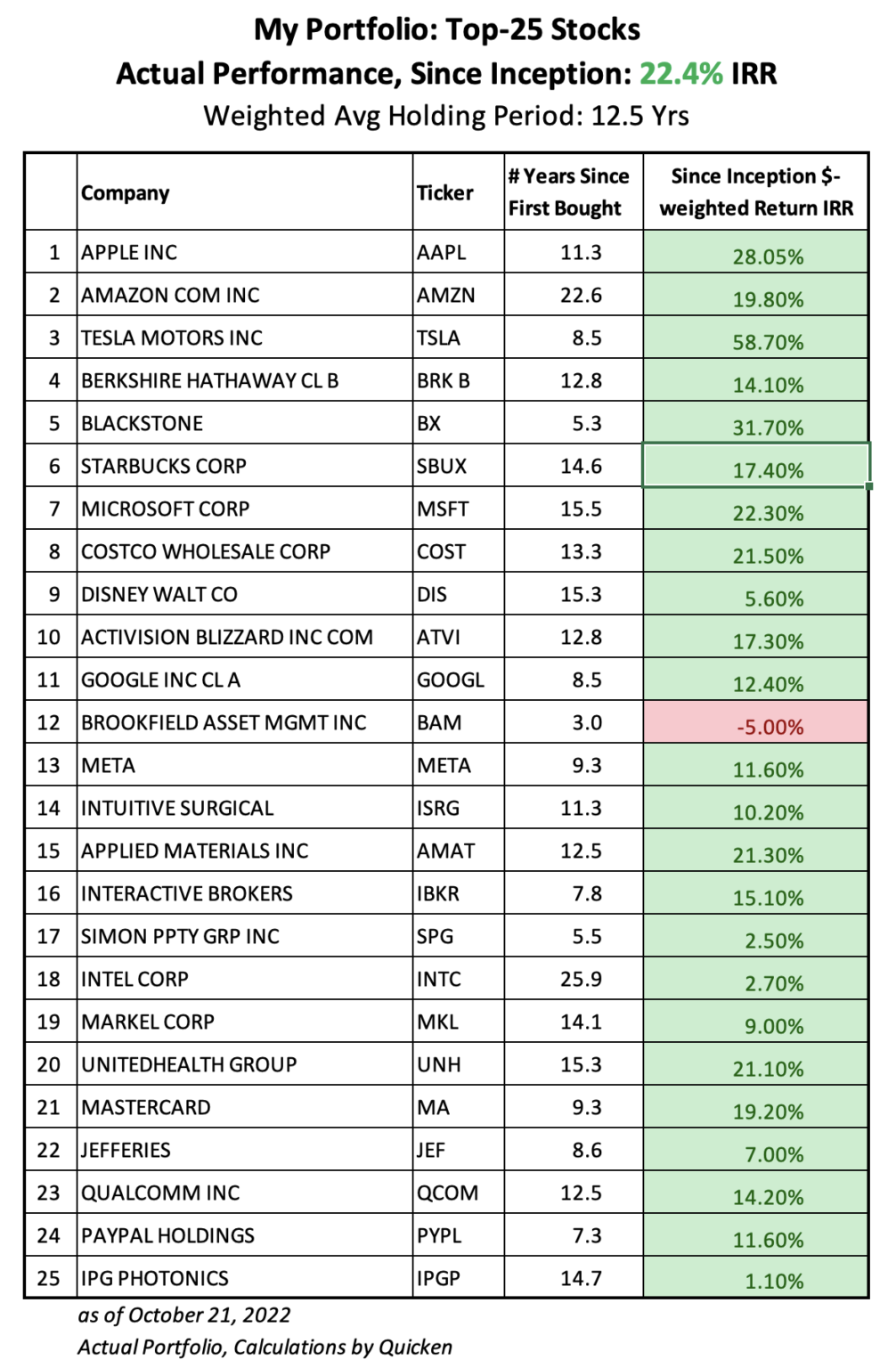

A Note on the Market: Since my last blog entry, the stock market has kept climbing the wall of worry. It has gone on to new highs recently. As I’ve said before, I don’t plan to ever get out of the market completely but I continue to gradually raise cash by taking some money off the table. As the S&P 500 reached an intra-day all-time high on May 29th, I skimmed some of my high-flying positions to raise more cash. Total cash in my portfolio now stands at 17.8% – this includes both my dry powder cash and my rainy-day funds.

Amid the prevailing optimistic sentiment in the market, there are some stocks that have been left out. Among them are travel related businesses and those that are affected by high interest rates. Two such stocks that I have in my portfolio are Booking Holdings (BKNG) and Rocket Companies (RKT). I took advantage of these two’s recent slumps to add new shares this month. This was a market neutral move, however. My cash position didn’t change. I reduced my positions in Intel (INTC), Dell (DELL), and Qualcomm (QCOM) to raise cash for the two purchases. Semiconductor stocks are trading at all-time highs these days, so rotating some capital out of them into other stocks with depressed valuations seems prudent.

Certain other businesses that I closely follow are also trading at relatively depressed valuations today, though I haven’t yet pulled the trigger on them: Blackstone BX (Alt Investment manager), Intuitive Surgical ISRG (Robotics Surgery), and Paychex PAYX (Payroll & HR).

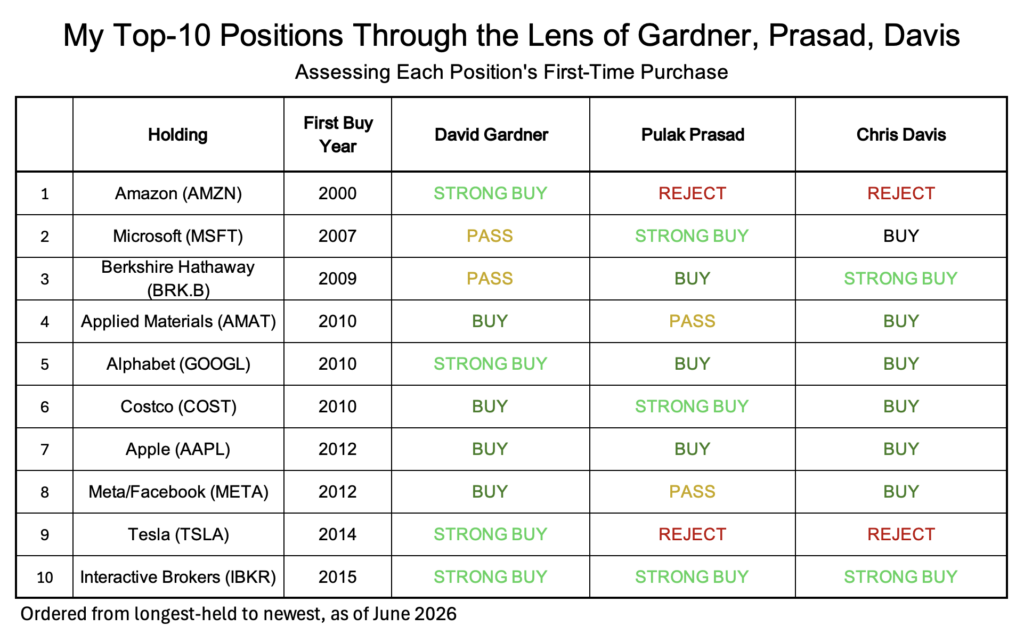

Continuing with my series on the three master investors—David Gardner, Pulak Prasad, and Chris Davis, in the remaining blog post, I will consider how the trio would have voted on my top ten holdings at the time when I first bought their shares. Note that my top holdings were built over a long period of time (often spanning a decade and more) so here I am only considering how the three would have seen the stocks at the time of my first purchases, notwithstanding any subsequent incremental purchases.

{kind=link}

Going through this exercise is also going to reveal how my own investing differs from (or matches with) their unique investing styles. And how would I characterize my own investing style based on what I bought, when I bought it, and whether the three master investors would have approved.

Last I shared my top ten portfolio positions in my January post. Today, the positions are the same but the order has changed a bit and Blackstone (BX) has fallen out of the top ten and replaced by Interactive Brokers (IBKR). For this discussion, I will go briefly over each position starting with those that are held for the longest period.

Here is how the scorecard shakes out:

Amazon (AMZN) — First Bought: 2000

Acquired during the peak of the Dot-Com bubble, when the stock was months away from undergoing a brutal 90% decline amid widespread bankruptcy fears. David Gardner would have enthusiastically endorsed this buy, viewing Jeff Bezos as a generational, “Rule-Breaking” pioneer building a potential e-commerce monopoly. Conversely, Pulak Prasad and Chris Davis would have flatly rejected the purchase due to its unproven business model, rapid cash burn, and deeply negative owner earnings, which signaled an unacceptably high risk of near-term extinction.

Microsoft (MSFT) — First Bought: 2007

Purchased during the uninspiring Steve Ballmer era, a time when Wall Street largely dismissed the tech giant as a stagnant, unexciting value trap. David Gardner would have passed on the stock, classifying it as a slow-moving “Rule Maker” that lacked the explosive, open-ended growth narrative required to fuel a power-law portfolio. However, Pulak Prasad and Chris Davis would have approved, recognizing that its massive recurring enterprise cash flows, high returns on capital, sticky customers, and exceptional owner earnings yield offered a strong corporate fortress trading at a deep discount.

Berkshire Hathaway (BRK.B) — First Bought: 2009

Executed in the troughs of the Great Financial Crisis amid systemic macroeconomic panic and market capitulation. Chris Davis would have labeled this a generational screaming buy, as the stock traded near historical book value while Warren Buffett operated a supreme liquidity fortress. Pulak Prasad would have warmly agreed, viewing Berkshire as an evolutionary apex predator designed to feed on panic, whereas David Gardner would have passed due to the conglomerate’s lack of tech-driven disruption.

Applied Materials (AMAT) — First Bought: 2010

Added post-recession when semiconductor capital equipment valuations were heavily depressed from the global economic downturn. David Gardner would have approved of the purchase, viewing the business as a critical “picks and shovels” provider enabling the global mobile and digital revolution. Chris Davis would have backed the buy on cyclical troughs due to its deep engineering moats, while Pulak Prasad would have passed because the intense cyclicality of semiconductor capital spending violates his strict preference for simple, unchanging models.

Alphabet (GOOGL) — First Bought: 2010

Purchased as the post-crisis bull market took flight and Google was solidifying its dominance over digital advertising. David Gardner would have given this a strong buy for its immense network effects and technological optionality under visionary founders. Pulak Prasad would have voted yes, identifying it as an essential, debt-free, high-ROCE digital utility destined for long-term survival, while Chris Davis would have jumped in too, realizing its explosive owner earnings growth heavily justified the premium and set up a classic “Double Play.”

Costco (COST) — First Bought: 2010

Invested during a period of shaky economic recovery post GFC crisis when the market was discounting its stable, high-quality consumer model. Pulak Prasad would have given this a strong buy, viewing its highly predictable membership model, high returns on capital, and simple operational design as the epitome of evolutionary perfection. Chris Davis would have readily voted buy for its stellar capital allocation and durable defensive moat, and David Gardner would have concurred, loving Costco’s unique corporate culture and unshakeable status as a retail top dog.

Apple (AAPL) — First Bought: 2012

Acquired amid high skepticism following the passing of Steve Jobs, as Wall Street panicked that Apple’s innovation engine had permanently stalled. Chris Davis would have aggressively bought this structural disconnect, recognizing that the market was mispricing a technology juggernaut at a single-digit P/E ratio, creating a massive owner earnings yield. Pulak Prasad would have loved its immense customer lock-in and debt-free balance sheet, while David Gardner would have happily backed it as a dominant ecosystem first-mover facing a transient dark cloud.

Meta/Facebook — First Bought: 2012:

Initiated shortly after Facebook’s notoriously botched IPO, when the stock crashed amid market skepticism over its mobile transition. David Gardner would have issued a strong buy, recognizing the unprecedented network effects of social infrastructure early on. Chris Davis would have enthusiastically agreed, seeing a textbook “Double Play” candidate where a high-margin advertising monopoly was severely mispriced against its underlying cash-flow potential, whereas Pulak Prasad would have passed due to the rapid technological mutation risks present in social media at that time.

Tesla (TSLA) — First Bought: 2014

Bought when it was a controversial battleground stock facing rampant short-selling, intense capital burn, and massive manufacturing execution challenges. David Gardner would have given this his highest recommendation, celebrating Elon Musk as a visionary category creator capable of completely disrupting global automotive infrastructure. Conversely, both Pulak Prasad and Chris Davis would have issued immediate rejections because the company was hyper capital-intensive, highly speculative, completely unmeasurable by conventional value metrics, and heavily exposed to operational extinction risks.

Interactive Brokers (IBKR) — First Bought: 2015

Purchased during a period of steady market expansion as the brokerage landscape was getting reshaped by automated, programmatic trading. This represents a rare unanimous strong buy across all three frameworks. David Gardner would have cheered a technology company disguised as a brokerage disrupting legacy Wall Street structures under a visionary founder; Pulak Prasad would have loved its pristine, debt-free, high-ROCE software-like model; and Chris Davis would have highly valued its massive operating leverage, high owner earnings, and structural status as a natural beneficiary of growing investor appetite.

Final Words:

When analyzing the DNA of an investment portfolio, it is easy to get trapped in a single market dogma: Are you a hyper-growth visionary like David Gardner, a strict quality purist like Pulak Prasad, or a disciplined value compounder like Chris Davis? However, I refuse to choose.

My investing approach is dual-pronged: balancing rock-solid moated businesses with high-upside disrupters. But I have one non-negotiable rule: every company must be run by a trustworthy leader (ideally the founder) who has serious skin in the game.

While Gardner routinely ignores valuation, and Prasad and Davis routinely ignore unproven hyper-growth, my style straddles both worlds. I take big risks on passionate founders who are changing the world, but I balance that by building my foundation on unshakeable, cash-generating monopolies.

Leave a Reply