Last week I read Davis New York Venture fund’s annual letter. Its eponymous portfolio manager Chris Davis writes thoughtful analyses of investing landscape every year. I enjoy reading his investor letters even though I have not (yet) invested any money in his Davis funds family. Chris Davis comes from a well-known investor/asset-manager family. Davis NY Venture is its flagship fund, and it was started by Chris’ father Shelby M. C. Davis in 1969. I did a short profile of Chris Davis in August 2020 here.

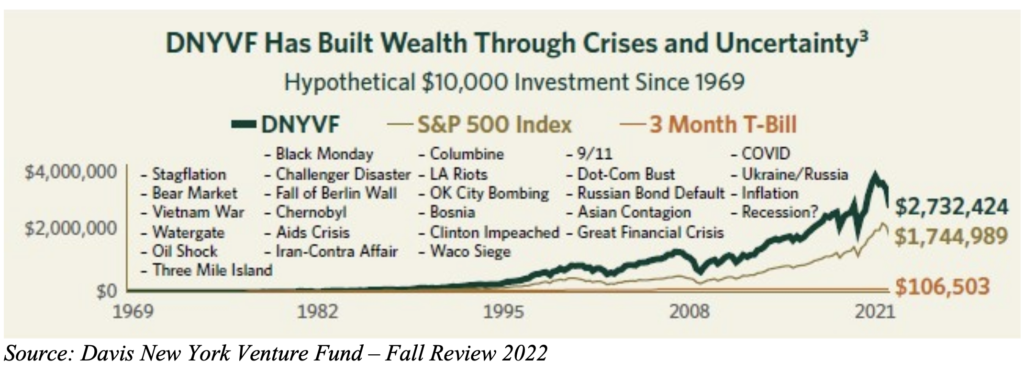

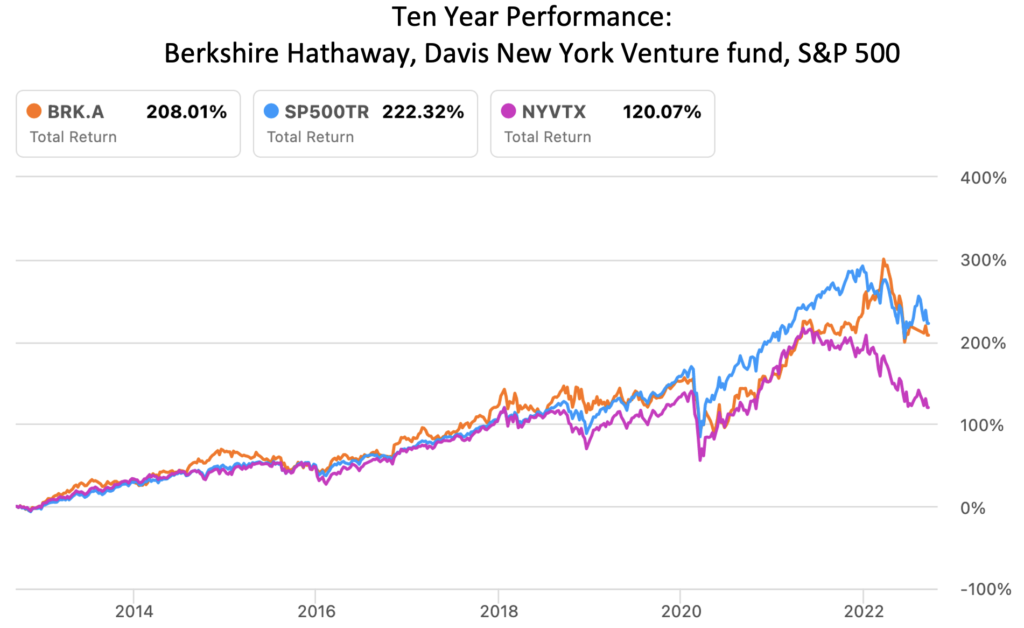

Davis NY Venture fund has not been a standout with respect to its recent performance. It has failed to beat the market in the most recent ten-year period. Longer term though, since its inception in 1969, the fund has handily beaten the S&P 500, as seen in below graphic.

There was more than one reason for the fund’s recent underperformance. But a main factor has been the relative popularity of high-growth high-valuation stocks over the past decade. At the expense of so-called value stocks. Chris Davis wrote about this in detail in his 2021 annual update. There have been other minor factors too. Such as higher concentration of financial stocks in the fund (relative to the S&P 500 index). And some ill-timed investments in China like New Oriental Education (EDU). But by and large, it was growth outpacing value stocks that led to its underperformance. Davis NY is focused on durable businesses that are selling at a discount to their true values. This is a trait it shares with several other value-focused funds and certain value-oriented capital allocators, as we will see later in this post.

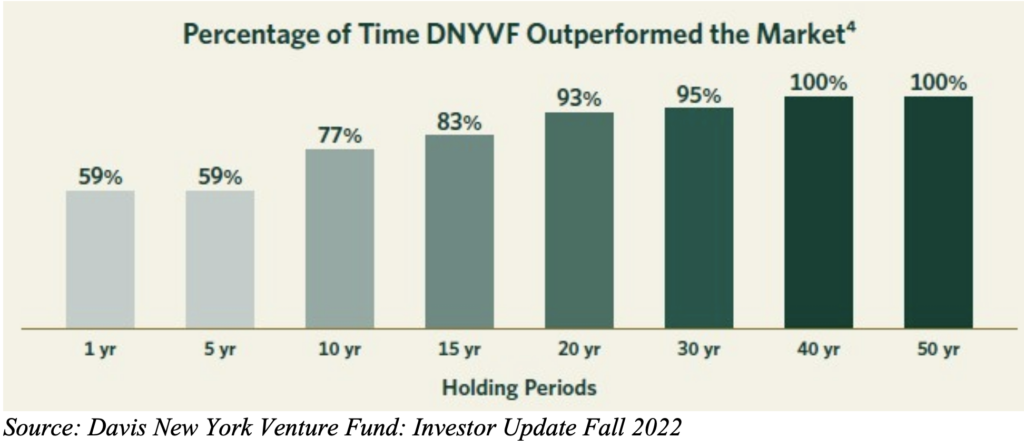

In the letter, Chris Davis shared this chart. It shows how often Davis NY fund has outperformed the market (in this case, the S&P 500 index) since its founding in 1969.

This is an interesting chart. In last 52 years, if I had invested in the fund and stayed invested for ten years, I would have beaten the S&P 500 index more often than not. About 77 out of 100 times, I would have come out ahead. This is an excellent winning average. Not many other mutual funds can boast of a record like this.

Most actively managed mutual funds haven’t been in business since 1969. And then very few managers have the kind of substantial personal wealth (to the tune of about $2 billion) invested in their own funds like Chris Davis does. 85% of mutual fund managers have less than one million dollars of own money invested in their funds.

So is it a good time to invest with Chris Davis? I think so, yes. So long as we’ve ten years to stay invested. [Ten years is not an unreasonable time frame for long term investors. Three years ago, I wrote about investments I have kept for a decade: A coffee can approach to investing]

While we are talking about market outperformance, another great candidate to buy today would be Berkshire Hathaway (BRK.A, BRK.B). Berkshire’s stock too hasn’t kept pace with the market during the last ten years. Just like in Chris Davis’ case, it is Mr. Buffett’s dislike of buying high flying over-valued growthy stocks (or entire businesses) that is at least partly responsible for its underperformance.

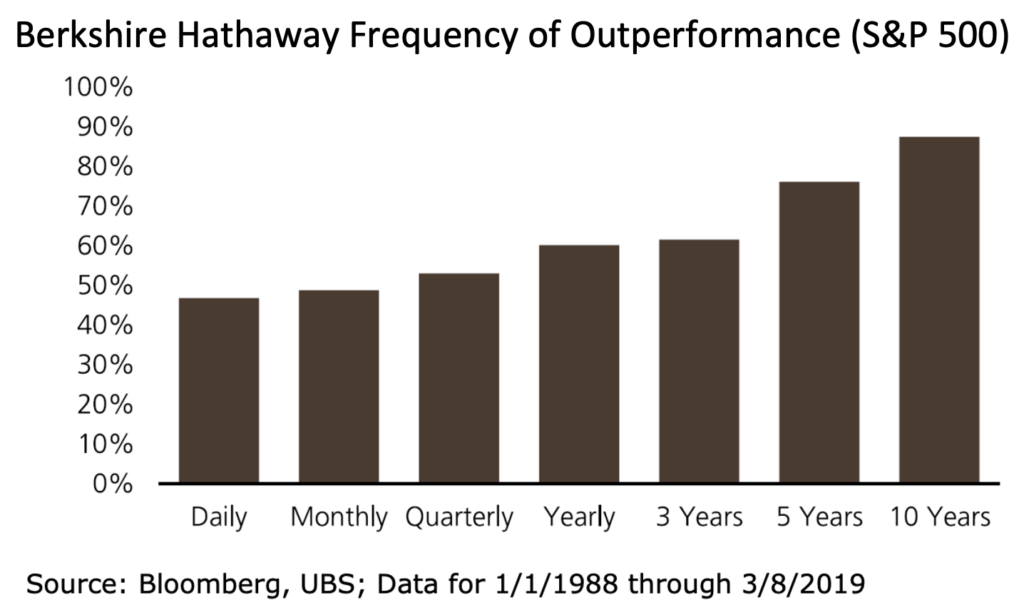

Like Davis New York fund, Berkshire Hathaway’s history of beating the S&P 500 is also outstanding. In fact, Berkshire does better than Davis. See this chart (src: Firing Warren Buffett):

Since 1988, Berkshire has beaten the market nearly 85% of the time in any rolling ten-year period. This is even more impressive than Davis fund’s performance. I like these odds. An outstanding business like Berkshire with strong odds of winning if I stay invested for a decade. It hasn’t done so well in the most recent ten-year period which makes its odds of winning even more appealing for the next ten years.

Berkshire has long been my top-five holding. This market downturn, I added to my position in May when it was trading near $300. Today, it is down a further 8%. Its price to book value today is 1.3x. For perspective, during the last ten years, Berkshire has traded at an average of 1.4 times book value. I am considering adding to my position today.

Some thoughts on this current bear market: I haven’t bought any new shares since June when I last reported. 36% of my portfolio’s dry powder cash is already invested in stocks. The market hasn’t gone further down since its June low. If it does, I will have more opportunities to deploy cash.

Regardless of where the market will go from here, it’s good to keep a long-term perspective. Bear markets are inevitable part of the investing landscape. I don’t try to avoid them. Rather, I attempt to take advantage of them. This blurb, taken from Worm Capital’s recent investor letter, expresses my view well:

Bear markets are inherently uncomfortable, but historically, they have been short-lived. They also have tended to be followed by much longer periods of market growth. As we wrote in our Q1 letter earlier this year, “major declines are relatively rare, and always followed by five to 10 years of ‘good times,’ in our experience.” Historically, markets also tend to bottom midway through economic downturns.

For any long-term investor, short-term market fluctuations should be considered noise. If anything, they are typically a good time to load up on one’s highest conviction ideas.

Berkshire is one of my high conviction ideas today.

Leave a Reply