Costco just announced a special dividend of $10 per share, payable in December. This is their fourth special dividend payment to the shareholders in last eight years.

It’s called special dividend because it is in addition to the regular dividend that Costco pays every quarter. Also, this is not regularly scheduled so we shareholders can’t always predict it very well.

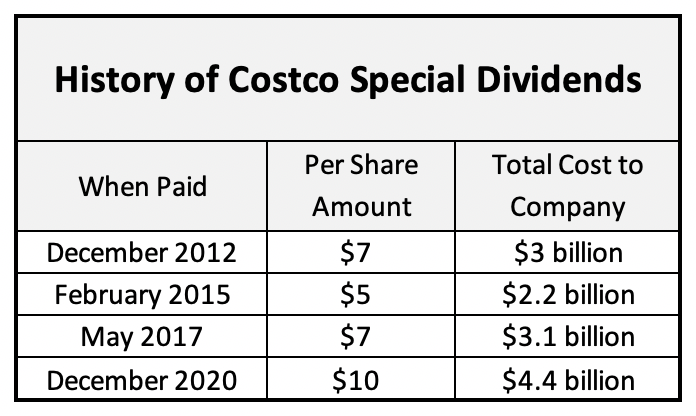

Of the four special dividends that Costco has paid so far, this is the highest per-share dollar wise. Last three were $7 in 2012, $5 in 2015, and $7 in 2017. Combined with the next month’s payment, it amounts to a total of $29 per share. Today, each Costco share trades at about $390. Or roughly 1.8% effective annual yield. If we throw in the 0.7% regular dividend yield, we get an overall dividend yield of 2.5% averaged over the last four years.

I own Costco shares since 2009. With my average cost basis of $75 per share (I have bought multiple times since my first purchase in 2009), the company has returned $29 to me since then. Just in special dividends.

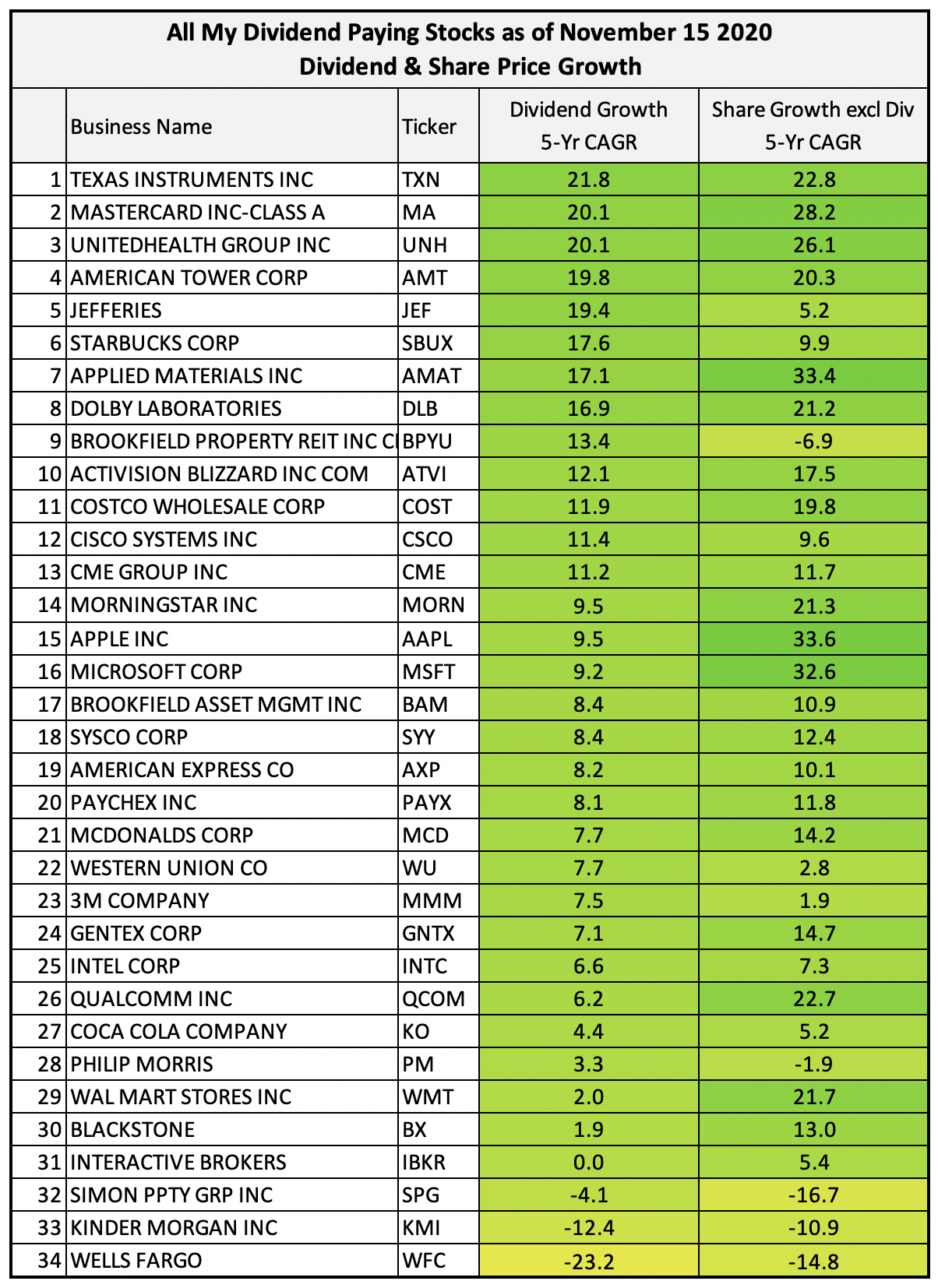

Let’s turn to Costco’s ordinary dividends first. As I shared in my last blog post, Costco has increased its regular dividends at 11.9% CAGR in past five years. Perhaps not surprisingly, its share price has increased at an even higher clip in that period—about 19.8% CAGR. We long-term shareholders were already being treated well by the Costco management. The special dividends are just icings on this yummy cake.

A brief history of Costco’s special dividends: When it first paid out a special dividend of $5 in late 2012, it cost the company $3 billion. At the time, there was an impending fiscal cliff (dividend tax would have gone up starting in 2013) that might have been the catalyst for the move. Then in 2015, the payout was $5, and the total cost was $2.2 billion. In 2017, it paid $7 special dividend with the total price tag of $3.1 billion.

In each of the first three cases, Costco raised new long-term debt to partially pay for this expense. While this move would normally be frowned upon by investors and analysts alike—taking on unnecessary debt to pay shareholders—it was justified in this case. Costco’s balance sheet had been strong but underleveraged. It had ample balance sheet capacity.

However, today’s special dividend does not come with any new debt. Management pointed out in the press release that it will be paid entirely from existing cash on its balance sheet. This year’s payment is also the largest, amounting to $4.4 billion total.

Costco is a beautiful and yet simple business, run by great shareholder friendly managers and an excellent company board. In a 2018 blog post (Are moats really lame?), I wrote about my investment thesis on Costco. I wrote then that Costco is one of my all-time favorite business to own. It also has a wide economic moat to keep competitors at bay. It has reputation, scale, and great execution on its side. See my full profile on Costco here.

Why I like Costco’s dividends? I own many dividend paying businesses, as you can see in this table. But I also own many other businesses that don’t pay any dividends. Dividends are just one way to return capital to investors. Another is to buy back own shares. Some companies do that instead of dividends. Then there are others like Amazon who don’t do either. They reinvest all their profits into further growing the business. You can see all my reinvesters, repurchasers, and dividend payers in this blog post: Grading CEOs as capital allocators.

{kind=link}

All else being equal, dividends are not as tax friendly as share repurchases. But in case of Costco, they are arguably the best way to return profits to shareholders. Why so? Several reasons for it. One, as I explained in my earlier blog post, Costco doesn’t need all its annual profits to expand its business. It has a deliberate and time-tested approach to expanding its warehouse footprint. A recent case in point: China. Costco opened its first store in Shanghai last year, after several years of selling its wares online to Chinese customers. Even with Shanghai store’s huge success in 2019, Costco still only has two more stores planned for China this year. Its annual capital expenditure on new and remodeled stores is fairly predictable year in and year out.

Secondly, Costco’s business model doesn’t require acquisitions or R&D expenses either. So with all that excess cash flow it generates every year, it is only prudent to return it to shareholders. Here, Costco could just buy back own shares instead of paying cash dividends. But its shares have always been a bit pricey. More so, in last three years.

Share buybacks are only accretive to existing shareholders if they are done below the company’s fair value. In this case, I don’t think buybacks would have made sense, so I am happy to receive my share of profits in cash dividends.

Owner managers? Readers of this blog would know that I prefer to own businesses where managers are significant owners too. I wrote about my founder run businesses here and here. Costco is not on that list, however. But it doesn’t mean its management is not as good. The reason why Costco is not on that list is because Costco founders have retired. Costco is now being run by second-generation managers. Messrs. Sinegal and Brotman were co-founders. They ran this business from 1983 to 2012 before passing on. Today’s CEO/CFO pair is also very long tenured with Costco, and in my opinion equally good.

Another reason to admire Costco is its board of directors. At one time, it was chaired by one of the cofounders but today the board chairman is Tony James, an independent director who’s been on the board since 1988. James is Blackstone’s (BX) executive vice chairman (previously its COO), another company that I highly respect. See my Blackstone profile here.

Also on Costco’s board is the one and only Charlie Munger, Berkshire Hathaway’s vice chairman and Warren Buffett’s long-time investing partner. There are only three for-profit companies whose boards Mr. Munger sits on. Costco is one of them. Munger has been on Costco’s board since 1997.

It’s always reassuring to see this nexus of connections between good businesses. I believe Costco is in good hands today.

As I noted earlier, I own Costco shares for eleven years and counting. Today, Costco shares are trading at a premium. I haven’t bought shares since 2017. The stock has outperformed the market in last five years, so it’s possible it may underperform the next five. But I am not selling what I own. I like the business, and good businesses like these are for keeps. Even if its stock underperforms from here on, that won’t affect its inherent business quality. Meanwhile I will continue to collect dividends, both ordinary and special. After all, I am a buy right, sell never kind of an investor.

Leave a Reply