As my long-time readers would know, I am always looking for companies that are running quality businesses and have the durability to survive economic downturns. My goal is to find them, invest in them, monitor their progress, and just hold on to them as they grow.

Last month, I read Simon Kold’s book On The Hunt For Great Companies. He called the book an investor’s guide to evaluating business quality and durability. In the book, he had put together an excellent framework for judging a business’s quality: from people running the business, to the business’s inherent competitive advantages, to assessing various risks the business faces, etc.

It was a great read overall. The inspiration for this blog post came from the final section of his book titled Predicting Quality. He asked: Is it possible to predict future quality rather than merely measuring current quality? He then went on to explain that even though his framework was specifically designed to measure current quality, it could also be applied to theorize about the future quality of a business.

In other words, can we spot businesses that have emerging quality, rather than those that have already established quality? For example, could we have predicted in 2003 that Amazon showed signs of emerging quality? The author went on to evaluate 2003’s Amazon against his framework of evaluating the management, its emerging business advantages, and the risks it faced as it scaled up. His conclusion from the book:

I think no one could have comfortably predicted the extent of Amazon’s wild success, but I do think that the frameworks of the book can also be used to make judgments about the future quality of a business.

Now, Amazon is a favorite business of mine and I own it since 2000. I can reasonably argue that I bought Amazon well before it became a proven quality business. This question led me to look into my own portfolio and identify what other businesses I’ve bought in the past that were then emerging stars and were not yet of proven quality.

I picked inclusion in the S&P 500 index as a rough proxy for when a business transitions from emerging to established quality. This does not work every time, but I think it will do as a quick measure. After all the index comprises of the largest 500 US based publicly traded companies that also meet certain other requirements such as GAAP profitability, public float, and restrictions on corporate structures. While the index does not always carry the very top 500 market-cap companies, it comes close to it. To get to the top 500 requires business scale and market recognition that generally eludes emerging contenders.

With that in mind, I screened for all the companies that I had bought in my portfolio before they were included in the S&P 500, and I still own them. The screen found seven of them and I added another two that I think are on the verge of getting listed. Here’s the full list:

Inclusion in a major index like the S&P 500 usually moves share price up significantly, sometimes in anticipation of it. The reason has to do with all the passive index funds and ETFs that mirror the S&P 500. Those funds are all forced to buy each new member company in proportion to their portfolios.

But the upward moves are not just limited to the initial spikes. As you will see in the stock charts, most of the businesses I own exhibited strong upward movement months and years after their initial index inclusions. To me, this is evidence of them getting recognized as proven durable quality businesses.

On above nine stocks: While one or two of them (Berkshire and Brookfield come to mind) may already be proven quality businesses when I first bought them, most were not. Those two just happened to not be in the index for other reasons, which I’ll discuss below. For the remaining, at the time I bought them, I don’t think they would have passed Simon Kold’s quality assessment framework. None of them had developed a competitive barrier to keep others out. In Kold’s terms, they did not have economies of scale, switching cost advantage, network effect, brand advantage, or proprietary resources. Yet.

So what made me pick these companies when they were still emerging stars? At the time, I could see some possibly developing scale advantage over competition; some had business models that lend to potential network effect down the road; and some others had first-mover advantage that could’ve someday translated to brand or switching cost advantages. But still, they were not there yet.

What stood out as a common theme among these picks was that they were all run by founder-CEOs who were passionate about their businesses, had long-term incentives tied to the business’ success, and were reliable and consistent communicators. I’ve written before about my focus on founder-CEOs. It is a key aspect of my investing approach. Many of my most successful investments were from founder-run businesses.

Assessing business managers is also a key topic in Simon Kold’s book. There, he attempts to answer the following question: What makes some people create exceptional long-term per-share business performance? I won’t rehash his full analysis here; for that, you should read his book. But here is a scale on which he suggests that we rank business managers:

Control of companies is placed with people spanning a panoply of passion:

- At one end are people for whom the job is a stepping-stone, something they do a few years until a bigger company calls.

- At the other end are people for whom the firm is their life’s work.

Let’s go over each individual business in more detail:

Amazon was added to the index in late 2005 at the time when the market had mostly recovered from the Y2K bust but it would be a few more years before Amazon recovered its Y2K high. It’s debatable if Amazon was already an established quality business by year-end 2005. Certainly, media did not see it that way. There were many negative stories about Amazon back then, including a long running theme that Amazon was never meant to generate any profits ever. Over time, Amazon proved the naysayers wrong.

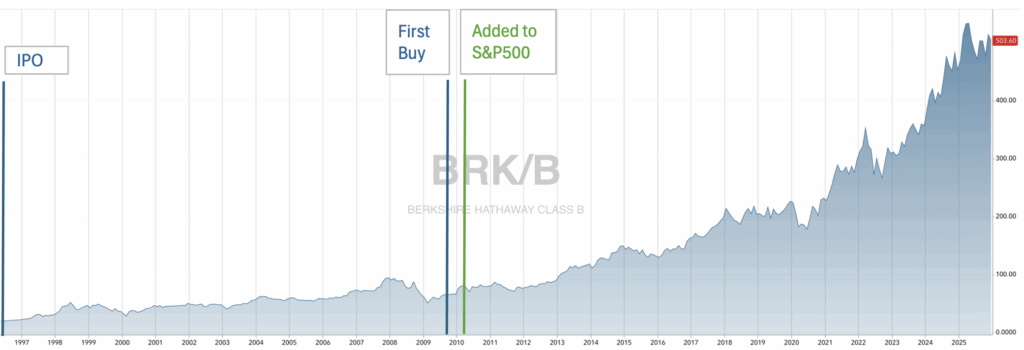

Berkshire Hathway is an outlier in this list. Its shares have been publicly available since 1965 in one form or other; first on OTC markets and then on NYSE. Then in 1996, it introduced class B shares that were worth 10,000x less than earlier class A shares. This made Berkshire shares much more affordable to individual investors. 14 years later, those class B shares were granted a seat in the S&P 500. When I bought B shares in 2009, it was arguably already a well-established quality business. So perhaps, Berkshire should not even be on this list.

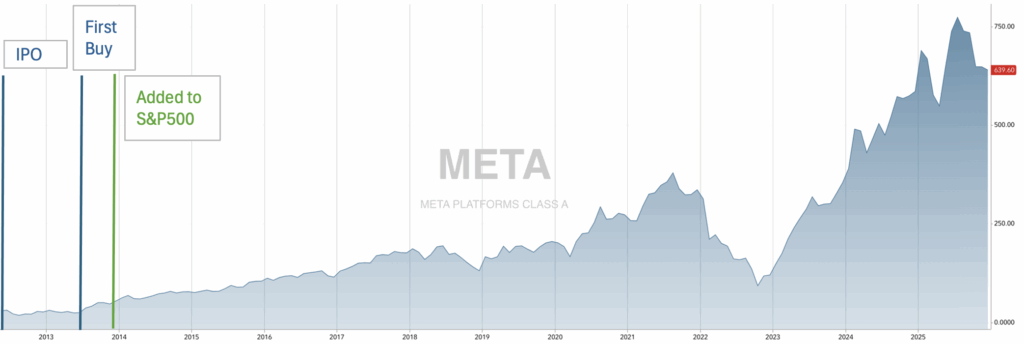

I bought Meta (then Facebook) about a year after its IPO in 2012. Six months later, Meta was added to the S&P 500. This quick move from IPO to index inclusion was mainly due to Meta having already established strong financial numbers even before it came public. One could argue that Meta was already a proven quality business at that time. Do note though how it continued to scale up in a big way in the years since the index inclusion.

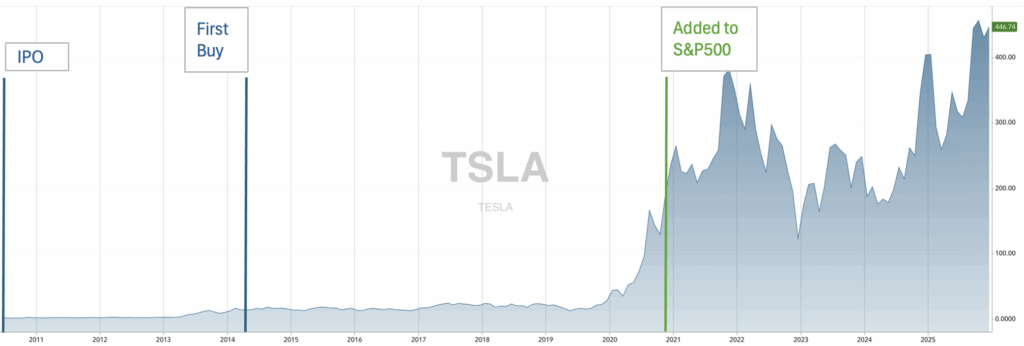

Next up is Tesla. At the time I first bought shares, Tesla was definitely not in the same league as Meta. It wasn’t profitable and years away from developing its first mass-market affordable electric car. It took S&P more than ten years post IPO to add it to the index. That was seven years after I first bought shares. Since then, the market has clearly recognized it as a quality business, as seen from its chart.

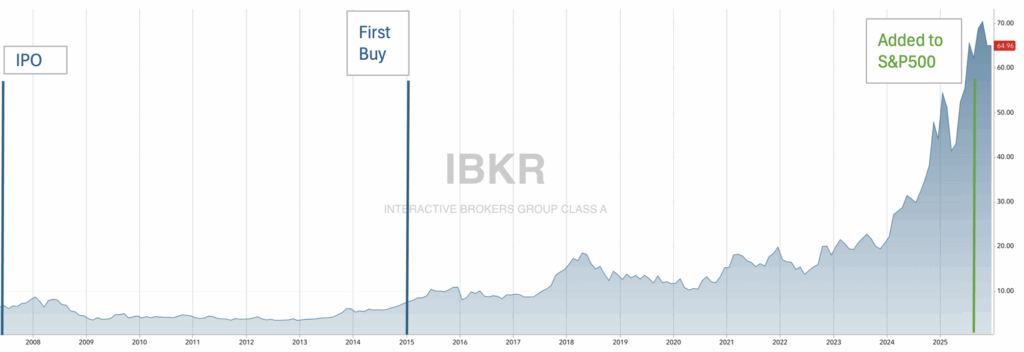

Interactive Brokers just got included in the index this year, ten years after I first bought shares. Then, it was a much smaller broker though already very profitable and well regarded in the industry. Today it has greater than $100B market cap and ranks in the middle of the S&P 500 pack. IBKR could also have been picked for the index earlier, but was excluded due to its dual-class structure and limited share float. It may not have established its creds in 2015, but it has been a proven quality business for several years now.

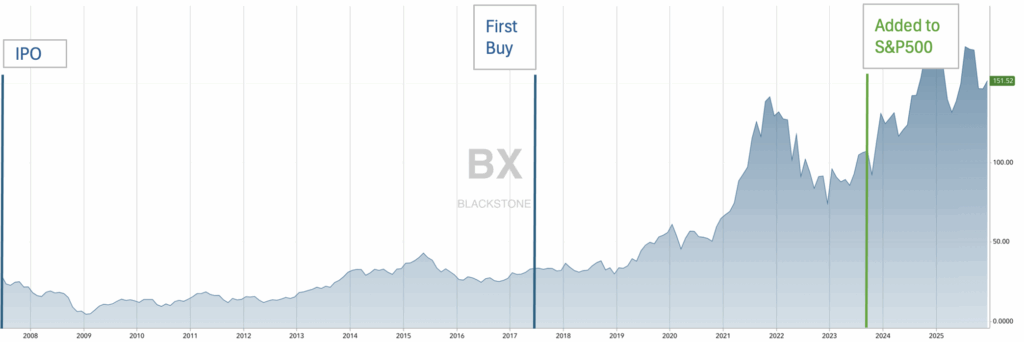

Blackstone went public as a publicly traded partnership (PTP) in 2007. As it grew substantially over the years, it remained ineligible for S&P inclusion because of its corporate structure and multiple share classes. In 2019, Blackstone converted into a C-corp and then in 2023 S&P dropped its share class restriction, thus making BX eligible. I became a shareholder when it was still a partnership in 2017. It’s debatable if it was already a proven high-quality business back then. But it’s pretty clear it was there when S&P finally decided to add it.

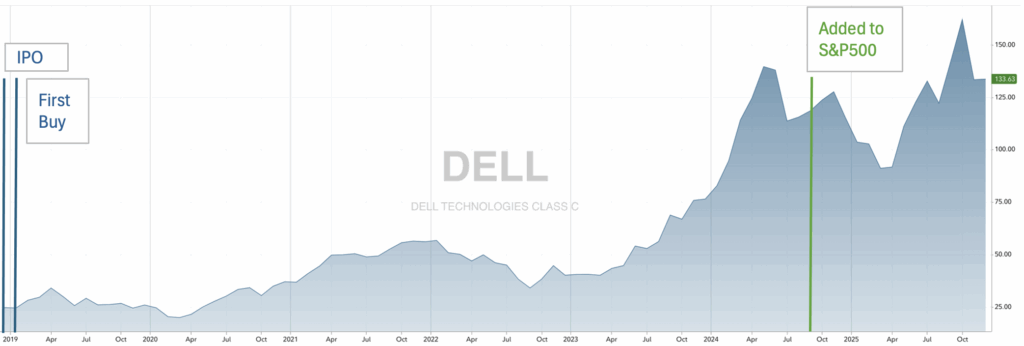

Dell started its second life as a public company in 2018. I was intrigued enough by the business and its eponymous founder-CEO that I bought shares a few months later. But it didn’t get picked for S&P 500 until 2024, almost six years later. The reason was lack of consistent GAAP profitability. It was always cash flow positive but had large debt burden and high amortization expense from prior acquisitions. Well before its inclusion, the market had already started looking favorably at Dell stock, as you can see from its chart.

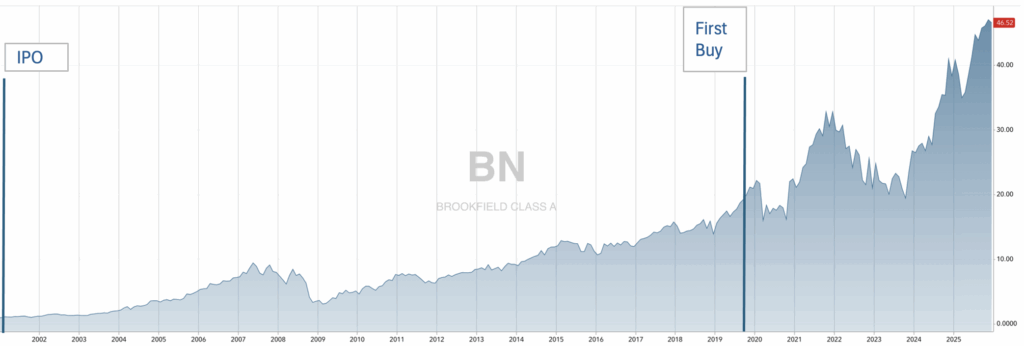

Brookfield is not part of S&P 500. But it is already a well-regarded quality business. Main reason why neither of its two main corporate entities are in the S&P 500 is because it is headquartered in Canada. However, now that its asset management arm, BAM, has relocated to New York, I expect it to be picked by the index eventually. I came late to Brookfield (just six years ago). It had already done very well for its shareholders since its 2000 IPO.

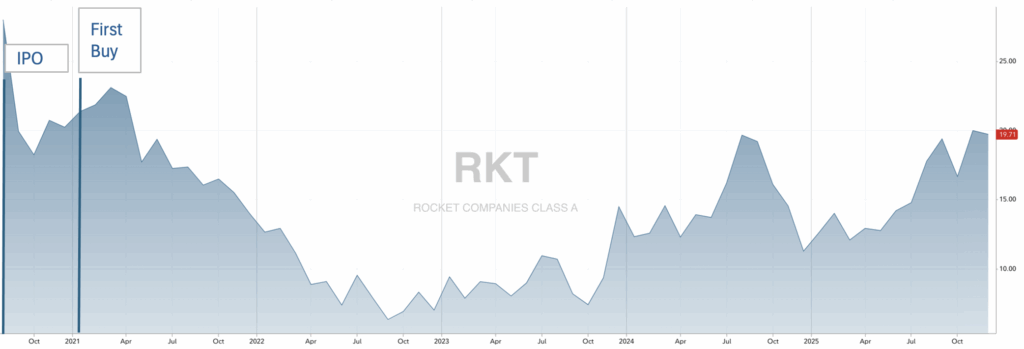

Rocket Companies first went IPO in 1998, but it was soon taken private by Intuit. Three years later, Dan Gilbert, its founder, bought back the business from Intuit for $64 million, a mere pittance when one compares with its current valuation. He ran the business as CEO from its founding in 1985 until 2002. He is still chairman of the board and controls majority stake in the business. Rocket’s second IPO was in 2020. Today, its current market cap is about $53 billion. Rocket could soon be eligible for S&P 500 inclusion; just as soon as it shows consistent GAAP profitability. I fully expect it to do so when the housing market recovers from its current slump.

You can check my full portfolio and its performance here.

Leave a Reply