As I explained in my previous post on dry powder, I have cash that only gets deployed when stocks go down by a certain amount. How much cash to deploy and when? From the same post, you can see the rulebook I follow.

As I explained in my previous post on dry powder, I have cash that only gets deployed when stocks go down by a certain amount. How much cash to deploy and when? From the same post, you can see the rulebook I follow.

If stocks follow historical averages, I may be able to deploy 10 to 20% of this cash every couple of years. Perhaps up to 50% – 60% in a half-decade. Still, up to 40% of dry powder may not get invested for a decade or longer. The stock market is unpredictable in the near-term but, on average, stocks go down 30% or more once in a decade.

Since I adopted this dry powder strategy five years ago, I have only been able to deploy cash a couple of times and only a modest amount.

Opportunity Cost. As you can imagine, there is a substantial opportunity cost with this strategy. A lot of money is tied in cash for long periods of time. Money that otherwise could have been invested for gains elsewhere. To reduce this cost, I use an options strategy called protective collars to invest this dry powder cash. I wrote about it earlier in this post: Get more out of your cash. In that post, I wrote about protective collars and buffered collars – both are equity-options based investments.

Protective Collars. Since I wrote that post, I’ve moved away from using buffered collars – opting instead to focus on protective collars. Why? Buffered collars have higher return potential than protective collars, but they come with limited principal protection. Because this is dry powder cash we’re dealing with, I need this investment to be fully principal protected. If/when stocks go down substantially, I will need my dry powder ready to be deployed. As you see from that earlier post, protective collars are fully principal protected.

With protective collars, my downside risk is known and limited at the time of investment. The upside potential is also known and capped. Actual realized return will fall somewhere between the two extremes. Let’s go through a real-world protective collar I invested in this month:

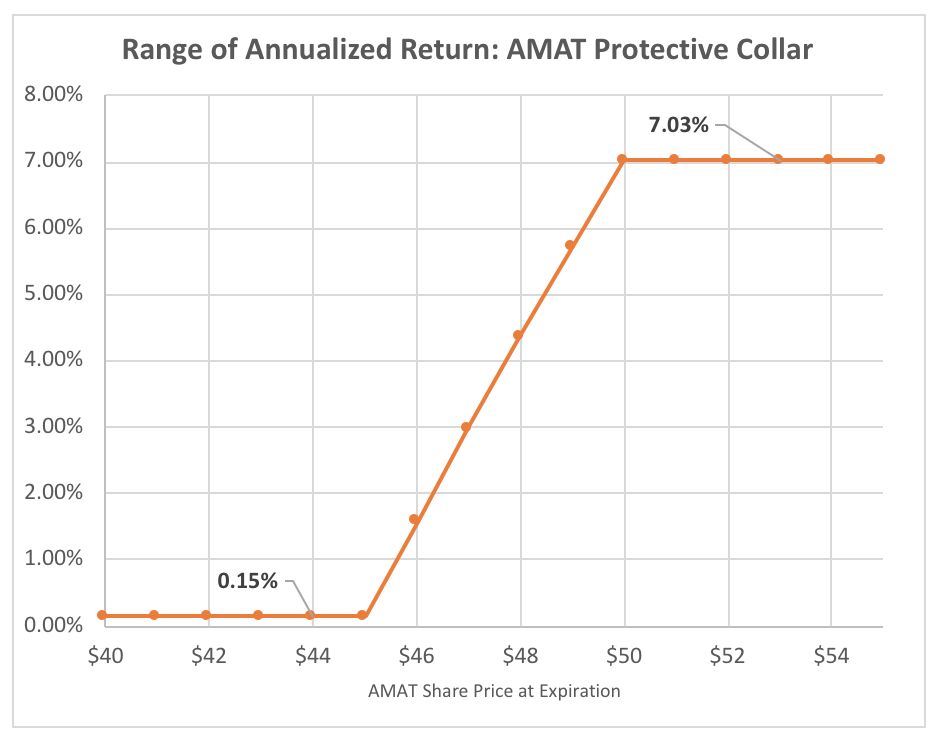

A real-world collar. This is a protective collar position I created on July 11th. It will last until January 2020 so about 1½ year before it expires. If Applied Materials (AMAT) shares rise to 50 or above by Jan 2020, my position will have a net annualized gain of 7.03%. Worst case return, in case AMAT drops below 45, would still be a gain (albeit small) of 0.15%. If you want to see the details of where these gains come from, see the earlier post where I detail how protective collars are set up.

A real-world collar. This is a protective collar position I created on July 11th. It will last until January 2020 so about 1½ year before it expires. If Applied Materials (AMAT) shares rise to 50 or above by Jan 2020, my position will have a net annualized gain of 7.03%. Worst case return, in case AMAT drops below 45, would still be a gain (albeit small) of 0.15%. If you want to see the details of where these gains come from, see the earlier post where I detail how protective collars are set up.

Why I chose AMAT? Because it is a business I understand well, its share price is depressed today but I believe it has a good chance of bouncing back in next 12 to 18 months, and its dividend is very safe. In other words, I believe there is a better than average chance that, provided the stock market does well in the time period, AMAT shares will be significantly up in next one year or so.

Return in every market? In general, protective collars, when chosen wisely on good stocks offer much better returns than cash/bonds in up markets. In down markets, I will get no return but my principal will be protected so I could then deploy cash to take advantage of bargain prices. In go-nowhere market, I will likely get par-with-cash (or a bit lower) returns. And that’s ok too. I will pay some opportunity cost but it is still a good tradeoff.

I could also generate better-than-cash return if I invest my dry powder in long-term corporate bonds. However, my money would then be stuck for 5 – 10 years. That would not work with my dry powder strategy. Here, my investments are locked for no more than 1½ year max. And I stagger expirations so that some positions are always maturing in a few months.

On occasions when I need cash quickly, I could use my rainy-day funds and when protective collars mature, I reallocate released cash into rainy-day fund. Money is fungible after all. See my full portfolio here.

Market-neutral returns? Going back to the last week’s post on Yale endowment, as I pointed out there, Yale has about one-quarter of its portfolio allocated to market-neutral absolute return strategies. It doesn’t keep much cash either – only about 1.2% as of 2017 report.

I haven’t found any good absolute-return funds that are open to retail investors like me – and those with decent long-term history that I’d feel confident investing in. Lacking this, my dry-powder cash invested in protective-collars is currently my best market-neutral alternative. With protective collars, I don’t take stock market’s downside risk – at the same time I get better-than-cash returns whenever the market is up. Over a full market cycle (including both its up and down phases), I expect to generate good return. In good times, I hold more collars. In bad times, I invest in cheap stocks.

[…] expenses (my rainy-day fund) as a way to keep my portfolio secure from ill-timed withdrawals. I also keep dry powder to take advantage of a down market – whenever it may […]