According to a recent WSJ article, eighty-three U.S. public companies have either canceled or suspended dividend payments so far this year. And another 142 companies have reduced their dividends. The journal went on to predict about 10% decrease in dividend payouts overall this year.

Considering such dire prospects for dividend payers, how are my positions holding up?

As regular readers of this blog would know, I don’t invest exclusively in dividend stocks. In fact, many of my large positions are in companies that do not pay dividends at all. They tend to be high growth younger companies that reinvest profits for further growth. [I wrote another blog post on my reinvesters, dividend payers, and share repurchasers.] But at the same time, I also invest in durable dominant businesses that generate excess cash flow and return some of it in form of dividends. In this post, I will focus on just those dividend generating stocks.

Q1 earnings reporting season is almost over. Nearly all my portfolio positions have already reported. Along with the earnings, most dividend payers have also announced quarterly dividend payments.

There were a few surprises, but by and large majority of the companies stuck with their dividend payouts. Some even increased payments, bucking the trend. But there were indeed a handful of businesses that decided to suspend or cancel dividends entirely.

So, here’s how my dividend payers have fared so far. I broke them into three buckets: Those that continued paying dividends unchanged, the ones who bucked the trend and increased dividends, and finally the few who have suspended or delayed payments. Below tables cover all dividend actions taken by these stocks since February this year.

First bucket: I own shares in many different public companies in various industries. But many of these positions are relatively small (less than 5% each of my portfolio). There are only a few companies where I have outsized positions. For instance, my top 10 positions make up over 55% of my portfolio. See this blog post (My Portfolio is Getting Top Heavy) for background.

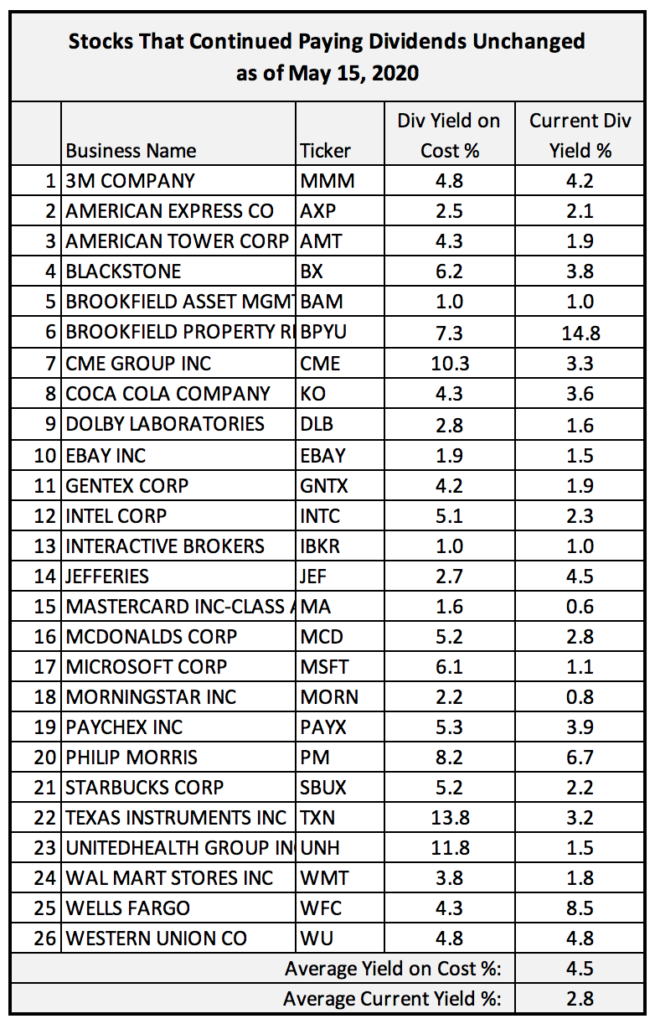

The table below shows all my dividend paying stocks (large or small) that have announced a quarterly dividend that is unchanged from before.

This is by far the biggest category—a total of 26 stocks. They all continued paying dividends as usual, even in these unusual times. This reflects on durability of these businesses. They are best equipped to handle temporary economic dislocations. They have balance sheet strengths, pricing power, and dominant market positions to endure through these times. It does not mean though that they are fully immune to long-term economic malaise. No company is. So we can’t completely rule out the possibility of future dividend cuts/suspensions if lockdowns persist and the economy continues suffering. But the possibility that all of them would suspend dividends is indeed remote.

At the same time, I believe many of these companies would have actually raised dividends even in today’s economy if a raise were due. Most of them tend to announce a dividend raise once a year on a set schedule. If that announcement weren’t due in the first quarter, they’d kept the dividend unchanged.

It is worth pointing out that from the above list, two companies, Blackstone and CME Group, have somewhat unusual dividend policies. Blackstone does not have a fixed dividend payout. It pays 85% of its free cash flow and because of the nature of its business, the actual dollar amount varies from quarter to quarter. CME Group pays two different dividends: A fixed dividend allocation paid every quarter and a variable special dividend that is paid once a year.

For Blackstone, I have assumed that current dividend rate would be maintained going forward. For CME Group, I’ve taken a three-year average of past special dividends and added them to its regular dividend.

My dividend yield on cost for these stocks is about 4.5% (weighted average based on individual position size) and current yield is ~2.8%. Both are above the current S&P 500 dividend yield of 2.05%.

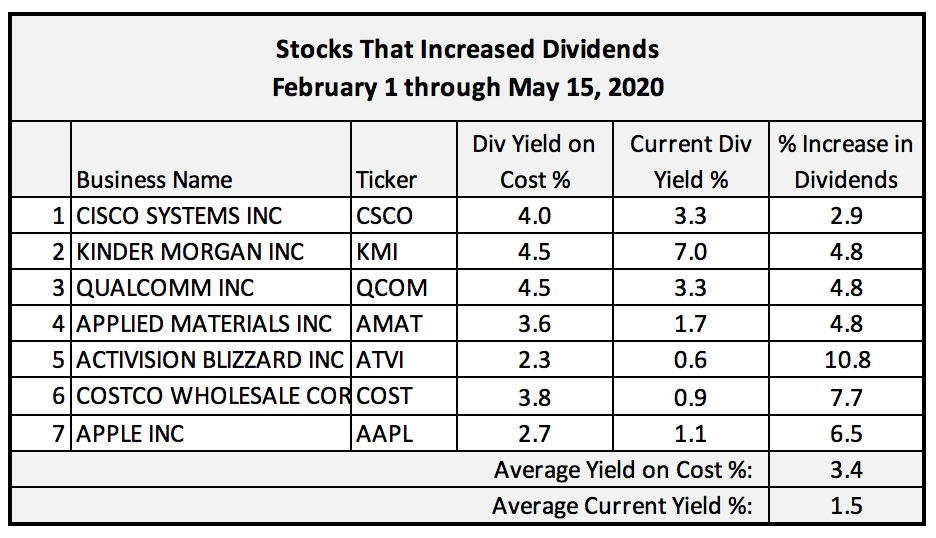

Second bucket: This next group of stocks are those that bucked the general trend and announced raising of their quarterly dividend/share since February. Naturally, it’s smaller bucket—just seven stocks in total. After all, not every business can afford to increase dividends in today’s markets. But nevertheless, these seven did.

These seven names are veritable dominant players in their industries. Four of them are in technology (Apple, Qualcomm, Applied Materials, Cisco), one well-known retailer (Costco), a video-game industry veteran (Activision), and an oil-gas midstream pipeline operator (Kinder Morgan). The dividend increases range from about 3% for Cisco to nearly 11% for Activision.

The market has also rewarded these stocks. Three of them are near their all-time highs (Apple, Costco, Activision). Unsurprisingly, my current yield on this group is only about 1.5%.

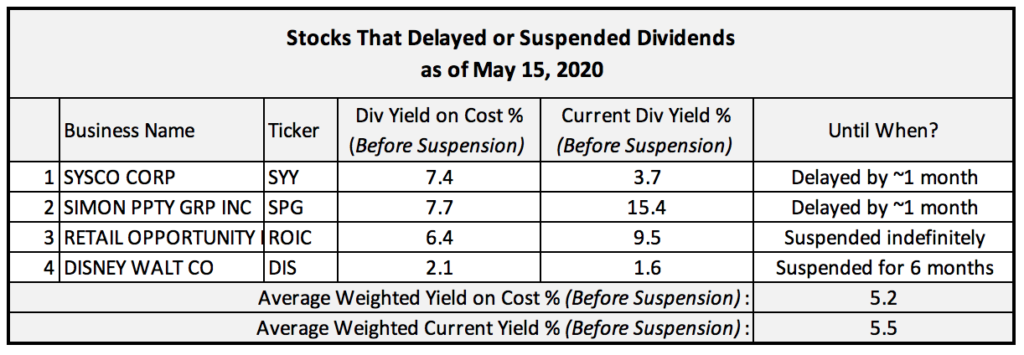

Third bucket: And finally, the dreaded third category belongs to those who had either suspended or delayed dividend payments recently. It’s a small list fortunately. Just four stocks. Let’s review each case.

Sysco is #1 in food distribution business with restaurants as one key client group. It hasn’t stopped paying dividend—just that it’s delayed for this quarter. I believe it could cut its dividend by half for the rest of this year.

Simon Property is the #1 mall landlord in the U.S. It has also just delayed announcing the dividend. Even though the times are tough for this REIT business, the CEO has been explicit in stating its intention to continue paying dividends. It has the financial strength to survive in today’s conditions. Though for now, it could also cut its dividend by half to improve cash flow.

Retail Opportunity is also a REIT focused on grocery anchored shopping centers on the west coast. It’s a much smaller business than the other three. It has suspended dividends indefinitely. I don’t expect it to resume paying until perhaps the fourth quarter this year. I am not bailing out though because I believe it can also endure through this period.

The last one on this list is the venerable Walt Disney Company. Disney only pays dividends twice each year. That it suspended dividend payment for the second half of 2020 came as a surprise. It undoubtedly has the financial wherewithal to pay its dividend. It continues generating healthy free cash flow (though down 30% QoQ in Q1) despite significant business interruption. A Morningstar analyst recently wrote that Disney’s dividend suspension is not because of any financial constraints, but mostly for good optics. It has furloughed nearly 100,000 theme-park and hotel workers back in April. It just wouldn’t have looked good if it had continued paying dividends. I am a believer in this business. No doubt they will recover and will eventually resume dividends too. I expect this suspension to only last six months.

The overall effect of these dividend suspensions is noticeable but not significant to my portfolio’s yield. If these four companies cut their dividend by 50% for one year, my effective dividend yield (for the entire dividend paying portfolio) would drop from 2.6% to about 2.4%. So long as my other dividend payers continue paying.

I don’t lose sleep over temporary dividend cuts. I am still a believer in all these businesses. Over time I expect them to restore dividends fully and start growing them once again. In the meantime, I am still getting paid for owning shares—albeit at a slightly lower rate.

Warren Buffet has said once: “You only find out who is swimming naked when the tide goes out”. Well, it has been a low-tide period in the stock market lately. But for my dividend paying portfolio, it is so far so good.

I own JP Morgan. It’s dividend yield today is around 3.8% which looks pretty good to me. Do you think it’s safe? I am bailing out but I do wonder if I can count on it paying dividends in future.

I like safe dividend paying stocks in general.

Hi MKwi: I don’t own any major banks except Wells Fargo (WFC) as you can see from the tables above. WFC dividend yield is even more appealing than JPM (~8%) but I believe it reflects the uncertainty surrounding future payments. I don’t have a strong view if major US banks will be able to continue paying at today’s rate. As with many other things in investing, it will depend on how the economy would do in the next 12 months.

Most European banks have suspended dividends. US banks have suspended share repurchases, but not dividends. At this time, US banks are quite profitable and loan loss reserves are not too high either. Would their regulators force them to cut/stop dividends? May be. If that were to happen though, I suspect that the additional retained earnings will result in higher dividend payouts down the road. I am holding on to my Wells shares. No reason to sell when share price is so low.

Here’s another view from Barron’s on this: https://www.barrons.com/articles/bank-dividend-questions-wont-go-away-heres-why-51590065558

Your div yield of 2.6% is good, but not great. There are many good stocks out there that today yield more than 3%. I own JPM and CSCO, they both yield >3% today. Also have Altria yield is >8%.

Hi JorgeCh, good for you. One thing I’d point out about my portfolio is that while it’s current yield is ~2.4% (down from 2.6% due to dividend cuts), the dividend yield-on-cost-basis is ~4.5% today. This is substantially higher than today’s average market yield. You can see the yield on cost for each bucket in the tables.

As soon as the market recognizes that a div raise is here to stay, it reprices the share price. So while current yield is a fine parameter to compare against a market yield, what I really measure is yield on my original cost basis. When I bought these stocks, they weren’t yielding 4%. But with dividend increases over time, I got to where I am. So today, I am getting 4.5% yearly income and also sitting on significant capital gains as evident from the difference between current and on-cost yields.

Thanks for sharing your thoughts!