Is gold a good investment in today’s world? After all, gold is no longer the dominant medium of exchange – it has been replaced by national currencies backed by sovereign countries.

Is gold a good investment in today’s world? After all, gold is no longer the dominant medium of exchange – it has been replaced by national currencies backed by sovereign countries.

Our obsession with the yellow metal is well known. Gold coins have been in use for trade since 560 B.C. The Romans minted coins. Europeans used gold as a medium for exchanging goods with Asians and Africans. Without mutual trust of gold (or silver) coins, global trading between vastly different regions of the world would not have been possible. There were no other medium of exchange back then. Author Yuval Harari wrote about the era of global trading between continents:

-Yuval Noah Harari, “Sapiens, A Brief History of Humankind”

Gold as an exchange currency made sense back then because it is a precious metal – it is rare but naturally occurring. Goods could be conveniently valued in gold. People could be reasonably assured that the value of gold will stay about the same – because its supply was constrained.

– Yuval Noah Harari , “Sapiens, A Brief History of Humankind”

Today, the world has adopted fiat currencies – they are no longer backed by gold or any other physical commodity.

The problem with gold is that it does not have any inherent value. It has limited utility now that it does not serve as a currency. Neither does it produce any cash flow – unlike a profitable business, a farmland, a rental property, or even a government bond. Gold’s value lies in how much a buyer is willing to pay for it at a given time. That makes it subject to human sentiment and speculations. It also makes it difficult to put a number on its value.

Since gold does not produce any recurring cash flow, its value can’t be determined by traditional means of valuation. Its price often rises and drops with investor fears. People value gold higher when they fear that the traditional currencies will devalue due to inflation, recession, mismanagement, corruption, or any number of related concerns.

Similar to gold, the stock market is also subject to investors’ speculation. It also fluctuates widely in the near term. However, unlike gold, stocks also have an intrinsic value because they are tied to underlying businesses that produce income. Their value can be derived from their future income generating potential. As long as a country’s GDP is growing, its businesses will also continue to increase profits for their owners (i.e. stockholders).

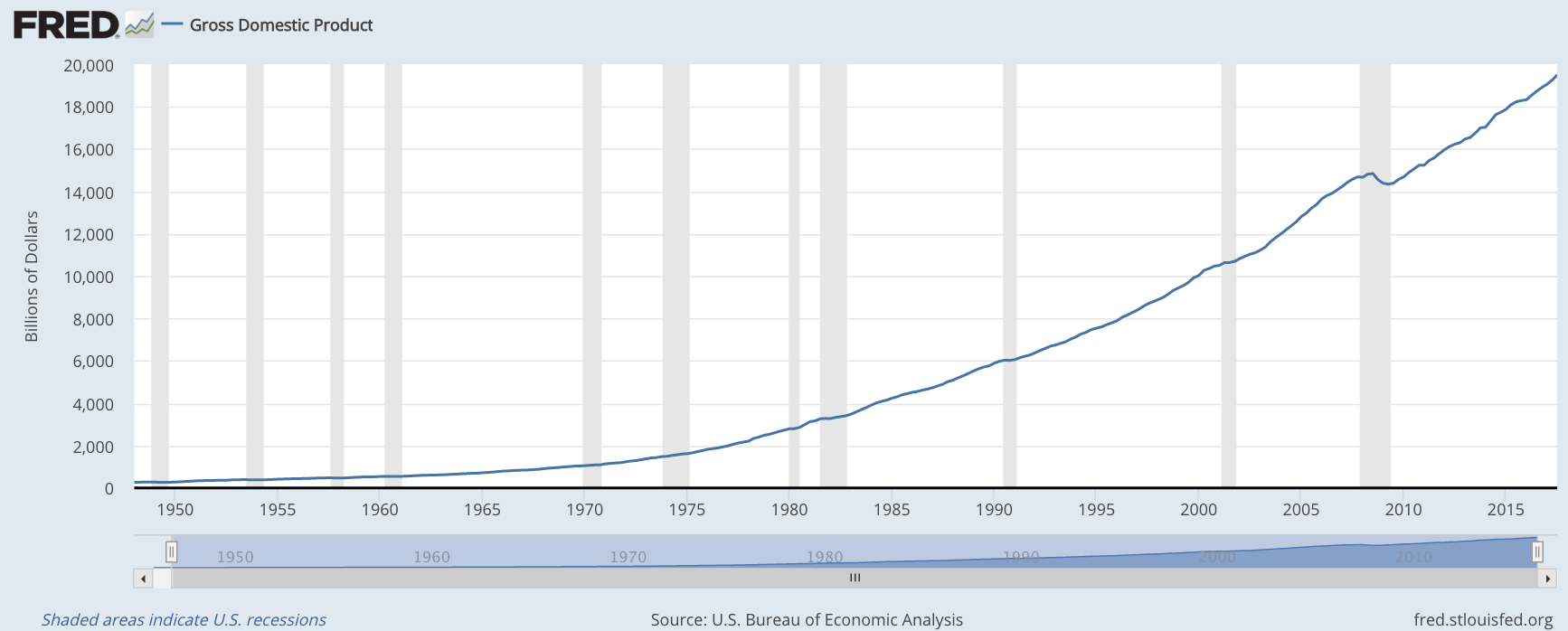

You can see how U.S. GDP showed a relentless and steady rise in the last 65 years as the country grew its population and productivity.

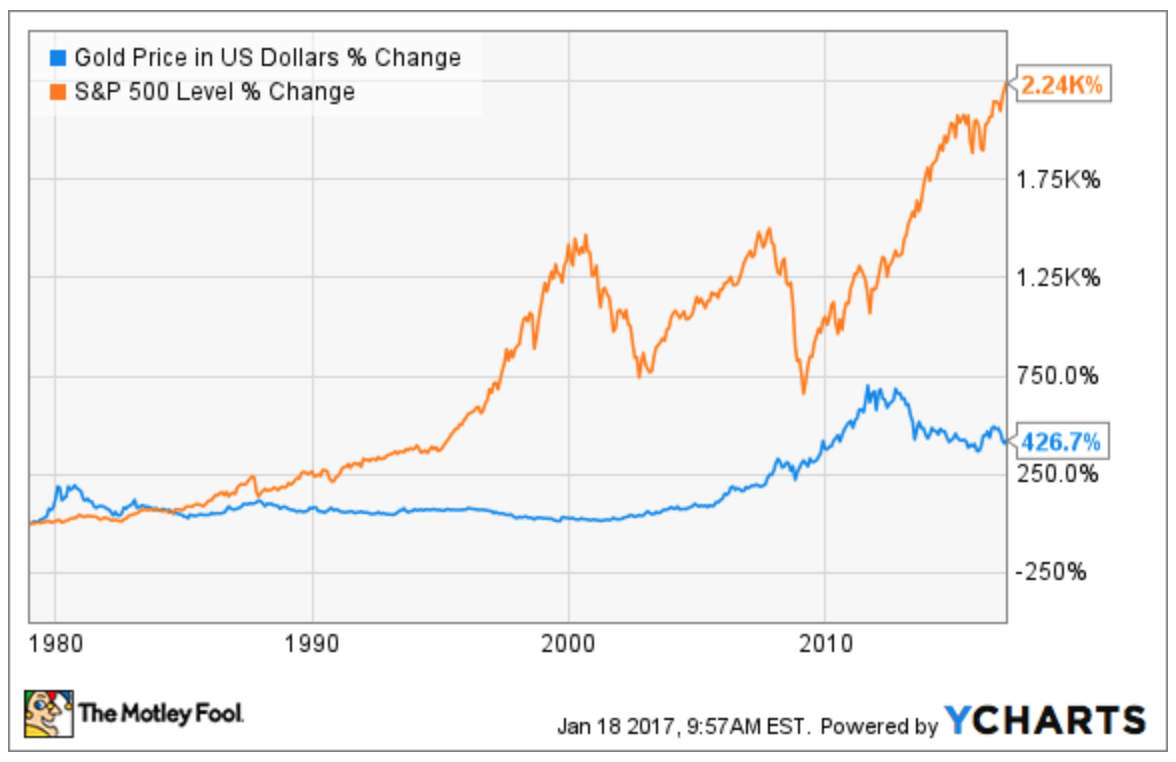

As the GDP grew, the US stock market also grew – albeit with much greater volatility.  Take a look at how gold and the U.S. stock market have done since 1980s. As expected, the stock market is more volatile, but it also has a clear upward trajectory over the long term. Gold’s value rose in early 80s when Nixon took U.S. off the gold standard and inflation was rampant. But as fear over the economy subsided and inflation got under control, gold steadily declined in value over the next three decades. It rose once again in the most recent decade as fears about the economy started building again – peaking in the aftermath of the Great Recession.

Take a look at how gold and the U.S. stock market have done since 1980s. As expected, the stock market is more volatile, but it also has a clear upward trajectory over the long term. Gold’s value rose in early 80s when Nixon took U.S. off the gold standard and inflation was rampant. But as fear over the economy subsided and inflation got under control, gold steadily declined in value over the next three decades. It rose once again in the most recent decade as fears about the economy started building again – peaking in the aftermath of the Great Recession.

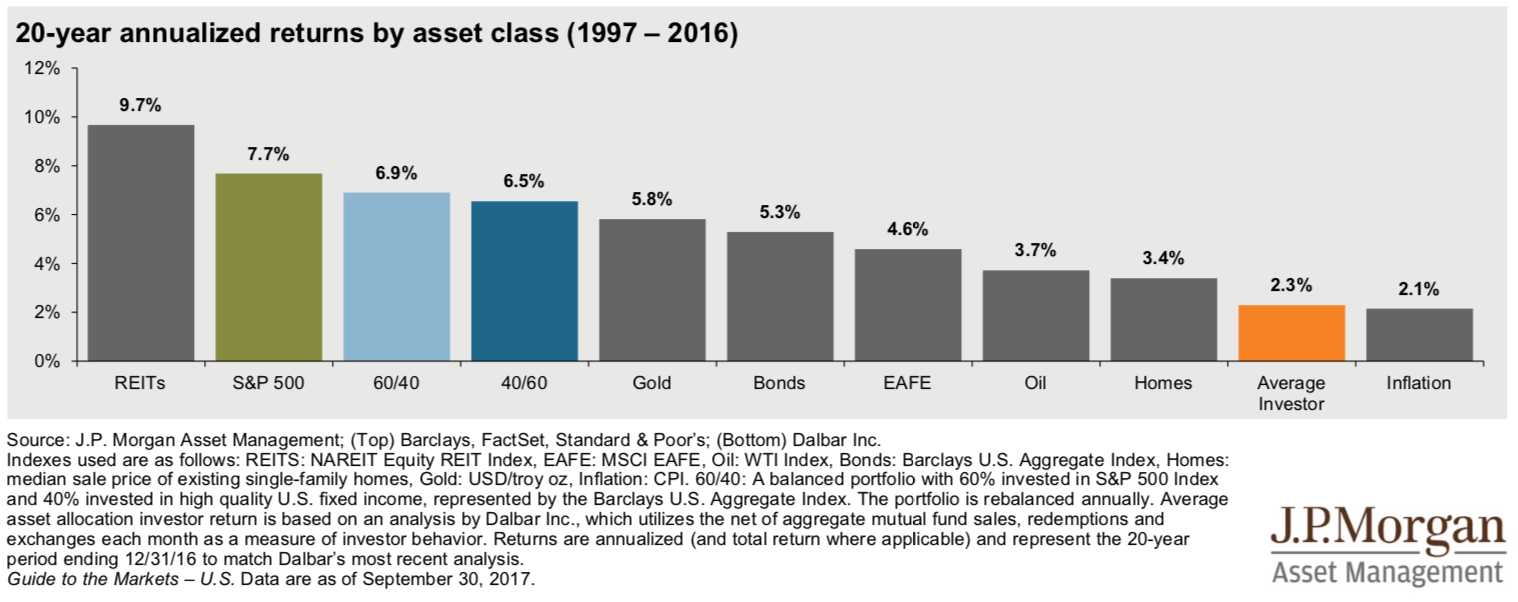

Even with this recent rise of gold, it still did not manage to beat the US stock market. As this chart from JPMorgan shows, gold had an average annualized return of 5.8% while the S&P 500 index rose by 7.7% in the last 20 years. And remember even this gold’s improved performance came in reaction to the widespread fears prevalent during the 2008-2009 Great Recession. Where do you think gold price would be in the next 10 years if another such deep recession does not materialize?

If you have 10 or more years to grow your savings, where would you rather put your current and future savings in? Can you count on gold to grow your nest egg faster than alternatives? Or put another way, can you count on fears rising about the state of the economy, the currency, or the global trade? If not then you are better off not putting your money in gold.

Warren Buffett does not believe in gold as an investment either. In the 2012 Berkshire Annual Letter, he compared a pile of gold with an equivalent investment in agricultural land and businesses.

Pile of Gold versus U.S. Farmland

“Today the world’s gold stock is about 170,000 metric tons … At $1,750 per ounce – gold’s price as I write this – its value would be $9.6 trillion. Call this cube pile A. Let’s now create a pile B costing an equal amount. For that, we could buy all U.S. cropland (400 million acres with output of about $200 billion annually), plus 16 Exxon Mobils (the world’s most profitable company, one earning more than $40 billion annually) … Can you imagine an investor with $9.6 trillion selecting pile A over pile B? Beyond the staggering valuation given the existing stock of gold, current prices make today’s annual production of gold command about $160 billion. Buyers – whether jewelry and industrial users, frightened individuals, or speculators – must continually absorb this additional supply to merely maintain an equilibrium at present prices.”

“A century from now the 400 million acres of farmland will have produced staggering amounts of corn, wheat, cotton, and other crops – and will continue to produce that valuable bounty, whatever the currency may be. Exxon Mobil will probably have delivered trillions of dollars in dividends to its owners and will also hold assets worth many more trillions (and, remember, you get 16 Exxons). The 170,000 tons of gold will be unchanged in size and still incapable of producing anything. You can fondle the cube, but it will not respond. Admittedly, when people a century from now are fearful, it’s likely many will still rush to gold.”

“I’m confident, however, that the $9.6 trillion current valuation of pile A will compound over the century at a rate far inferior to that achieved by pile B.”

– Warren Buffett, “Berkshire Hathaway Annual Shareholder Letter 2012”

Note that Buffett wrote this note in 2012 when gold was at its peak – it has come down since then. Do you feel like betting against Warren Buffett? I don’t – given his past record. For instance, see this bit of advice he gave in 2008.

I don’t invest my savings in gold. I am not a worrywart. Recessions may come and go. US dollar will rise and fall. Inflation perks and subsides. As I wrote in a previous post, recessions are part of normal business cycle – not something to fear about. U.S. economy is the largest in the world and arguably the most resilient too. Rather than count on investors’ fears rising, I take a prudent approach to investing – by keeping enough dry powder to take advantage of stock market downturns.

The only gold I’ve ever spent money on was in form of gifts for my wife. But that’s not investing in the traditional sense. Rather, they were investments in my marriage!

Leave a Reply