is a historical data point that has zero influence on the company’s future earnings, competitive position, or stock price. Novice investors tend to focus on the past. Experienced investors must be look at each stock’s future potential.

The market does not know or care what my cost basis is in each stock I hold.

We tend to separate our money into different money buckets, based on its source. Money earned from a salary is often treated with more caution, while a surprise bonus or a lottery win is placed in a windfall account. In the same vein, money we used to buy stocks is treated differently than any subsequent gains those stocks made. But a dollar is a dollar. Every dollar, regardless of its origin, has the same purchasing power. We investors must treat all our capital as a single fungible pool of resources.

Circling back to my portfolio, I ended up selling about 1% each of my top 15 holdings this time. It amounted to about 37% of dry powder cash that I’d invested in April. Those April investments show about 42% gain today, down slightly from 45% that I reported in July. I expect I’ll be able to convert the remaining two third of my dry powder investments into cash in a few months, if the market continues to make new highs.

Leave a Reply