One recurring theme in a young earner’s life is that you never have enough money to buy something outright! But what you do have is future cash flow – many years of earnings ahead. You take out loans against the future earnings to buy a car or a house that you otherwise could not afford to buy outright. You can also save and invest a portion of that cash flow for a future spending need – or even retirement.

One recurring theme in a young earner’s life is that you never have enough money to buy something outright! But what you do have is future cash flow – many years of earnings ahead. You take out loans against the future earnings to buy a car or a house that you otherwise could not afford to buy outright. You can also save and invest a portion of that cash flow for a future spending need – or even retirement.

Just like you can buy a big-ticket item and pay it off gradually over many years from future cash flow, you can think of saving for retirement the same way. Save and invest a portion of your earnings every month to buy your retirement. I call this investing in installments. You will be investing a small chunk every month for many years. This turns out to be a good thing for another reason too …

When you invest a small amount regularly in the stock market, you don’t need to be concerned about where the market is going. If the market goes up from there, your portfolio will grow with it. If the market goes down, your dollars will be buying more shares at a cheaper rate than before – a good thing. In either case, you win!

Consistently investing a fixed dollar amount every month is a good thing. Investment professionals call this dollar-cost averaging. You don’t need to worry about where the market might be heading next. Another good thing is that it helps most investors stay calm and disciplined as market fluctuates – as it is wont to do.

Remind yourself of these points whenever you find yourself questioning the wisdom of steady investing through thick and thin …

Up Market:

- The market is rising – so is your investment portfolio. You should be feeling good about it.

- Is the market too high and about to crash? No one knows for sure but you have many more dollars to invest in future so why worry. If the market tanks, your savings will buy you even more shares.

Down Market:

- The market has tanked and financial media is panicking. It’s ok for you because of two reasons:

- You know the markets always recovers over time. You have another 10, 15, even 20 years to go before you need this money.

- Your new dollars will buy you a lot more shares in good businesses than before.

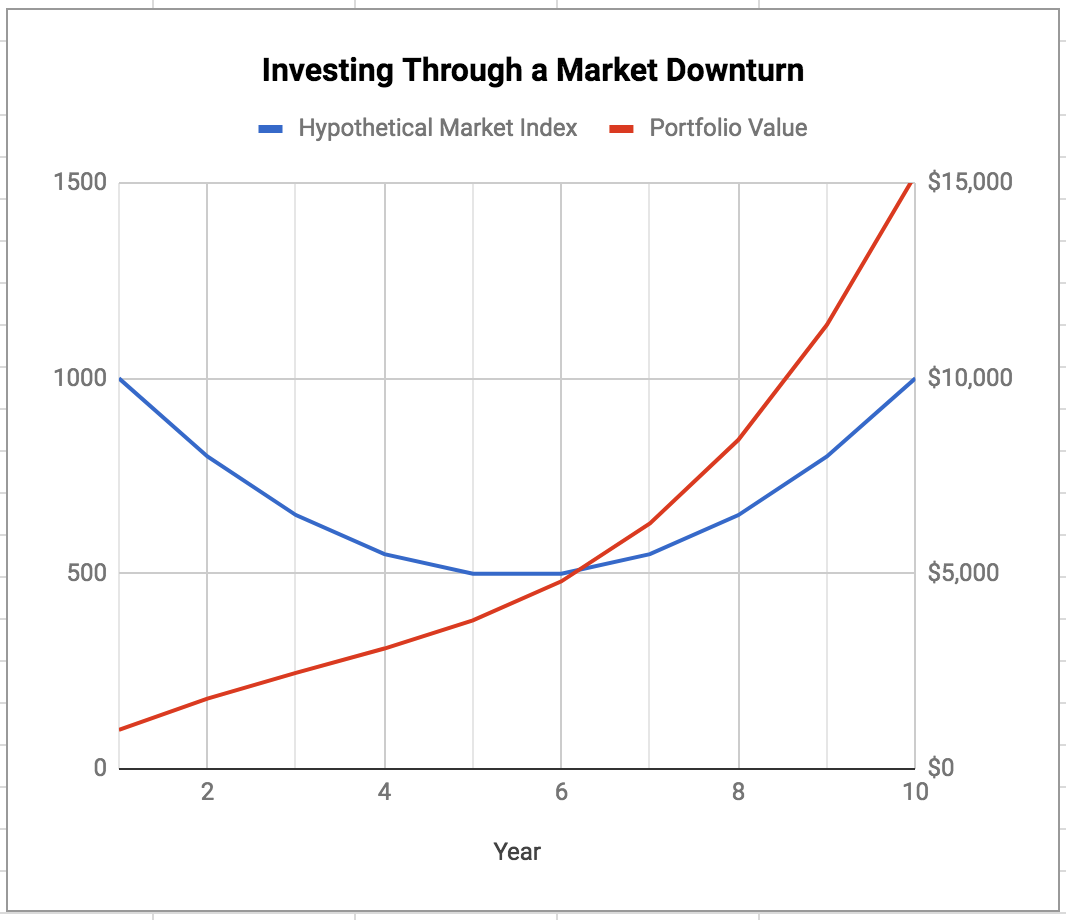

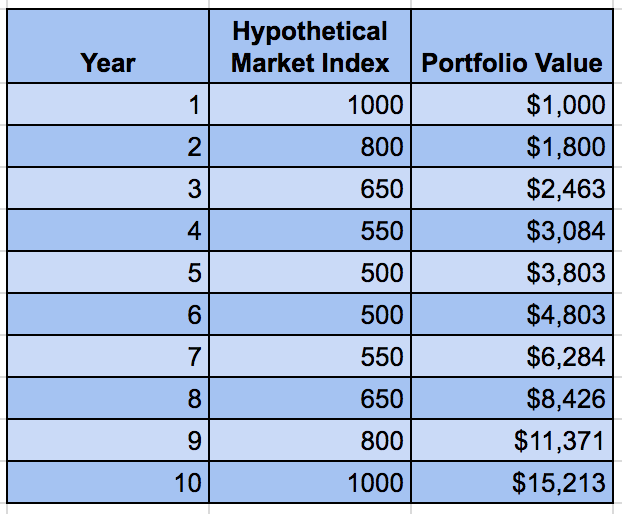

Consider this hypothetical scenario: you started investing when the stock market index is at a high of 1000 and just about to start dropping from its peak. Over the next five years, the market keeps going down every year – becoming cheaper by the year. At the end of year 5, it hits a bottom of 500 and then gradually recovers until by the end of year 10, it has reached its previous high of 1000. So in 10 years, the market has essentially come back to where it was before – overall return of zero. But if you have been investing by installments, you’d have made money even in this market. Why? Because you spread your buying uniformly over ten years – buying less shares when the market was high and buying more as the market goes down.

If you have invested $1000 at the beginning of each year, by the end of year 10, your investments would have grown to be $15,213. Your total gains for the period are $5,213 ($15,213 minus your savings of $1000 x 10). You gained more than 50% on your portfolio despite the market being essentially flat for the entire 10-year period.

Sounds easy, doesn’t it? To do this successfully in real-life, you will need a steady hand – don’t panic when the market is down – and don’t get too excited when market is up. Stay even keel and stick with your investing schedule.

[…] investing the money you save – over time and in any market condition. See this post: Investing in Installments. When I was younger and had a busier life, I just had my 401K account on auto-pilot. Dollar-cost […]