In May 2020 annual shareholder meeting, Warren Buffett said this:

“You’ve got to be prepared when you buy a stock to have it go down 50% or more and be comfortable with it, as long as you’re comfortable with the holding.”

He went on by pointing out that Berkshire Hathaway’s stock has also suffered this 50% drop three times in its history. So far. The stock’s worst drop was 59% that occurred in 1973-75 period. Its most recent 50% drop happened, as expected, during the GFC (Great Financial Crisis) of 2008-09 when it dropped by nearly 51%.

I wrote about this volatility in Berkshire shares four years ago in a blog post here. I wondered then what did it say about Mr. Buffett’s investing acumen when the greatest investor of all times himself suffered these huge haircuts.

50% stock drops happen, even to excellent businesses like Berkshire’s. We the long-term investors can’t avoid them. Neither can Mr. Buffett. Each time it happened, his own net worth was cut down by an equal amount. That’s because most of his net worth is in Berkshire shares. Of course, it goes without saying that despite those setbacks, he still managed to become one of the most successful investors in the world.

It’s also clear that many investors don’t do well when faced with such 50% drops in their stock positions. Buffett went on to say this:

“Some people are more subject to fear than others… If they can’t handle it psychologically, then you really shouldn’t own stocks, because you’re going to buy and sell them at the wrong time… I don’t know whether today is a great day to buy stocks. I know it will work out over 20 or 30 years. I don’t know whether it’ll work out over two years at all.”

Today (March 11, 2022), the stock market is in correction territory. The S&P 500 is down by about 13%, the NASDAQ composite by about 21%, and my own net worth is off its peak by 15%. With the NASDAQ sporting the steepest decline, it’s not surprising that many high-flying new tech businesses are faring the worst. Many of them are down by more than 50%, some by as much as 70 to 80% off their last year’s peaks. Among those are some well-known media darlings such as Stitch Fix, Zoom, Peloton, etc.

Would these stocks also recover just like Berkshire had recovered from previous major slumps? I am not sure. Many of them have unproven business models, fragile balance sheets, and therefore uncertain prospects. Most of them I don’t own. Neither do I closely monitor them.

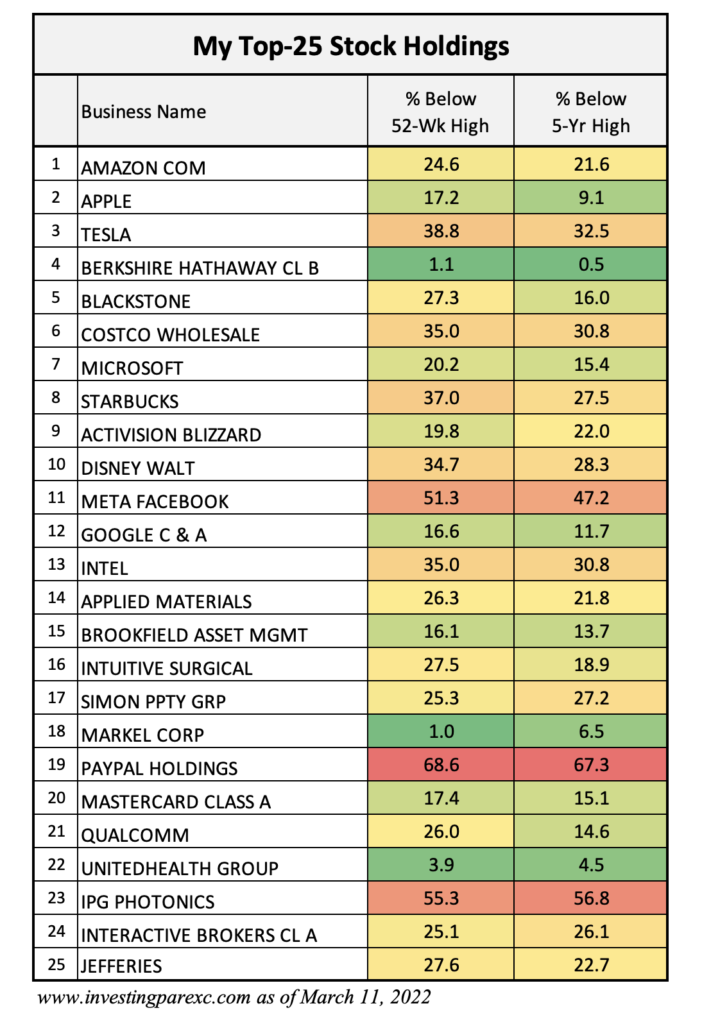

Among the stocks I own, there are only a couple that are down by more than 50% today. Here’s my top-25 stocks today:

Majority of my top holdings are down by double digits. 16 out of 25 are down by 25% or more. If I just take a simple arithmetic average assuming all these stocks have equal weight in my portfolio, I’d be down by about 27%. However, as I mentioned earlier, my overall net worth is only down by ~15%. Why this discrepancy? Partly it’s because I hold other asset classes too: cash and principal protected positions (dry powder cash, rainy day cash fund), and residential real estate. I broke them down in more detail in a November 2019 post — see here. Another reason is that not all stock fluctuations are correlated. Individual stocks did not all make their 52-week highs at the same time, and thus did not coincide with my portfolio’s 52-week high. Also worth pointing out is that my top-25 positions shown in the table constitute about 85% of the total. The rest are miscellaneous small positions that I am either in the process of winding down or gradually building.

Three of my stocks are down by more than 50% today. Do I still have faith in them? Yes. Am I confident that they will eventually recover? Yes. Let’s go over each of them.

Meta/Facebook: I’ve owned it since just after its IPO, nearly nine years ago. It’s still run by its founder CEO Zuckerberg who has done a wonderful job growing it at a phenomenal rate (5-year revenue growth CAGR 40%). It’s a highly profitable business (40% operating margin, 30% return on equity). No other social media network even comes close to its scale (~3bn people use one of its apps daily). It’s also the second largest ad network in the world, just behind Alphabet.

Today FB shares are down for several reasons. Its user growth has slowed down in North America and Europe due to saturation. Ad market growth has some near-term hiccups due to its pivoting towards short-form videos. Apple’s recent privacy moves have also made it more difficult to efficiently target ads, and this has affected ad prices some. On top of it all, the company is investing a substantial portion of its profits ($10bn out of $46bn operating income in 2021) into its metaverse AR/VR platform.

In my view these are all near-term concerns. Its core business is still doing very well. Metaverse investments are clearly risky, but I tend to trust Zuckerberg to do the rational thing: invest aggressively but walk away from it if it doesn’t pan out. He’s still the largest stakeholder in the business and I am willing to go along with him as a minority shareholder.

PayPal: I’ve owned PayPal shares even before it went public in 2015. That’s because I held eBay shares at the time PayPal was spun off from it in July 2015. Since then, I have sold my eBay stake but kept PayPal.

PayPal is also a wonderful business. It is the dominant digital wallet in NA/Europe (76% of top 1500 largest online retailers accept PayPal as compared to just 27% for Apple Pay, its nearest competitor). It is also a very profitable business with 21% FCF margin and ROIC (Return on Invested Capital, excluding goodwill) averaging 30% since the spinoff. Its balance sheet also sports a net surplus cash of ~$7bn.

One major reason why PayPal shares are down so much today is its high valuation. At its peak last year, it sported a 71x multiple of earnings. That was not sustainable. Today it is trading at a reasonable ~22x multiple. The market was too enthused with PayPal’s growth prospects during the last two years. However, with Covid effects on e-commerce subsiding along with an unexpectedly fast eBay transition to its own managed pay service, PayPal’s growth expectations in 2022 are not that high anymore. 2022 will be a slower growth year and management is focused on increasing user growth rather than adding new accounts.

PayPal is not a founder run company. However, its CEO Dan Schulman has been at the helm since the spinoff. His capital allocation record so far is quite good, with Braintree/Venmo acquisition, BNPL (Buy Now Pay Later) development, strategic alignment with banks/card networks, and focus on further strengthening its two-sided consumer-merchant network moat.

I continue to believe in PayPal’s underlying business strength. It will be difficult for a new competitor to enter this space and achieve a scale similar to PayPal.

IPG Photonics: IPGP, unlike Facebook and PayPal, is not a consumer facing company. It’s also a relatively small mid-cap business ($6bn total market cap). IPGP is the leader in fiber laser technology. It sells its products directly to manufacturers as well as OEMs that make industrial use welding/cutting instruments.

I own IPGP shares since 2008. I was initially attracted to the business because of its leading technology, a founder-owner management, and its financials. I still like the business for the same reasons, even though the stock has been quite volatile over the years. Its detractors would say that IPGP’s total addressable market is not very big, and its Chinese competitors have low-cost advantage over it. Both arguments are true to some extent. However, IPGP has clear technology edge over the Chinese. And with EV/battery industry growing fast and increasing medical applications, fiber laser products are expected to grow well.

I like that IPGP management is very long tenured (current CEO was a co-founder) and disciplined about capital spending. IPGP has been a selective acquirer and spends far more on internal R&D. It has vertically integrated its manufacturing. It operates in a highly cyclical cap-ex driven industry which is currently going through a down cycle due to Covid slow-down and geopolitical situation. Like previous downturns, IPGP continues to stay cash flow positive and has ample net cash on its balance sheet. I like the strength of its business and plan to stay as a shareholder.

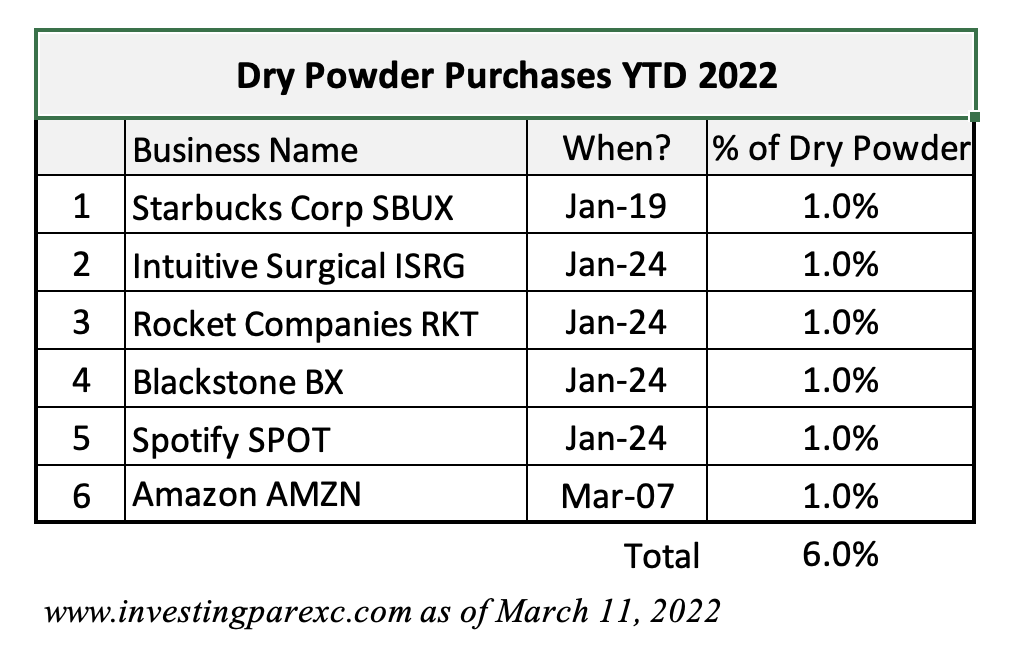

My dry powder: I wrote last month that I have been deploying my dry powder cash into stocks as they went down. Since then, there wasn’t much activity in this area except that I bought additional Amazon shares last week. As of today, I have used up 6% of my dry powder cash. The market continues to be volatile but today it is at more or less the same level as last month. If it goes down further, I stand ready to buy more stocks at even better prices.

Leave a Reply