Bill Ackman is a well-known and widely followed hedge fund manager. During the Covid market selloff in early 2020, he made several billion dollars by timely moving in and out of the markets. First, he bought credit default swaps to hedge against panic in the bond market. That netted him more than two billion dollars in profits. Then he correctly anticipated the market’s quick recovery by investing that money (and some of his dry powder cash) into common stocks for further gains. He made two successful bets in a short span of few months. His first bet was on imminent economic shutdown of the country due to Covid. And then he correctly foresaw the economic reopening. His big trade that netted him $3.6 billion in short order is well documented in the financial press. See this Barron’s article, for instance.

What he did for his fund was pretty amazing. Great market timing! Could I as an individual investor have made similar moves (even if not on the same scale)? Not a chance!

Mr. Ackman has certain obvious advantages over us, the lowly individual investors. He can afford to hire talented investment professionals, likely has a good number of smart research people working for him, has access to institutional level assets (e.g. credit default swaps), and above all, has resources to quickly pivot and change his investing direction.

But I as an individual investor have my own advantages – no clients to report to, no quarterly imperative to show profits (or beat an index), and no fixed timeline to deliver. In other words, I can afford to be slow and deliberate in my investing decisions, unlike a hedge fund manager. I can also keep my investing simple (do I really have a choice?). I am not being paid by clients to deploy complex trading strategies to generate alpha. All I need is a long-term commitment to durable businesses, a steady hand in turbulent times, and a reasonable cash portion to take advantage of inevitable market drops.

I could have been invested in Mr. Ackman’s closed-end fund Pershing Square Holdings Ltd. (PSH is open to all investors), but I wasn’t. As much as I admire Bill Ackman’s investing acumen, I prefer to invest on my own. I might not generate a ton of alpha, or outperform his fund. But I bet I can outperform most individual investors by staying invested in good businesses through thick and thin. As I wrote about it last month, I managed to beat both the S&P 500 and the NASDAQ composite over the last 3- and 5-year periods.

Why am I comparing myself with Mr. Ackman? After all, we don’t even play in the same league. And yet there are lessons to be learned from thinking through and contrasting his and my motivations for investing decisions. In the same vein, I once sized up my (rather meager) personal portfolio against Yale University’s endowment fund run by late David Swensen. I wanted to see how Yale’s asset allocation would compare to mine. See this blog post (Benchmarking against Yale’s endowment) from 2018. Another time, I measured my portfolio’s concentration with Berkshire Hathaway’s public equity portfolio (What’d Buffett do?) to check if I am overdoing it.

March 2020 was an unusual period. It was rife with uncertainty and fear of the unknown. Even smart and well-read investors were prone to panic selling, or at least cut down on their stock holdings. Take the example of @borrowed_ideas. He’s a savvy business analyst (I subscribe to his paid equity research). He’s young (from Gen Z cohort), having just started working a few years ago. As the market staged a recovery from its March 23rd trough, he was concerned that it was just a bear market rally, bound to drop again. So in the first week of April 2020, he increased his cash holdings from 13 to 18.5%. At the time, the market was still down by about 20% off its peak. Not that I want to pick on him but selling stocks to increase cash when there is panic selling all around is not a wise move. Time to increase cash holdings is when stocks are doing well. Time to right-size one’s cash holding in anticipation of future crises is also then. Like in late 2020 or 2021. When you are young and resourceful, you can afford to ride out any market volatility.

What was I doing in March? Unlike Mr. Ackman’s perfectly timed market moves and @borrowed_ideas somewhat ill-timed cash raising, I was content in simply following my dry powder cash playbook. Throughout February and March 2020, I invested 70% of my dry powder cash in fallen stocks. You can see what I bought from my blog updates here and here. In early February that year, total cash (both dry powder and rainy-day funds) stood at 13%. By the end of March, my cash holdings had dwindled to 8%. I was investing as stocks were falling. I wasn’t concerned with how much further stocks were going to fall.

What did I do in 2021? Like most investors (I guess Ackman was an exception), I had no idea how the market would behave after the initial Covid panic selloff. As stocks recovered in April and then doubled over the following 18 months, I gradually increased my dry powder cash. At the end of 2021, I had about 16% of my portfolio in cash. In absolute terms, this was a lot more cash than what I had in early 2020 because by then my portfolio had also gone up by 60%. As my stock holdings grew, I gradually sold some throughout 2021 to increase cash. As I said, the time to raise cash was in 2021, not in March 2020.

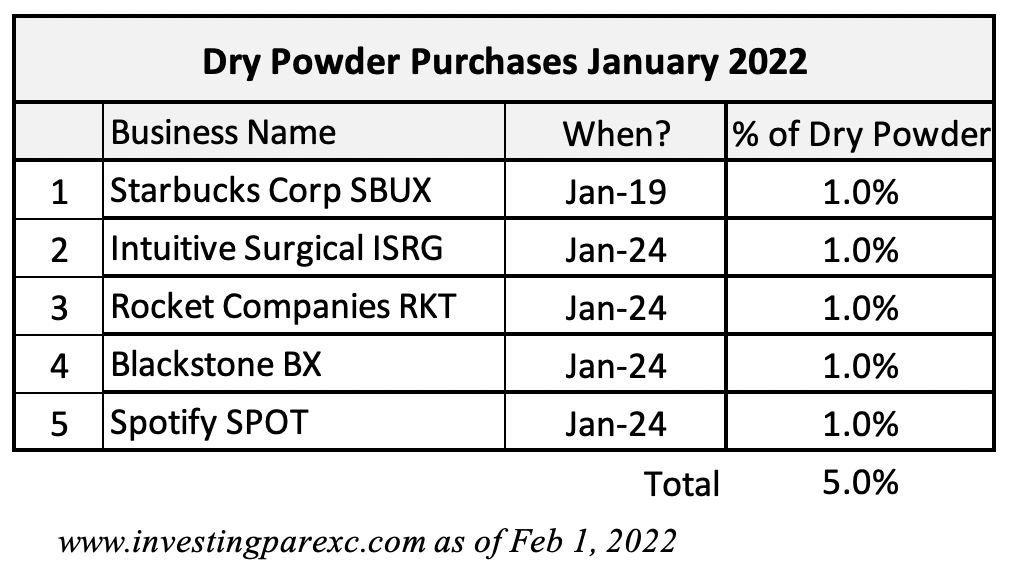

Where I stand today? Stocks have been falling again since the beginning of the year. This time the worries are different — inflation and interest rate hikes, not Covid shutdowns. Nevertheless, as the S&P 500 dropped below 10% in January, I once again started scooping up some bargains. Per my dry powder rulebook, I am supposed to invest up to 10% of cash when the market is down between 10% and 15%. But the S&P 500 only went down by about 12% in late January. So I managed to deploy just 5% of available cash so far. What did I buy? See the table below:

I’ve owned four of these businesses for years. Only Spotify is a new holding. I greatly admire Starbucks, Intuitive Surgical, and Blackstone as durable long-term advantaged businesses. I wait for opportunities to add to my positions. See my previous thoughts on them here, here, and here. I must say I am especially happy to increase my ISRG position. This was the first time I had bought ISRG shares since 2013.

Rocket is a relatively recent position. I’ve only begun buying the stock about a year ago. See my initial thoughts on Rocket from last year here.

Spotify is a business I haven’t written about before. I have only bought it twice. It’s a small position. Spotify is the founder-run streaming music leader worldwide. It has twice as many subscribers as Apple music, its nearest competitor. It is also the global leader in podcast streaming. Though not highly profitable yet (doesn’t have scale yet), it has zero debt and generate enough operating cash flow to acquire more content and more subscribers. It is a risky but small position in my portfolio. I will be watching Spotify’s progress closely as it gains scale and develop an economic moat.

This market downturn hasn’t ended, so it’s possible that I will get more opportunities in the near future to deploy cash into stocks. I am comfortable in doing that. As I wrote in a blog post, I size my cash holdings appropriately for my next three to five year cash needs. Dry powder cash could one day go all in stocks (if stocks are down by more than 50%), but my rainy-day funds will still be there in safe cash-like assets.

Leave a Reply