Why so many people seek to double or triple their money in no time? First, it’s the thrill of doing it. And perhaps bragging about it to friends and family.

Why so many people seek to double or triple their money in no time? First, it’s the thrill of doing it. And perhaps bragging about it to friends and family.

Another reason could be that people don’t really understand the power of compounding. As we explored in an earlier post, consistent 10-15% return will make you lot of money if you are patient and disciplined.

Yet another somewhat depressing reason people aim to double triple their money in quick order is that they might be running out of time.

When you are 25, you don’t have as many big expenses coming your way soon. Perhaps some college loans to pay off, a down-payment for an apartment, upcoming marriage, etc. When you are 50, you start worrying about your own retirement. If you hadn’t started saving for retirement until then, you’d have squandered away the chance of 25 years’ worth of compounding your savings. So what do you do then? You seek higher returns from savings to make up for lost time.

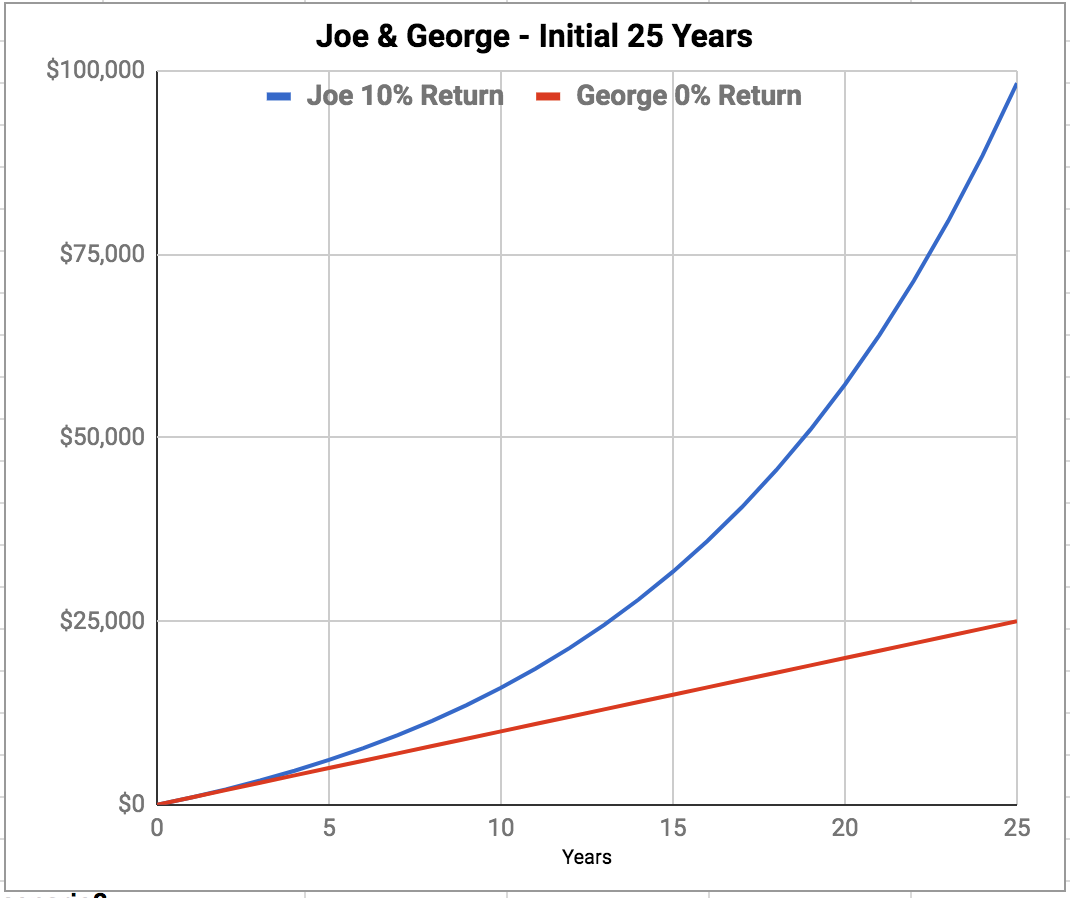

Take this hypothetical example:

Joe and George are both 25-years old. They put away $1000 every year. Joe invests his money into a stock index fund getting an average annual return of 10%. George, on the other hand, is a very conservative individual. He keeps his savings in a cash account (or may be under a mattress) that does not pay any interest. Neither of them take any money out of their savings. After 25 years of savings, Joe’s total investments would have grown to be about 4 times higher than George’s ($98.3K versus $25K). You can see from the chart how the gap between Joe’s and George’s portfolio widens every year that goes by.

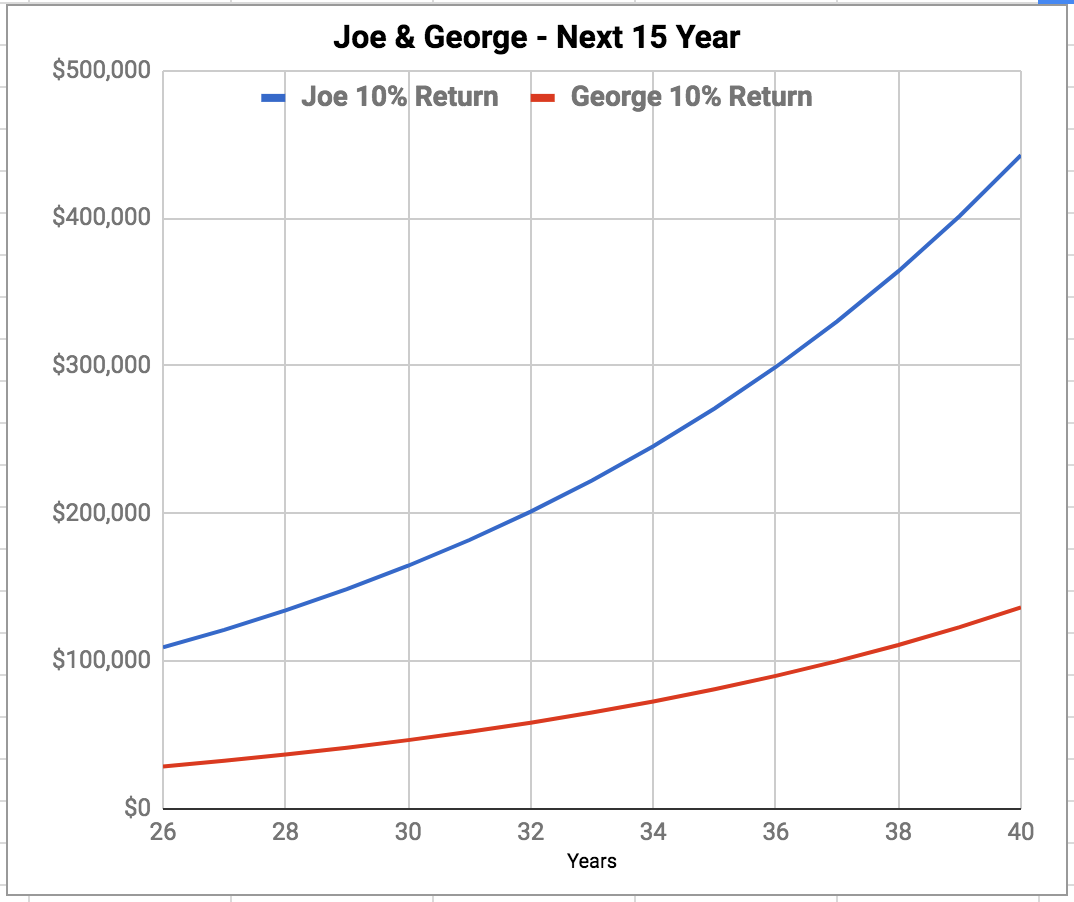

Here is a twist to the above scenario:

Joe and George are now 50 years old. After 25 years of just keeping all his savings in a cash account, George now realizes his mistake and wants to make up for it. If he now switches over to a 10% yielding investment like Joe’s, he still can’t narrow the widening gap between his and Joe’s money. At 65, Joe will be a half-millionaire (nearly) at $442,500 while George still only about a third of it ($136,200).

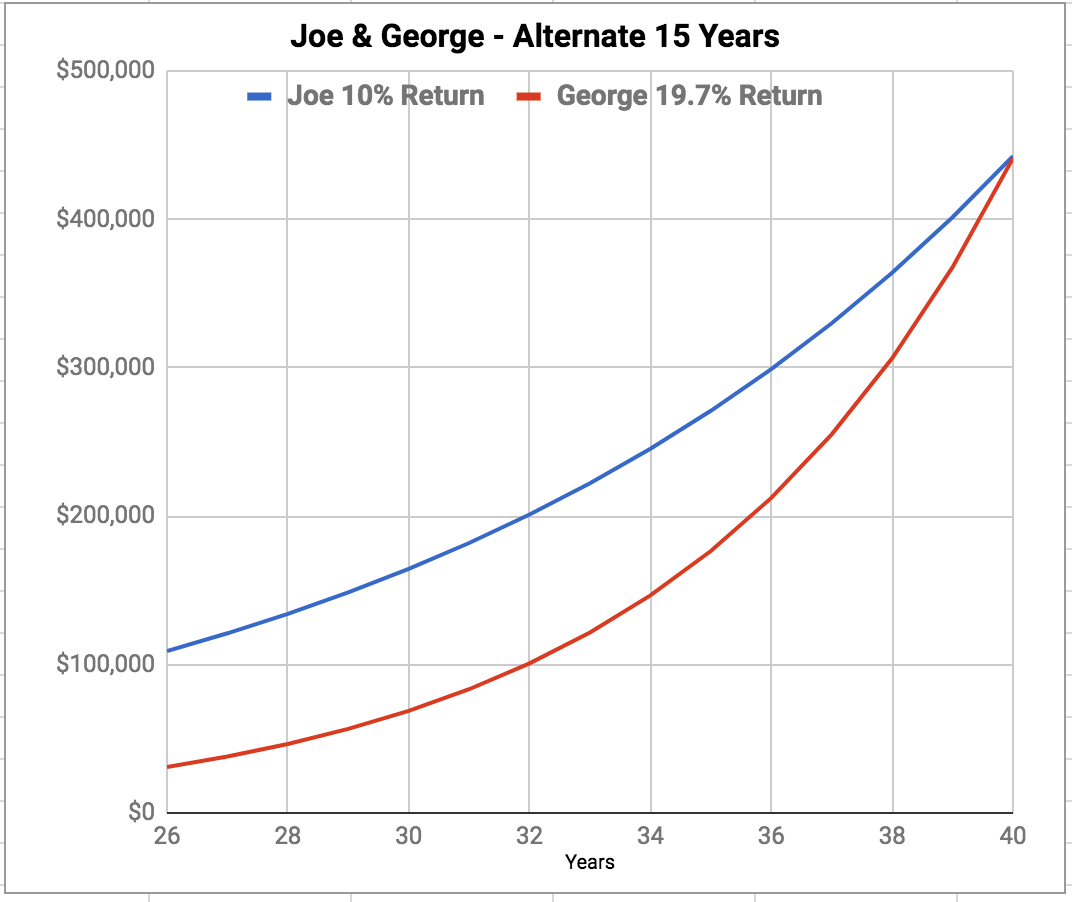

Once Joe’s has established a 25-year head start, it is very difficult for George to catch up to him. George only has another 15 years to catch up if he wants to retire at 65. As this next chart shows, George will need to find an investment that could return 19.7% annually for next 15 years in order to bridge the valuation gap. Unless George is an extraordinary investor, achieving a 19.7% annual return for 15 years is an impossible target.

You don’t want to be in George’s shoes. It is highly unlikely that George will find suitable high-return investments to make up for the lost time. Investments that promise higher-than-average returns rarely keep their promise – and more likely end up as major disappointments.

Rather, you want time to be on your side – be like Joe – start early in your savings/investing career and even boring middling 10% returns will get you where you need to be.

Related:

Leave a Reply