These days, there is a steady drumbeat in the financial media about an imminent economic recession in the country. I don’t have a position on whether one is inevitable. I try to only invest in quality businesses that can survive (and even thrive) in a recession. Like Chris Davis of Davis Funds, who said in a 2020 interview that he bought stocks with the expectation that he’d hold them through a recession or two.

I wrote about that very insightful Chris Davis interview in April 2020 when we were in the middle of the last recession. Davis pointed out that he prefers to invest in businesses where he may be unable to estimate the next-year’s earnings but still has enormous confidence in their resiliency to survive an economic downturn.

My investing approach is similar. I don’t sell for the fear of a recession. I stay invested in resilient, quality businesses that can handle a downturn.

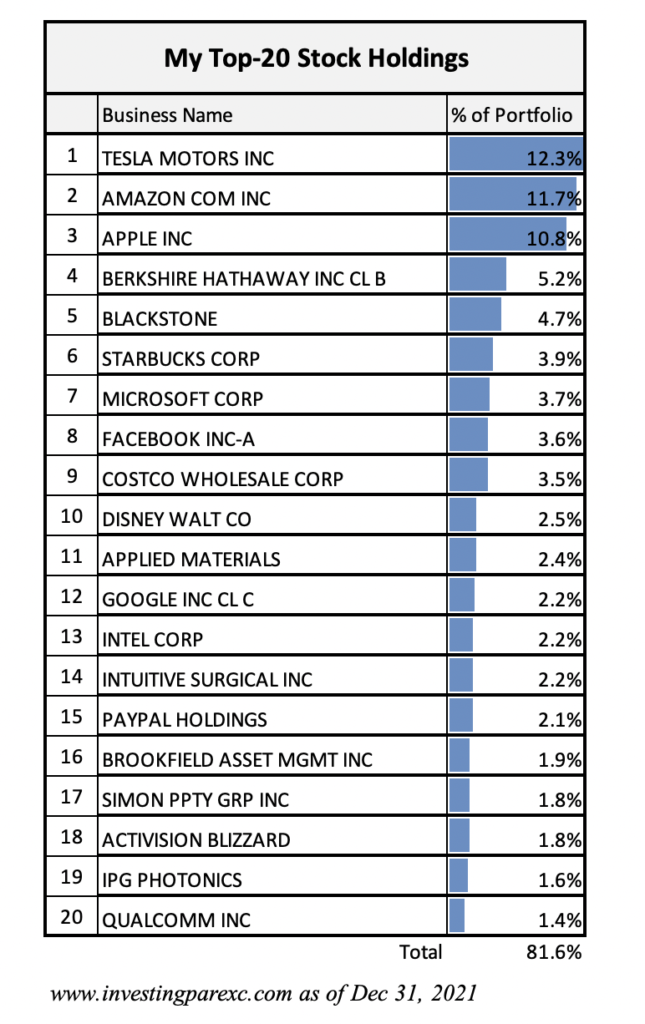

With that in mind, for this post I decided to run down some numbers on my top-20 holdings. I wanted to see how they had performed in a previous recession. I picked the Great Financial Crisis (GFC) of 2008-09 for this analysis. I didn’t bother with the 2020 Covid recession because it was very short-lived, and its economic pain was not evenly spread.

My top-20 positions at the beginning of this year (before this current downturn started) were shared in this blog post. For this analysis, I had to exclude four of the twenty stocks: Tesla (TSLA), FB/Meta (META), PayPal (PYPL), and Activision (ATVI). Tesla and Meta were not public companies in 2007. PayPal was still part of eBay. Activision had just finalized its merger with Blizzard in July 2008, making apple to apple earnings comparisons difficult from the previous years.

So how did my remaining 16 businesses fare during the GFC? Here are the details:

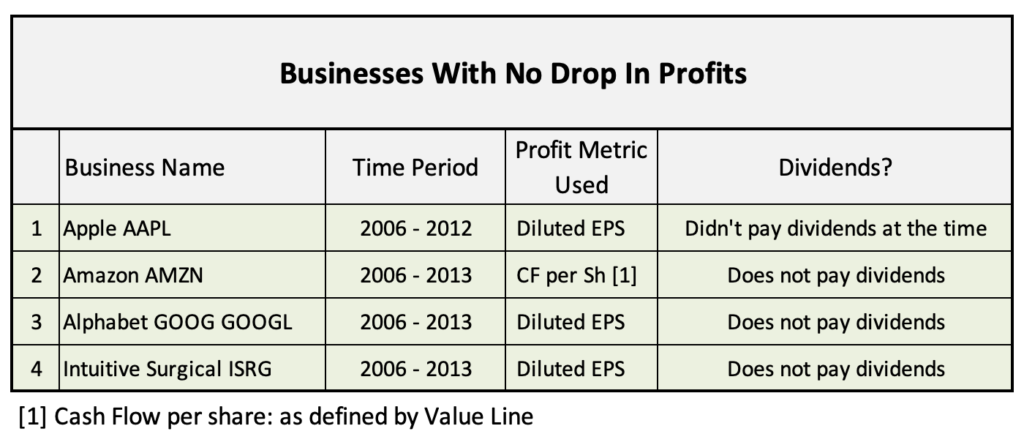

Businesses that sailed through: Four of my favorite businesses went through that entire recession as if nothing had happened. They increased both revenue and profit YoY during and immediately after the GFC. None of them paid any dividends back then (Apple started paying in 2012). But if they were, they would have no issues to continue paying throughout that period. In fact, if we pretend to not look at their share prices and just focus on business fundamentals, these four companies were nearly unaffected by the economic malaise of those times. Other than their growth rates slowed down some in 2008-09 and managements recalibrated their near-term expansion plans.

On a sidenote here, I used Cash Flow instead of EPS to measure Amazon’s profits. Cash Flow in this context means earnings with depreciation/amortization expenses added back (Value Line definition). At the time, Amazon was plowing back nearly all its profits into growth, so its GAAP earnings were depressed and did not represent actual profits that the business was generating.

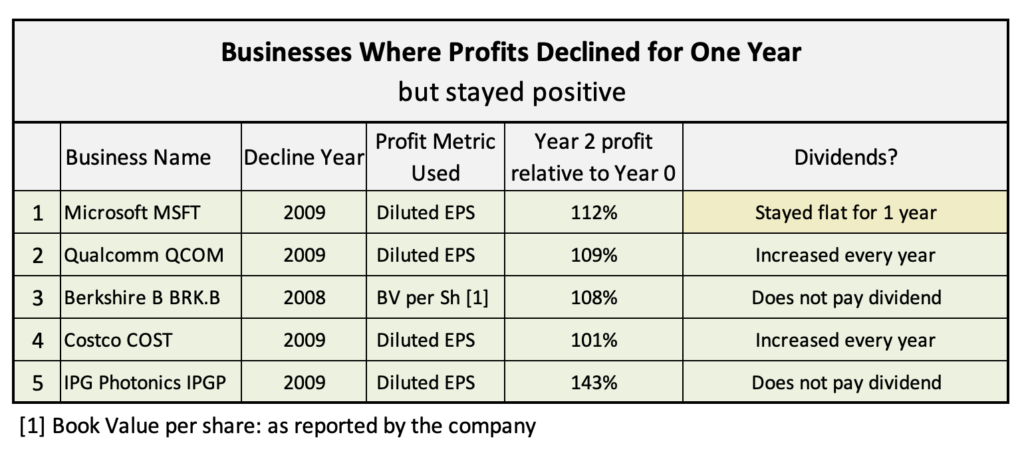

One-year declines: Next comes a group of businesses whose profits took a short dip (one year or less) but recovered quickly in Year 2. To illustrate, look at Microsoft in the table. Its earnings per share declined in 2009 and then strongly recovered (12% above ‘08 EPS) in 2010. Same with the other four companies. Three of them were dividend payers and they continued paying throughout. Microsoft did not increase per-share dividend in 2009, but Costco and Qualcomm did.

In Berkshire’s case, I used book value per share as its measure of profitability. This is a common practice for financials and more accurately reflects their underlying business performances.

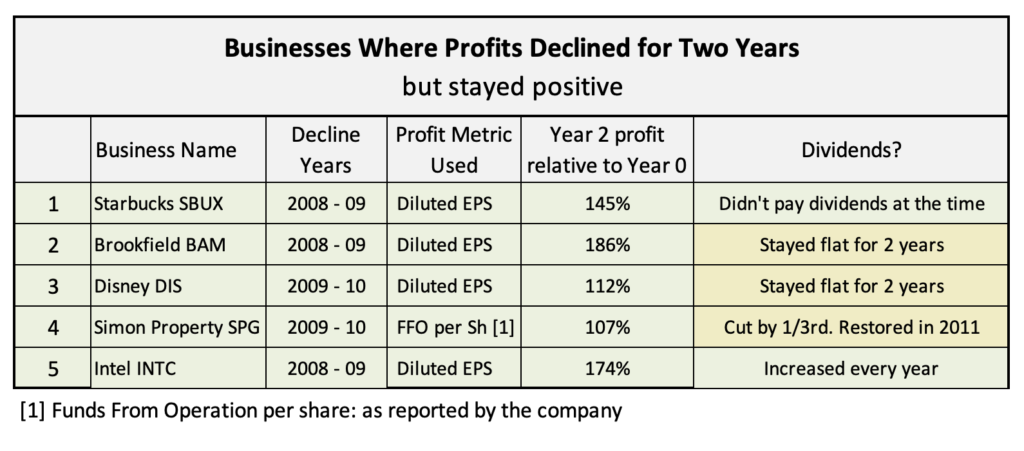

Two-year declines: These five companies did fine during the GFC, never lost any money and had no balance-sheet issues. But their profits declined for two years in a row (2009 and 2010) before recovering strongly in 2011. You can see from the table how Starbucks, Brookfield, and Intel EPS came roaring back after two years of declines, up 45, 86, and 74% respectively from 2007 peaks. Dividend payers continued to pay. Simon Property, whose mall real-estate business was worst affected by the consumer spending slowdown, did cut the dividend by 33% but then fully restored it in less than two years.

Note that I am using FFO per share (Funds from Operation) as the relevant profit proxy for Simon. FFO is a commonly used profitability measure in the REIT industry.

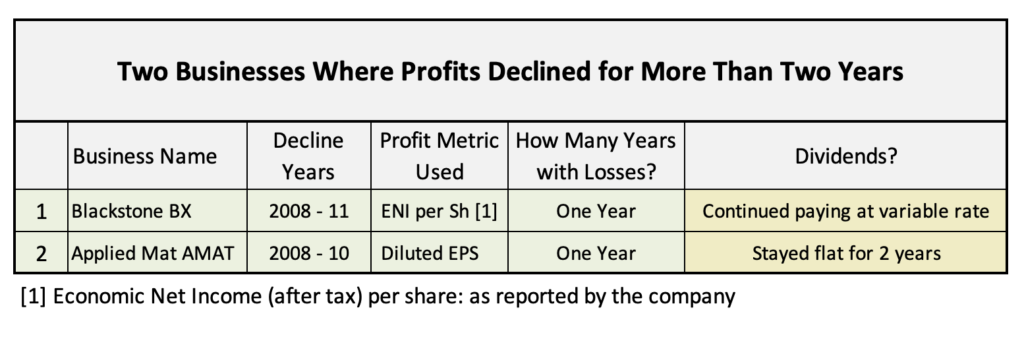

Two businesses that took the longest to recover were Blackstone (BX) and Applied Materials (AMAT). But that does not mean the two are lesser quality franchises. Blackstone, which I have written extensively about in a previous blog post here, is an excellent founder-run business. If we go by its traditional profit metric, Economic Net Income (ENI) per share, BX did not regain its peak earnings until 2012. However, the nature of alternatives asset management is such that profits are not consistent year to year. BX makes multi-year investments on behalf of its clients and does not realize performance fees until those investments are exited. It is also a pro-cyclical business where more profits are earned when the economy is expanding. During the GFC, many of its investment exits were delayed until markets had normalized, resulting in Blackstone profits getting deferred.

Today’s Blackstone is a more diverse business. Equally importantly, today a significant portion of its profits comes from managing perpetual capital in the form of yearly management fees. In the next downturn, I expect Blackstone to fare better and earn more consistent profits.

Applied Material plays a dominant role in the semiconductor equipment industry. It is one of the two largest wafer fab equipment manufacturer in the world. Unlike Blackstone, it is a much older company, founded in the 1970s. But it operates in a highly cyclical industry, driven by multi-year cap-ex driven cycles. During the GFC when the chip industry froze all expansion activities, AMAT business also suffered. EPS stayed down for three years even though 2009 was the only year where it lost money. But it is a well-run business with strong balance sheet. While dividends were not a big fraction of its total earnings, it kept paying them uninterrupted throughout the period.

Blackstone and Applied Materials business quality can be judged from what happened since the GFC. During the last ten years (2012 to 2021), BX has increased its earnings and dividends by 23% and 9% CAGR. AMAT has done even better with 23% and 12.5% CAGR. Both BX and AMAT are excellent business to keep for the long term.

In the big picture, those 16 businesses did quite well during the last major recession. None of them had any financial troubles. Those who were paying dividends continued to do so (except one). Four sailed through without even a hiccup. Ten others saw their earnings decline for less than two years before fully recovering. Most importantly, none of them were permanently damaged by the severe economic turbulence of those times.

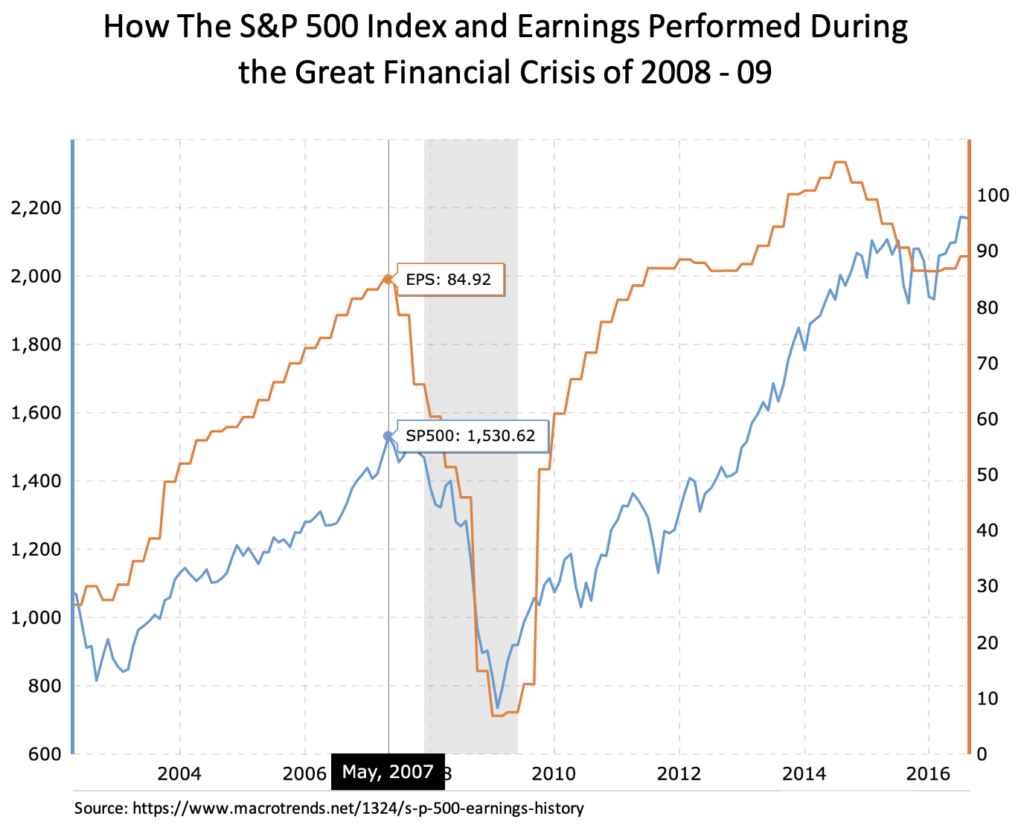

In contrast, it took the S&P 500 companies four years reach to their prior peak combined EPS. See below chart. Clearly my group of businesses did far better.

Focus on the business, not its share price: This financial outperformance is ultimately what counts. Not how individual stock prices fare. As seen in the chart above. The S&P 500 index took an extra year and a half (after achieving record EPS) to reach its prior peak price. Most of my holdings also took longer to recover. Since I wasn’t in those businesses to make quick exits, it didn’t bother me. I prefer to see my companies excel financially first. Share prices take care of themselves eventually.

I wrote in October 2019 that I consider myself fortunate to have gone through two bear markets in my investing career. That was before Covid – so today my count is three. The first two bears were very deep, about 50% drop each time. On the other hand, garden variety bear markets only drop about 25% on average. See the details here. I don’t know how long this bear market will last or how deep it will be. But eventually, it will also give way to a new bull market. Happy investing!

Epilogue: Since my last blog post published on June 7, the S&P 500 index had dropped further. As a result, I was able to deploy more of my dry powder cash. Details in the next update.

Leave a Reply