In his 2010 shareholder letter, Warren Buffett wrote that his elephant gun had been reloaded, and his trigger finger was itchy. He was referring to Berkshire’s dry powder cash that was intended for major acquisitions. Extending the same metaphor, today I could say that my BB gun is fully reloaded. I am ready for the next market decline. Given the size of my portfolio, it seems appropriate to call mine a BB gun – unlike an elephant gun like Mr. Buffett carries.

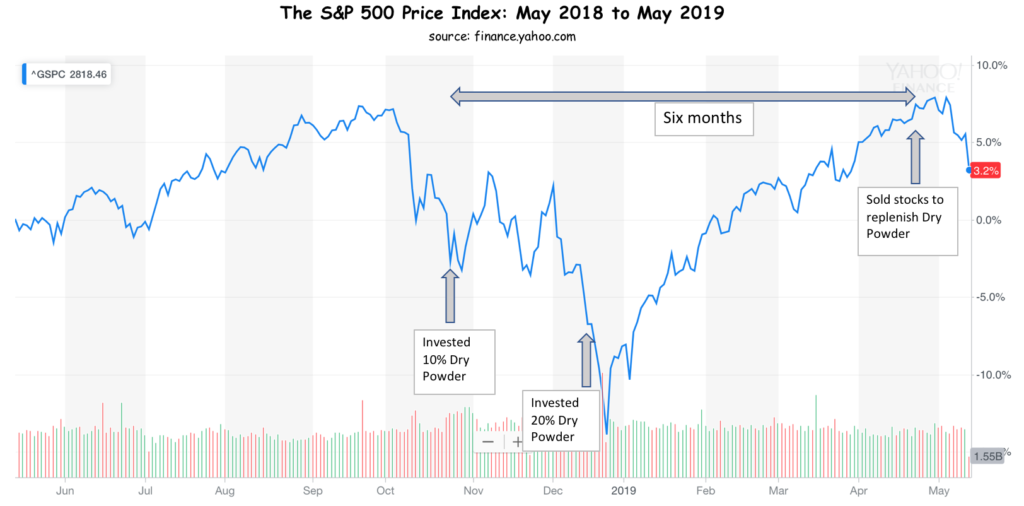

As the S&P 500 finally returned to its previous high last month, I had replenished my dry powder cash reserves by selling some stocks. Mostly I sold a fraction of my holdings in stock index funds to raise cash. I had two small stock positions in UPS and Bed Bath & Beyond that I also sold. As I explained in my November 2017 blog post (A deeper look into my portfolio), I have been gradually moving capital away from index funds and into individual stock positions since 2005.

I’d readily admit that it feels good to be able to deploy cash in October and be able to redeem it in about six months – with tidy profits. However, I try to not let it get to my head. It would be easy for me to think that I knew it was going to be a short dip followed by a quick recovery. But that would be my hindsight bias. I am no fortune teller. In fact, if I had somehow known it’d be a quick six-month V-shaped recovery, I’d have gladly put all my cash reserves into stocks then and made even more profits.

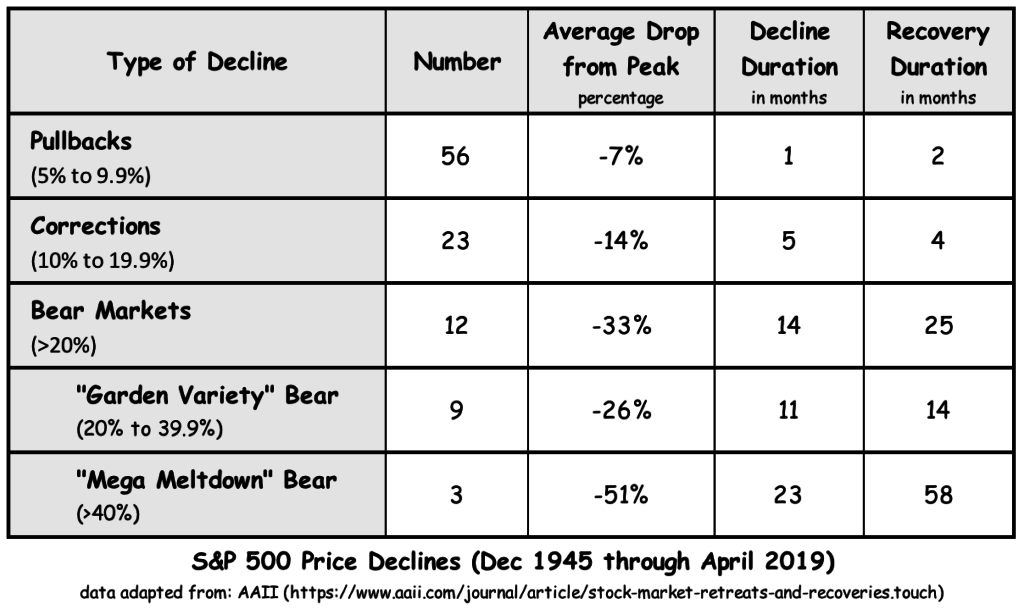

Market history research: To get a better perspective on how common this short market decline was, I went about looking for some historical data about the lengths of market declines. I found a nice summary in an article on AAII (American Association of Individual Investors) website. That data covered until July 2016. Since then we’ve had two more market corrections (drops of 10% or more). With the updated stats, below is a summary of all S&P 500 market declines from December 1945 until April 2019.

As you can see from the table, market pullbacks happen often but don’t last for long. A month of decline followed by a couple of months of recovery. Market corrections (declines of 10% to 20%) last longer though – on average, five months of decline and four months of subsequent recovery. The two market corrections we faced in 2018 were both shorter. The first one (January through August) was a 10.1% decline in just about two months followed by a four-month recovery. The second correction (September 2018 through April 2019) was much steeper – 19.8% decline in three months with four additional months of recovery.

In both cases, it took less than six months to fully replenish my dry powder cash. However, I am under no illusion that this will always be the case. When the stock market goes into an extended decline, my capital will stay invested for multi-year periods at a time. That would surely be the case when we enter a bear market. Take a look at the last two rows of the table. Garden Variety bear markets, on average, last about a year, followed by a 14-month period to fully recover. If we were to go into an average bear market tomorrow, I’d be able to deploy all of my dry powder cash and it will stay invested for a good two-year time period.

Next, take a look at those rare big bad bear markets – those that the AAII article author called Mega Meltdown bears. There have only been three in the last 74 years and boy, do they last long! On average, two years of decline followed by five years of recovery. I have been through two of them in my investing career: The Tech Bubble of 2000 and the Great Recession of 2008. See this post: My 401(K) story – from 1992 to 2012. Average stats here are not very meaningful though. The last two Mega Meltdown bear markets didn’t last nearly as long. Both times, total round trip time (from start of decline to full recovery) was between five and six years.

I have written several times in past blog posts that I don’t invest any capital in stocks that I might need in the next five years. I follow that rule for my dry powder reserves too. If we get into a deep bear market like the 2008 crash, I fully expect my dry powder cash to be tied up for five or more years. There are two mitigating factors to consider though:

One, as I follow a set of rules to gradually invest the dry powder (rather than invest all at once), as the stock market eventually starts recovering, the purchases I’d made last (say when the market was already down 30%) would become profitable much sooner than the market recovery completes. A similar benefit can be seen when investors do dollar-cost averaging: The purchases made at the market trough give a good boost to portfolio values when recovery begins. In a previous post (My 10-year odyssey with a Schwab index fund), I shared my real-life experience of this post-crash portfolio recovery while investing through the Great Y2K Dot-com meltdown.

Another factor to consider is the impact of dividend reinvesting. The decline and recovery times shown in the table were based on the S&P 500 price returns. Dividends we receive from the S&P 500 companies were not taken into account. But those dividends are real, and a vast majority of businesses keep paying them even during recessions. I plan to reinvest those dividend dollars back into stocks even during downturns. That would also help my portfolio recover quicker than nominal decline-recovery times. In another post last year (Revisiting the lost decade of U.S. stocks), I pointed out how the S&P 500 had zero net return from March 2000 through September 2012 when measured without dividends. And yet, if we had reinvested all dividends during this time period, we’d have achieved 26% total return.

The main thing I get out of this analysis of past market declines is that if I stay steadfast and patient in my approach to investing and keep a long-term perspective, I’d do fine no matter what the market brings on next. In the words of the AAII article author:

Unless you have a fool-proof indicator of when declines are going to strike—and how far they will end up falling—you are probably better off taking advantage of these declines (rather than running from them) by buying instead of bailing.

Amen to that. “Buy, not bail” is my motto too!

Leave a Reply