In recent months, I have seen a change in casual investors’ behaviors. They seem more interested in stocks. These days, people approach me to see if I have any hot stock tips for them. Or they ask if I think the market is too high and it’s time to bail out. My response tends to disappoint both groups. I don’t have any favorite stock that I am actively buying today, nor have I liquidated any of my stock positions lately.

It’s true that I have been trimming some stocks to increase cash holdings, as I have mentioned before in this space. But it is a gradual process, not any drastic shift. Today, I have about 17% in cash. Same time last year, I had about 16% in cash. But then I deployed some of it into stocks in April when the market dropped (the so-called Liberation Day correction). Later, I moved back into cash as the market recovered in the second half of 2025.

Today, there is clearly optimism in the stock market. We can see it reflected in the stock prices. I also see it in regular people. Stock market has become a popular topic of discussion once again. A few of my connections who normally don’t care about stocks seem to have developed sudden interest in AI or chips stocks.

My investing style is passive and contrarian. It doesn’t sit well with most casual investors. I don’t have any good buying tips for them. And when I become an active buyer of stocks, many of them are no longer interested in hearing about them. We contrarian investors could never be popular!

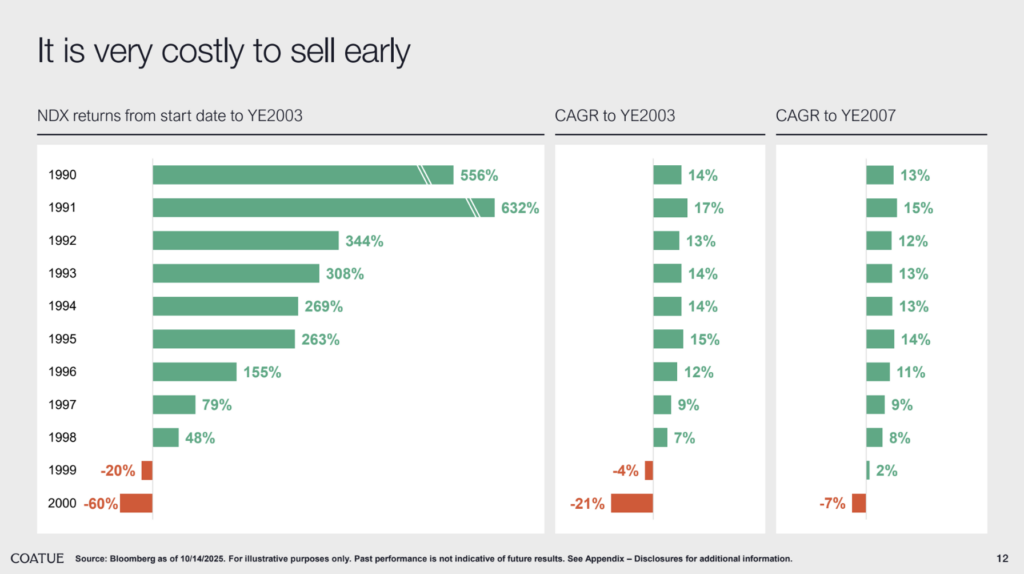

I came across an interesting chart the other day from Coatue Capital’s October 2025 investor update. They were making the case for staying invested and not getting out of the market too early. Else, the opportunity cost is too high. To prove their assertion, they picked the 1990’s bull market that ended with its peak in early 2000 and then slid down for the subsequent three years. If an investor had bought the NASDAQ-100 index (NDX) at the beginning of each year preceding the Y2K peak then held on until the end of the bear market (year-end 2003), what would be their gain or loss? This slide shows the numbers:

Coatue Public Markets Update: https://www.coatue.com/blog/perspective/public-markets-update-2025-10-16

For instance, if you bought the index at the beginning of 1996, five years before the end of the bull market, you would be up by 155% (at 12% annual return) at year-end 2003. What is striking is that if someone had bought stocks just two years before the market peak (1998), his portfolio was still profitable at the bottom of the bear market.

This goes to show that quitting stocks too soon in a bull market means you are leaving a lot of money on the table. Investors run the risk of falling so far behind in compounding that they may not ever catch up with a “buy and hold” investor.

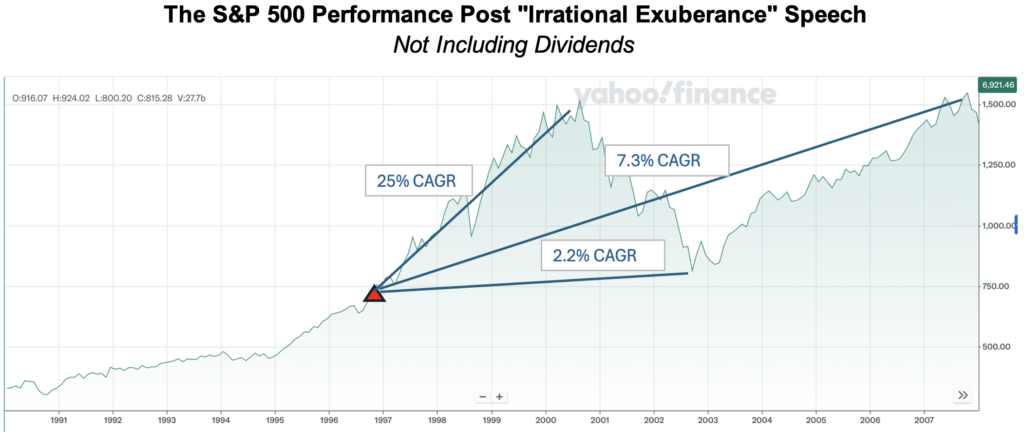

Another striking example of lost opportunity in a bull market: On December 5th, 1996, then Federal Reserve chairman Alan Greenspan gave his famous “Irrational Exuberance” speech, warning that US asset values (e.g. stocks) may be too high. But if you had sold all your stocks at the day of that speech, you missed one of the great wealth compounding periods in history. The S&P 500 went on to double over the next three years, peaking in March 2000 as shown in the chart below.

Not just that, but investors who sold off at Greenspan’s warning hoping to buy back when prices were cheaper never got the chance. Even after the dot-com crash bottomed out in 2002, the S&P 500 was still trading higher than it was when Greenspan gave his warning.

The best course of action in times like today’s is to stay invested. Ignore market predictions. No one could know when the market will top out (not even a Federal Reserve chair). Successful divesting from stocks and then redeploying at lower prices has a two-decision trap:

- When to sell: This feels like the “easy” part but remember the opportunity cost.

- When to buy back: Doing this in a timely manner is near impossible for most investors.

The 2013 Breakout: Following the 2008 crash, many investors stayed in cash, waiting for the “other shoe to drop.” The market rallied from 2009 to 2012. Investors who sold early in 2012 (fearing the “Fiscal Cliff” or European debt crisis) watched the S&P 500 surge 30% in 2013. Because the market was now 30% higher than where they sold, those investors felt they couldn’t buy back in (“It’s too expensive now!”). They remained on the sidelines for years, missing one of the longest bull runs in history.

Having said all that, today’s market is also not the best to initiate aggressive stock buying. Though if you are dollar cost averaging your savings, stay the course. For everyone else, remember that the market often goes down 10% every year and 20% every four years. There will be better times to invest down the road.

It goes without saying that when stock market turns sour, it takes some effort to go against the crowd and invest new money. Howard Marks calls it “intestinal fortitude”. Today, we need patience to resist temptation of over-paying. In down markets, we will need intestinal fortitude. Neither comes easily. We must train our minds for better mental discipline.

Postscript: I know people who were worried about market highs in 2017 and refused to invest because they thought it had been going up for too long. I wrote about them in a blog post in November 2017 (Why I stay invested in stocks?). Since then, the S&P 500 has gained about 3x (dividends reinvested) despite facing significant volatility and the bear markets of 2020 and 2022.

Leave a Reply