Today’s post is about a business I own since 2015 but I hadn’t bought any new shares in last three years. It’s a business that I am very familiar with. I am not only a shareholder but also a long-time customer. I use its tools and services extensively in my investing work.

I am talking about Interactive Brokers (IBKR). It’s quite possible that you may have never heard of it. Even though IBKR is the world’s leading discount broker in terms of trading volume.

I first bought IBKR shares after I had started using its trading platform. I hadn’t bought any more since then. In the last two months though, I have added to my original position. What made me interested in IBKR this time around? One, its stock price has gone down substantially since 2018.

Even more importantly though, I became intrigued when someone recently pointed out to me that IBKR’s pretax profit margin far exceeds anyone in the industry. This is not common and given that IBKR is not the dominant player in the broker-dealer business, it’s even more unusual. This got me looking at the business in more depth.

IBKR is the #1 broker in the world if we consider number of trades executed every year on its platform. However, it is a much smaller player among the brokers in conventional financial terms, such as annual revenue, number of clients, total client equity, or even number of employees. Its size pales in comparison to the two big dogs in the brokerage world, namely Charles Schwab (SCHW) and Fidelity. In fact, IBKR is smaller than the top three public brokerages: Schwab, Ameritrade, and E*TRADE. (Fidelity is a private company, so we don’t know its numbers.)

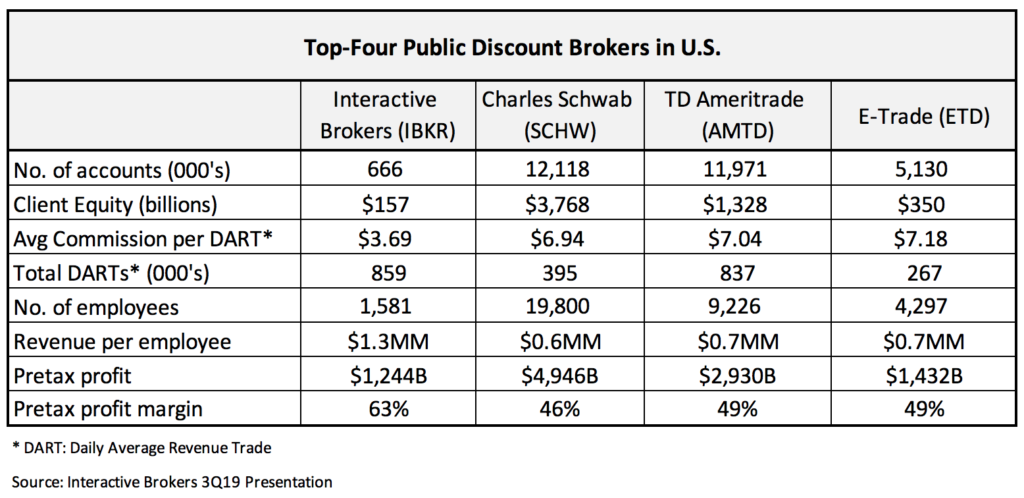

Take a look at IBKR numbers in comparison with the other three public brokers in the table below:

Compared to Schwab, IBKR has 20x fewer customer accounts and client equity, and yet it handles more than 2x trades every day. TD Ameritrade (AMTD), which caters to more active traders than Schwab, does not come close either. It also has 20x more accounts than IBKR but handles 15x less trades per account. Key takeaway is that IBKR has successfully attracted active traders to its platforms while other discount brokers mostly cater to infrequent investors. These frequent traders are sophisticated individual investors (I count myself in this group), hedge funds, proprietary traders, financial advisors, and introducing brokers. As a group, these clients like what IBKR platform offers to them: a sophisticated flexible platform, lowest cost of operation, and access to world-wide financial markets from a single account.

Now consider the number of employees each of these big brokers have. Schwab has 19,800 employees, Ameritrade at roughly half the number, and IBKR has just 1,581 employees. To paraphrase IBKR CEO’s words, they execute and clear roughly 859,000 trades in 24 currencies across multiple classes of exchange listed products in 29 countries every day with just a little over 1500 employees. How they do it? Through automation of all their processes and services. Unlike its competitors who employ hordes of salespeople and customer service agents, IBKR has a tiny army of software developers. It automates most of the work with internally developed software.

In fact, I consider IBKR to be a software-as-a-service (SaaS) company, rather than a traditional broker-dealer. And it shows up in its profit margins too. Going back to the previous table, see the revenue-per-employee number and its pretax profit margin.

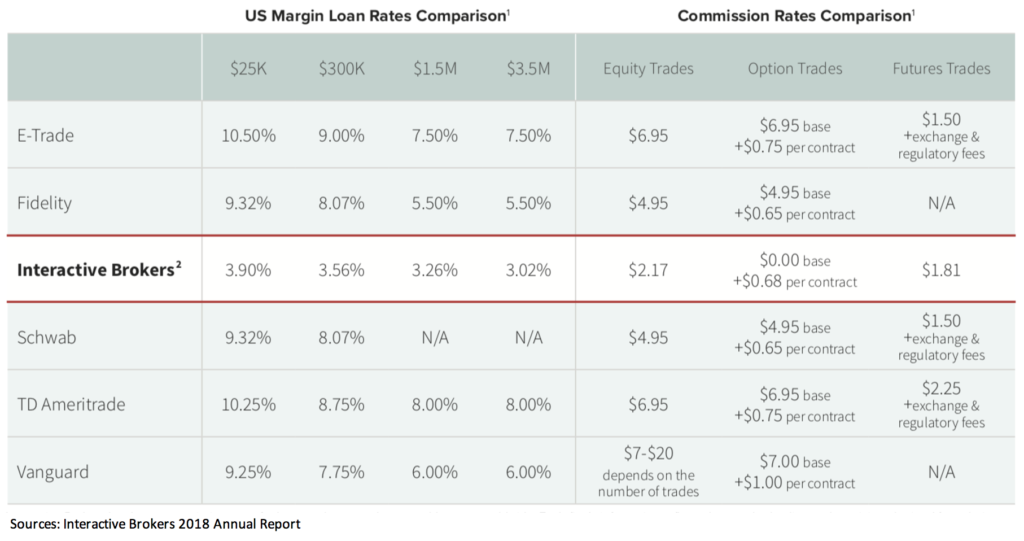

High-quality enterprise: It is this 60+% consistent profit margin that renewed my interest in IBKR. No broker in the world comes close to their level of profitability. None. And this feat is even more remarkable when we look at how much IBKR charges for its services. It offers the best rates on cash balances, margin loans, and trade commissions across the industry. On margin loans, IBKR rates are less than half of any other brokerage. On idle cash, its rates are highest and tied to the benchmark Fed Funds rate. Commissions were also the lowest in the industry before the recent adoption of industry wide zero commissions. See this table.

This combination of industry-high profit margin and lowest service fees is what sets IBKR apart from competition. It is consistently recognized as the best online broker. Key to its business model is the custom software that was built over 40+ years of market making and trading activities. Management often boasts that its top executives all came from software development background—not finance. Founder Thomas Peterffy himself is a software pioneer.

This ability to develop software for a complex worldwide trading platform is what I believe other brokerages are unable to match. And in turn, they all lag IBKR in terms of offering best services at lowest cost with minimum employee overhead. From the first table, you can see that IBKR’s average revenue per employee is two times higher even though it is a much smaller scale operation (in terms of # of clients).

So I believe that because of its unique business model, IBKR will retain its profit margin edge in the industry. I don’t believe competition could offer similarly priced services in foreseeable future. IBKR has been growing faster than the industry too. Granted it is off a much smaller base than its larger peers, IBKR has been able to successfully attract sophisticated clients to its platform over the years. It has grown at an annualized rate of 20% (client accounts) and 23% (client equity) in last five years.

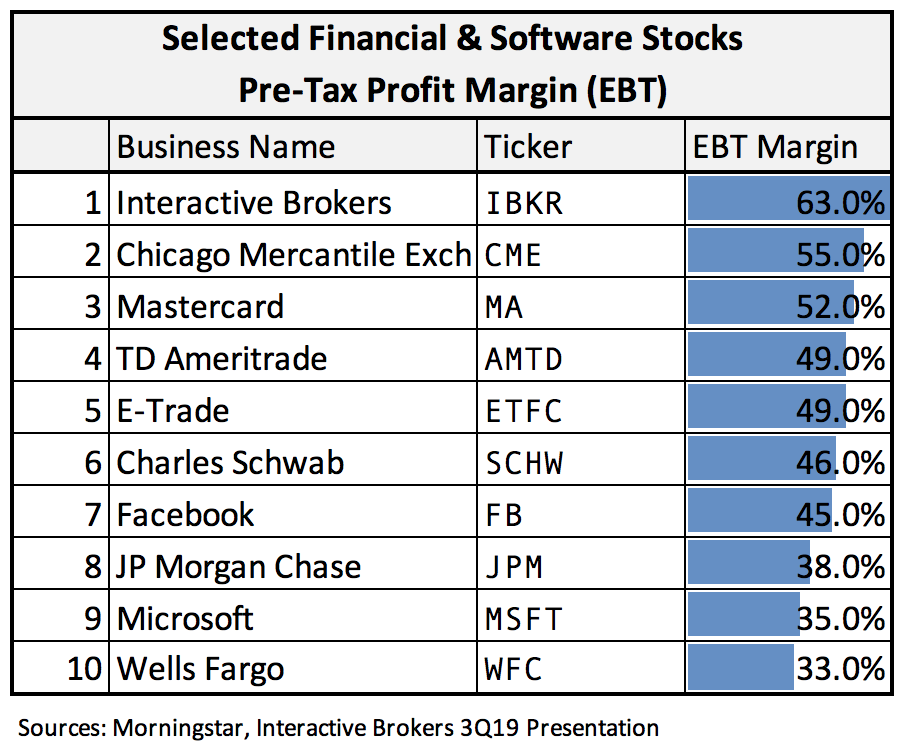

Consistent higher-than-peers profit margins are signs of a durable high-quality business. Brokerages are generally very profitable with average EBT (earnings before tax) margins in 40% – 45% range. This is higher than most large U.S. banks, for instance, where EBT margins are often 30% or lower. I attribute IBKR’s eye-popping pretax margin of 60%+ to it being a “software-like” asset-light business model. I own several such high-margin businesses in my portfolio, such as Facebook (FB), Microsoft (MSFT), Mastercard (MA), and Chicago Mercantile Exchange (CME). Even among these high-margin companies, IBKR stands out as the highest margin business. Look at the table below.

Management? Now that we’ve established that this is a high-quality durable business, let’s consider the people running it. IBKR started out some 40 years ago as a market-maker. Today, it is focused on the brokerage business. Its founder CEO is Thomas Peterffy who’s still at the helm, albeit as its chairman. He is in his 70s and has just handed over the CEO role to his long-time associate Milan Galik. Peterffy built this business from scratch and hadn’t needed any venture capital to support its growth. As a result, he still owns greater than 80% of the company. We, the public shareholders, own the rest 20%. Peterffy’s salary is fixed at a very modest $800K annual. No stock awards, no cash bonuses. His only other compensation is the modest dividend that IBKR pays out every quarter (about 0.7% per annum today). This is a “controlled company” where public shareholders have minimal influence. But that is fine with me. With an owner-founder at the helm whose legacy, reputation, and net worth are all tied to the business, I am comfortable that my capital is in good hands.

Peterffy’s capital allocation has been excellent so far. As I mentioned before, he has grown this business from scratch with internally generated cash flow. The company has no debt. It pays a modest dividend and retains majority of profits to support growth. To date, no major acquisitions either.

Why is IBKR down 40%? It’s a mid-cap stock with tiny float so I expect it to be volatile. There are two main reasons why it’s down so much since 2018. One, interest rates going down has put pressure on its net interest margin. This is an industry wide problem, not specific to IBKR. Two, Chinese government has recently started restricting its citizens from investing in foreign capital markets. As a result, IBKR international growth has slowed down. Neither issue is a long-term concern, as far as I am concerned.

Reasonable valuation: On the other hand, this drop in share price has made IBKR more appealing for new purchases. At $46 per share (that’s what I paid in October), it is trading at 22x last year’s earnings. If I ignore the one-time trading loss it incurred this year, its P/E ratio is about 20x. This is reasonable valuation given the business quality and future growth prospects.

IBKR also carries excess capital of $5.5B (beyond what’s required by regulators) on its balance sheet. Management has said it is retaining this capital to attract bigger clients. But if we take this out from its market cap (it’s not needed to run existing operation), effective P/E drops to about 15x.

Broker Price Wars: The latest shakeup in the brokerage industry was also instigated by IBKR when it announced in September a zero-commission service tier, a la Robinhood. Note that IBKR’s commission rates were already less than half what all other big brokers charged. See the previous table. Less than a week after the IBKR announcement, Schwab declared it is going zero-commission across the board. Fidelity, Ameritrade and E-Trade followed soon after. While Schwab (and Fidelity) can easily afford the resulting revenue cut, Ameritrade and E-Trade will take significant revenue hit from this move. Since then, Schwab has agreed to acquire Ameritrade.

Can IBKR thrive? So the industry is consolidating. Revenue streams from trade commissions are disappearing. If Schwab-Ameritrade merger is approved by regulators, there will be only four major discount brokers left in the country. Peterffy said recently that his company is not interested in acquiring E-Trade. It is not interested in E-Trade’s labor-intensive account acquisition/support strategy. Or for that matter, any other discount brokerage. I believe IBKR can continue to do well by remaining independent. It won’t be easy for Schwab-Ameritrade to combine their trading platform. (Schwab management suggested a 3-year timeline.) Meanwhile IBKR has opportunity to lure Ameritrade clients with its low-margin, best-execution service.

Smaller-scale brokers like E-Trade will be under serious cost constraints. Here, IBKR has another opportunity. It offers its technology to other brokers as a low-cost service. E-Trade could adopt IBKR’s trading platform and ditch its own to reduce expenses. Scottrade did this in 2014, before it was acquired by Ameritrade. One of China’s largest international broker, Tiger Brokers, also uses IBKR’s technology platform.

Zero commissions are not what they appear to be. While this is a broad topic and I could write a whole blog post on it, suffice it to say that brokers have other ways to earn profits when they offer commission free trades. For big brokers like Schwab and Fidelity, commissions have only been a small share of overall profits. They make more money from banking services, self-managed investment products, and margin loans. Small brokers like Robinhood make money by selling their order flow to high-frequency traders (HFT). With its newly introduced zero-commission tier, IBKR will also start selling clients’ order flow to HFTs.

As I pointed out earlier, I use IBKR trading platform extensively. I am also a client of Fidelity and Schwab. But most of my complex investments (like defined-outcome investments that involve multiple stock options) are executed on the IBKR account. It has the best execution and provides most flexibility in terms of access to various financial instruments around the world.

No plans to exit. Like my other long-term investments, I hold IBKR shares with no particular exit strategy in mind. I don’t have a target price or expected total return at which I will sell my position. I believe that IBKR is an excellent business with some distinct advantages over its competitors even though it is a relatively small player in the industry. With an owner-founder running the business, I like its long-term prospects. I would continue to hold my shares as long as the business prospects look good, notwithstanding near-term hiccups if any. I am attracted to the businesses that are driven by founders who have significant skin in the game. Besides IBKR, I own several other such companies like Berkshire, Amazon, and Blackstone.

Leave a Reply