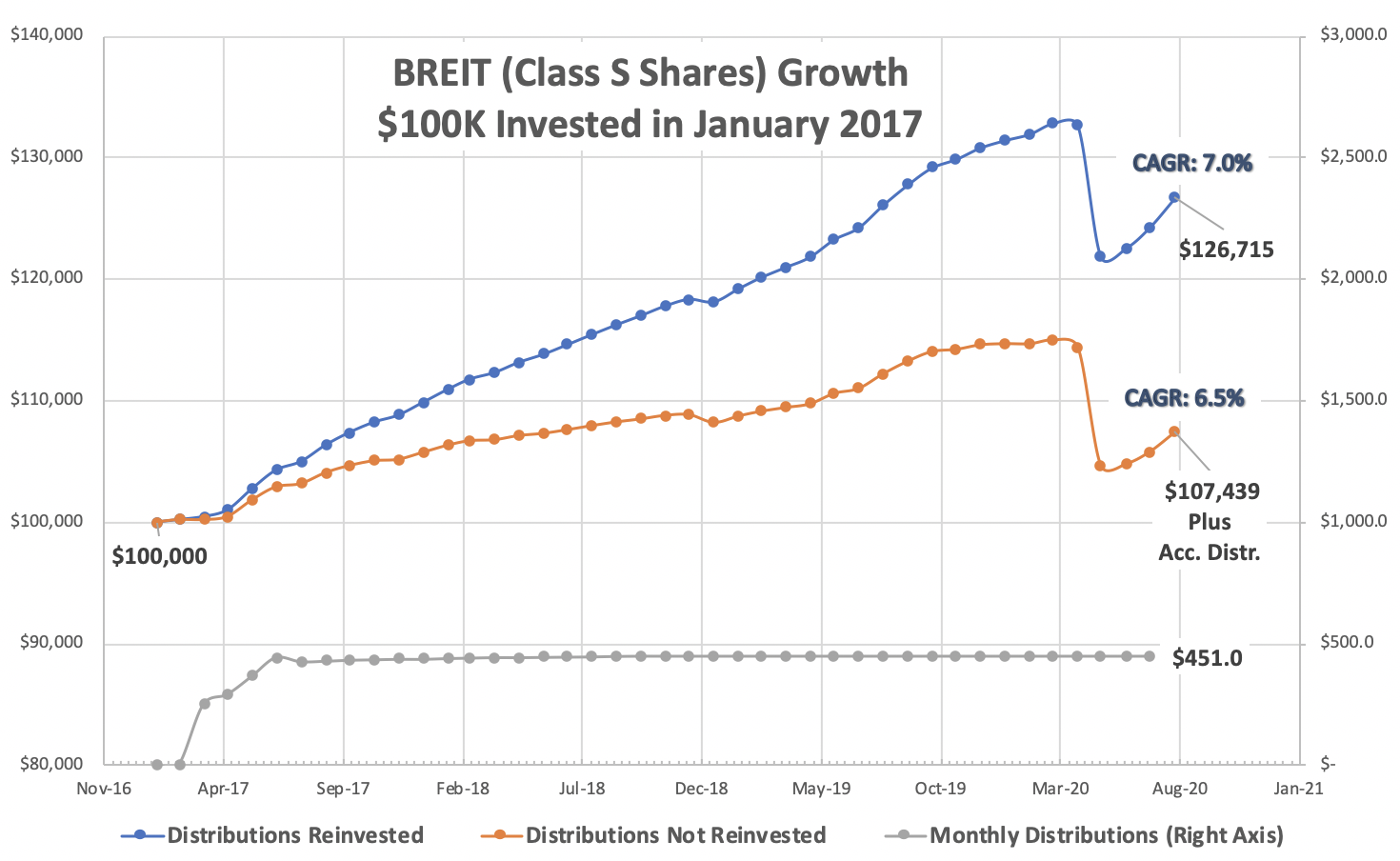

One of my popular posts over the last couple of years was on Blackstone’s non-traded commercial REIT called BREIT. I wrote about it a couple of times here. My last post on it was in August 2020.

Back in 2018 when I first wrote about BREIT, it was a new up-and-coming REIT. For the reasons spelled out in that post, I chose not to invest in it at the time. Two years later in 2020, I reviewed its 3-year performance. Since then, it’s been quite a roller coaster for the BREIT. 2H20 through 2021, BREIT was on a roll, growing tremendously with huge cash inflows – mainly from private wealth channels.

{kind=link}

Last year though was a very different story. As Fed’s interest rate regime changed, BREIT saw significant redemptions and cash outflows. Net cash outflow started in Q2 last year and gained momentum in the second half. Q1 and Q2 this year have also seen similar share redemption rates. In fact, the pace of redemption requests has been so high since the middle of 2022 that BREIT has started limiting them. BREIT has monthly and quarterly withdrawal limits of 2% and 5% as outlined in its prospectus. Also, investors who try to redeem shares within 12 months see a 2% haircut on repurchase price.

Why sell now? The larger question looming in the face of these withdrawals is why! Why are BREIT investors trying to redeem their shares en masse? It is a bit confounding to me. My understanding is that majority of BREIT investors are private wealthy individuals, most of them are likely have an advisor managed investment account.

This was in fact one reason why I chose not to invest in BREIT in the first place. As I explained in my 2018 blog post, I didn’t have an advisor managed account, nor did I wish to pay an advisor to manage my investments. And thus I wasn’t an investor that BREIT was targeting.

Majority of BREIT inflow since inception has come from private wealth channels. Why wealthy investors (and their professional advisors) want to get out of a good performing REIT asset? BREIT is meant to be a long-term holding. Its shares are not traded in the stock market, redemptions are limited and difficult, and investors are hit by a tax penalty whenever they redeem.

Taxes are usually an important factor for wealthy individual investors. One little known aspect of BREIT dividend is that most of it qualifies as return-of-capital, meaning we don’t pay any tax on those checks. Instead, those payments simply reduce our cost basis. In other words, dividend payments become tax deferred until an investor sells his BREIT shares. Per company filings, BREIT’s return of capital in 2019, 2020, 2021 and 2022 was 90%, 100%, 92% and 94%, respectively. In effect, investors have only been paying tax on less than 10% of BREIT distributions over the previous four years. The rest has been piling up as deferred capital gains. It’s one more reason why redeeming BREIT shares can be a bad move for those who have been in it for few years.

Today BREIT pays dividend at about 4.6% pre-tax. REIT dividends are generally considered ordinary income and are taxed the same way. For investors who are in higher tax brackets, they could be paying 24% to 37% of the payouts in federal taxes were it not for high depreciation costs of BREIT’s relatively young real-estate portfolio (which allows for accounting its cash flow as return of capital). Over time this tax preferential treatment of income will fade but I see BREIT continue to do mostly tax-deferred dividends in the next few years. In my view this is a compelling enough reason for existing investors to stay invested and ride out the current real-estate downturn. BREIT is a well-managed business with Blackstone as its corporate sponsor.

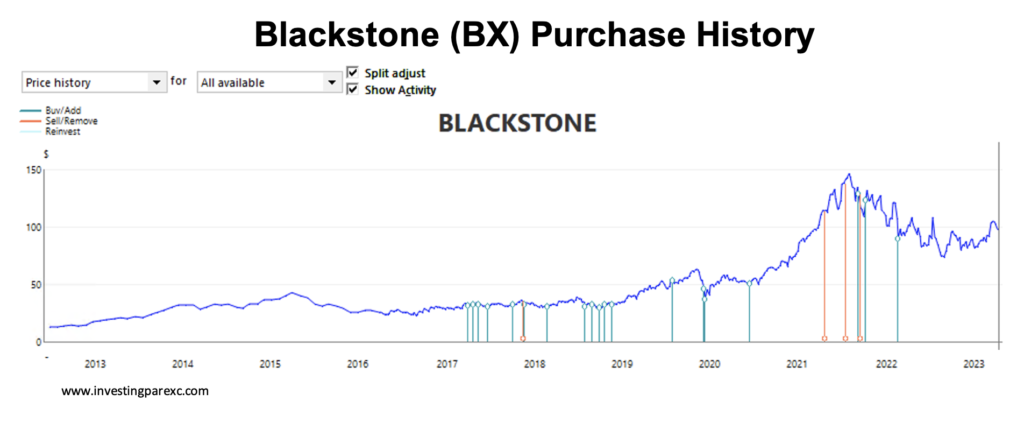

As for me, I am not invested in BREIT as I previously noted. But I am a happy shareholder in its parent manager, Blackstone (BX). See this note I wrote in 2019 about my Blackstone investment. Today, Blackstone is among my top-five stock positions. Since 2017 when I first started buying its shares, the company has paid me dividends equivalent to 40% of my invested capital. Current yield is 3.5%. My stake has grown by 2.2x (multiple on invested capital) not including dividends. See this chart.

The way I see it, both Blackstone and BREIT are good businesses to stay invested in. They cater to two different investor types. Blackstone is for more risk-tolerant investors who prefer higher growth. BREIT is for risk-averse real-estate investors who prefer steady monthly distributions and somewhat steady share price.

If BREIT were a publicly traded REIT, it very likely would have been a part of portfolio. But as of now, I only own Blackstone, its parent manager.

Leave a Reply